Biotech Depot 2008 - 500 Beiträge pro Seite

eröffnet am 03.08.08 17:44:52 von

neuester Beitrag 11.01.09 16:18:50 von

neuester Beitrag 11.01.09 16:18:50 von

Beiträge: 126

ID: 1.143.292

ID: 1.143.292

Aufrufe heute: 1

Gesamt: 46.195

Gesamt: 46.195

Aktive User: 0

Top-Diskussionen

| Titel | letzter Beitrag | Aufrufe |

|---|---|---|

| gestern 23:11 | 499 | |

| heute 00:52 | 263 | |

| gestern 21:36 | 158 | |

| gestern 23:28 | 147 | |

| vor 48 Minuten | 143 | |

| heute 00:16 | 139 | |

| vor 1 Stunde | 131 | |

| vor 1 Stunde | 130 |

Meistdiskutierte Wertpapiere

| Platz | vorher | Wertpapier | Kurs | Perf. % | Anzahl | ||

|---|---|---|---|---|---|---|---|

| 1. | 1. | 18.668,00 | -0,69 | 205 | |||

| 2. | 3. | 0,7757 | +15,60 | 93 | |||

| 3. | 2. | 2,6950 | -41,09 | 89 | |||

| 4. | 4. | 176,75 | -1,39 | 66 | |||

| 5. | 6. | 23,740 | +24,95 | 66 | |||

| 6. | 5. | 0,1930 | -4,93 | 59 | |||

| 7. | 8. | 1.139,01 | +6,98 | 42 | |||

| 8. | 7. | 2.358,14 | -0,13 | 39 |

Hallo!

Soll ich es nochmal wagen nach dem GPC-Desaster im letzten Jahr (Thread: Biotech Depot 2007)? 2008 ist schon halb rum... daher nun nach dem katastrophalen Biotech-Depot 2007 sehr verspätet nun wieder das neue Depot der reinen Biotechs 2008! - Neues Jahr neues Glück?

- Neues Jahr neues Glück?

Die einzige Lehre, die ich aus dem letzten Jahr ziehen kann: nie wieder eine so große Position auf einen Wert konzentrieren, speziell wenn es sich dabei um ein Ein-Produkt-Unternehmen handelt. Daher orientiere ich mich seitdem an den mittleren, bereits etwas teureren Biotechs, die entweder bereits profitabel sind oder eine breite Pipeline besitzen, viel Cash, hohe Investitionen in die Entwicklung, Produkte möglichst weit in der klinischen Entwicklung, potentielle Blockbuster und namhafte Partner. Zudem soll das Depot eine höhere Streuung erhalten. Der zurückliegende Monat ist ausnahmsweise mal sehr positiv gelaufen, so dass ich es wage, einen entsprechenden Thread zu meinen Biotech-Werten zu erstellen.

So sieht es aktuell im Depot aus:

24,3% Genmab http://finance.yahoo.com/q?s=GEN.CO

15,4% Regeneron http://finance.yahoo.com/q?s=REGN

9,5% Onyx http://finance.yahoo.com/q?s=ONXX

7,2% OSI Pharma http://finance.yahoo.com/q?s=OSIP

6,3% (KO) Intercell http://finance.yahoo.com/q?s=IJE.F

5,4% Vertex http://finance.yahoo.com/q?s=VRTX

5,3% Cubist http://finance.yahoo.com/q?s=CBST

5,1% Imclone http://finance.yahoo.com/q?s=IMCL

5,1% Evotec http://finance.yahoo.com/q?s=EVT.DE

4,8% Isis http://finance.yahoo.com/q?s=ISIS

4,0% Arena http://finance.yahoo.com/q?s=ARNA

3,1% ViroPharma http://finance.yahoo.com/q?s=VPHM

2,7% Micromet http://finance.yahoo.com/q?s=MITI

1,9% Supergen http://finance.yahoo.com/q?s=SUPG

auf meiner Watchliste stehen INCY, RIGL und POZN. In der zweiten Reihe SGEN, Basilea, EXEL und MNTA.

Aus dem alten Depot ist nur noch Genmab und Arena übrig geblieben... GPC hat sich nahezu aufgelöst, MOR, POZN und CRME habe ich verkauft, während Speedel kürzlich übernommen wurde.

Ich hoffe, dies wird ein besseres Jahr! Der NBI steht momentan gar nicht schlecht... kann sich aber auch schnell wieder ändern.

mfg ipollit

Soll ich es nochmal wagen nach dem GPC-Desaster im letzten Jahr (Thread: Biotech Depot 2007)? 2008 ist schon halb rum... daher nun nach dem katastrophalen Biotech-Depot 2007 sehr verspätet nun wieder das neue Depot der reinen Biotechs 2008!

- Neues Jahr neues Glück?

- Neues Jahr neues Glück?

Die einzige Lehre, die ich aus dem letzten Jahr ziehen kann: nie wieder eine so große Position auf einen Wert konzentrieren, speziell wenn es sich dabei um ein Ein-Produkt-Unternehmen handelt. Daher orientiere ich mich seitdem an den mittleren, bereits etwas teureren Biotechs, die entweder bereits profitabel sind oder eine breite Pipeline besitzen, viel Cash, hohe Investitionen in die Entwicklung, Produkte möglichst weit in der klinischen Entwicklung, potentielle Blockbuster und namhafte Partner. Zudem soll das Depot eine höhere Streuung erhalten. Der zurückliegende Monat ist ausnahmsweise mal sehr positiv gelaufen, so dass ich es wage, einen entsprechenden Thread zu meinen Biotech-Werten zu erstellen.

So sieht es aktuell im Depot aus:

24,3% Genmab http://finance.yahoo.com/q?s=GEN.CO

15,4% Regeneron http://finance.yahoo.com/q?s=REGN

9,5% Onyx http://finance.yahoo.com/q?s=ONXX

7,2% OSI Pharma http://finance.yahoo.com/q?s=OSIP

6,3% (KO) Intercell http://finance.yahoo.com/q?s=IJE.F

5,4% Vertex http://finance.yahoo.com/q?s=VRTX

5,3% Cubist http://finance.yahoo.com/q?s=CBST

5,1% Imclone http://finance.yahoo.com/q?s=IMCL

5,1% Evotec http://finance.yahoo.com/q?s=EVT.DE

4,8% Isis http://finance.yahoo.com/q?s=ISIS

4,0% Arena http://finance.yahoo.com/q?s=ARNA

3,1% ViroPharma http://finance.yahoo.com/q?s=VPHM

2,7% Micromet http://finance.yahoo.com/q?s=MITI

1,9% Supergen http://finance.yahoo.com/q?s=SUPG

auf meiner Watchliste stehen INCY, RIGL und POZN. In der zweiten Reihe SGEN, Basilea, EXEL und MNTA.

Aus dem alten Depot ist nur noch Genmab und Arena übrig geblieben... GPC hat sich nahezu aufgelöst, MOR, POZN und CRME habe ich verkauft, während Speedel kürzlich übernommen wurde.

Ich hoffe, dies wird ein besseres Jahr! Der NBI steht momentan gar nicht schlecht... kann sich aber auch schnell wieder ändern.

mfg ipollit

hier die zugehörigen Charts...

Genmab

Regeneron

Onyx

OSI Pharma

(KO) Intercell

Vertex

Cubist

Imclone

Evotec

Isis

Arena

ViroPharma

Micromet

Supergen

Genmab

Regeneron

Onyx

OSI Pharma

(KO) Intercell

Vertex

Cubist

Imclone

Evotec

Isis

Arena

ViroPharma

Micromet

Supergen

und die Watch-Liste...

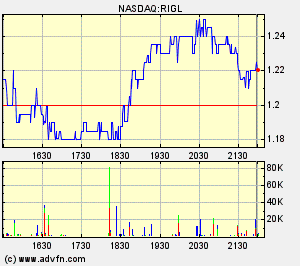

Incyte

Rigel

Pozen

mfg ipollit

Incyte

Rigel

Pozen

mfg ipollit

Genmab

http://www.genmab.com/

Marktkapitalisierung: 3,05 Mrd USD

Genmab ging aus Medarex hervor. Neben der AK-Technologie besitzt Genmab auch UniBody-AKs, die nur einen von zwei Armen besitzen, wodurch sich z.B. IgG4-AKs stabilisieren lassen. Außerdem besitzt Produktionsanlagen für die kommerzielle Herstellung von AKs.

die aktuelle Pipeline:

der wichtigste Kandidat ist Ofatumumab (Humax-CD20), der in einer 2 Mrd USD Kooperation zusammen mit GSK entwickelt wird. Ofatumumab ist eine humane Version von Rituxan. Die Indikationen sind demnach Blutkrebsarten wie CLL oder NHL, sowie Rheumatische Arthritis. Angepeilte peak sales sind bis zu mehrere Mrd USD.

Zalutumumab ist eine humane Version des Antikörpers Erbitux.

29.05.2008 | 11:45 Uhr

Genmab meldet Ergebnisse für das erste Quartal 2008

Kopenhagen (ots/PRNewswire) - - Zusammenfassung: Genmab meldet Ergebnisse für die ersten drei Monate des Jahres 2008

Genmab A/S (OMX: GEN) gab heute die Ergebnisse für das Quartal zum 31. März 2008 bekannt. Für diesen Zeitraum meldete Genmab die folgenden Ergebnisse:

Der Umsatz von Genmab lag für das erste Quartal 2008 bei 167 Mio. DKK (ca. 36 Mio. USD). Während des Vergleichszeitraums im Jahr 2007 erwirtschaftete Genmab einen Umsatz von 80 Mio. DKK (ca. 17 Mio. USD).

Der operative Verlust beläuft sich auf 197 Mio. DKK (ca. 42 Mio. USD). Verglichen hiermit lag der operative Verlust für den gleichen Zeitraum des Jahres 2007 bei 106 Mio. DKK (ca. 22 Mio. USD).

Im Nettofinanzertrag für das erste Quartal 2008 ist ein Nettoverlust von 14 Mio. DKK (ca. 3 Mio. USD) enthalten, verglichen mit einem Nettoertrag von 29 Mio. DKK (ca. 6 Mio. USD) im gleichen Zeitraum des Jahres 2007. Das Nettofinanzergebnis setzt sich einerseits zusammen aus den positiven Zinserträgen aus unseren Portfolios börsengängiger Wertpapiere, andererseits spiegeln sich darin die nicht realisierten Devisenverluste wider, die als Folge der anhaltenden Schwächung des US-Dollars gegenüber der Dänischen Krone im ersten Quartal 2008 entstanden sind.

Der Nettoverlust beläuft sich auf 210 Mio. DKK (ca. 45 Mio. USD), gegenüber einem Nettoverlust von 77 Mio. DKK (ca. 16 Mio. USD) im gleichen Zeitraum des Jahres 2007. Der Nettoverlust je Aktie belief sich im ersten Quartal 2008 auf 4,73 DKK (ca. 1,00 USD), verglichen mit 1,81 DKK (ca. 0,38 USD) im ersten Quartal 2007.

Genmab verzeichnete zum Ende des ersten Quartals einen Barmittelbestand von 2,4 Mrd. DKK (ca. 503 Mio. USD). Dies entspricht einem Rückgang um 1,3 Mrd. DKK (ca. 280 Mio. USD) gegenüber dem Bestand zum Ende des Jahres 2007. Der Rückgang ist dabei hauptsächlich auf den Kauf einer Produktionsanlage für 1,2 Mrd. DKK (ca. 240 Mio. USD zum Zeitpunkt des Kaufs) im März 2008 zurückzuführen.

Höhepunkte: Im Verlauf des ersten Quartals 2008 konnte Genmab etliche geschäftliche und wissenschaftliche Meilensteine erreichen, u.a.:

Im März erwarb Genmab eine Antikörper-Produktionsanlage von PDL BioPharma zum Preis von 1,2 Mrd. DKK (240 Mio. USD zum Zeitpunkt des Kaufs).

Im Januar meldete Genmab die Entwicklung eines neuen vorklinischen Produkts namens HuMax-CD32b. Der Antikörper könnte möglicherweise über therapeutisches Potenzial bei der Behandlung chronischer lymphatischer B-Zellen-Leukämie, kleinzelliger lymphatischer Lymphome, Burkitt-Lymphome, follikulärer Lymphome und diffuser grosszelliger B-Zellen-Lymphome verfügen.

Im Rahmen der Zusammenarbeit mit GlaxoSmithKline erreichten wir im Januar den dritten Meilenstein, als der erste Patient im Rahmen des Phase-III-RA-Programms behandelt wurde und wir eine Zahlung über 87 Mio. DKK (ca. 18 Mio. USD) erhielten.

Ausblick: Genmab behält seine Finanzprognose für das Jahr bei und erwartet weiterhin einen operativen Verlust von 900 Mio. bis 1 Mrd. DKK (ca. 187 bis 208 Mio. USD)sowie einen Nettoverlust im Bereich von 800 bis 900 Mio. DKK (ca. 167 bis 187 Mio. USD). Es wird erwartet, dass der Umsatz für 2008 ca. 1,0 Mrd. DKK (ca. 208 Mio. USD) betragen wird.

Zum Stichtag 31. Dezember 2007 verfügte Genmab über Barmittel und befristete börsengängige Wertpapiere in Höhe von 3,7 Mrd. DKK. Für 2008 erwarten wir, dass sich durch unsere Geschäftstätigkeiten sowie durch den Kauf der Produktionsanlage in Minnesota für 1,2 Mrd. DKK eine Barliquidität von 1,7 bis 1,8 Mrd. DKK (ca. 360 Mio. bis 382 Mio. USD) zum Jahresende ergibt.

mfg ipollit

http://www.genmab.com/

Marktkapitalisierung: 3,05 Mrd USD

Genmab ging aus Medarex hervor. Neben der AK-Technologie besitzt Genmab auch UniBody-AKs, die nur einen von zwei Armen besitzen, wodurch sich z.B. IgG4-AKs stabilisieren lassen. Außerdem besitzt Produktionsanlagen für die kommerzielle Herstellung von AKs.

die aktuelle Pipeline:

der wichtigste Kandidat ist Ofatumumab (Humax-CD20), der in einer 2 Mrd USD Kooperation zusammen mit GSK entwickelt wird. Ofatumumab ist eine humane Version von Rituxan. Die Indikationen sind demnach Blutkrebsarten wie CLL oder NHL, sowie Rheumatische Arthritis. Angepeilte peak sales sind bis zu mehrere Mrd USD.

Zalutumumab ist eine humane Version des Antikörpers Erbitux.

29.05.2008 | 11:45 Uhr

Genmab meldet Ergebnisse für das erste Quartal 2008

Kopenhagen (ots/PRNewswire) - - Zusammenfassung: Genmab meldet Ergebnisse für die ersten drei Monate des Jahres 2008

Genmab A/S (OMX: GEN) gab heute die Ergebnisse für das Quartal zum 31. März 2008 bekannt. Für diesen Zeitraum meldete Genmab die folgenden Ergebnisse:

Der Umsatz von Genmab lag für das erste Quartal 2008 bei 167 Mio. DKK (ca. 36 Mio. USD). Während des Vergleichszeitraums im Jahr 2007 erwirtschaftete Genmab einen Umsatz von 80 Mio. DKK (ca. 17 Mio. USD).

Der operative Verlust beläuft sich auf 197 Mio. DKK (ca. 42 Mio. USD). Verglichen hiermit lag der operative Verlust für den gleichen Zeitraum des Jahres 2007 bei 106 Mio. DKK (ca. 22 Mio. USD).

Im Nettofinanzertrag für das erste Quartal 2008 ist ein Nettoverlust von 14 Mio. DKK (ca. 3 Mio. USD) enthalten, verglichen mit einem Nettoertrag von 29 Mio. DKK (ca. 6 Mio. USD) im gleichen Zeitraum des Jahres 2007. Das Nettofinanzergebnis setzt sich einerseits zusammen aus den positiven Zinserträgen aus unseren Portfolios börsengängiger Wertpapiere, andererseits spiegeln sich darin die nicht realisierten Devisenverluste wider, die als Folge der anhaltenden Schwächung des US-Dollars gegenüber der Dänischen Krone im ersten Quartal 2008 entstanden sind.

Der Nettoverlust beläuft sich auf 210 Mio. DKK (ca. 45 Mio. USD), gegenüber einem Nettoverlust von 77 Mio. DKK (ca. 16 Mio. USD) im gleichen Zeitraum des Jahres 2007. Der Nettoverlust je Aktie belief sich im ersten Quartal 2008 auf 4,73 DKK (ca. 1,00 USD), verglichen mit 1,81 DKK (ca. 0,38 USD) im ersten Quartal 2007.

Genmab verzeichnete zum Ende des ersten Quartals einen Barmittelbestand von 2,4 Mrd. DKK (ca. 503 Mio. USD). Dies entspricht einem Rückgang um 1,3 Mrd. DKK (ca. 280 Mio. USD) gegenüber dem Bestand zum Ende des Jahres 2007. Der Rückgang ist dabei hauptsächlich auf den Kauf einer Produktionsanlage für 1,2 Mrd. DKK (ca. 240 Mio. USD zum Zeitpunkt des Kaufs) im März 2008 zurückzuführen.

Höhepunkte: Im Verlauf des ersten Quartals 2008 konnte Genmab etliche geschäftliche und wissenschaftliche Meilensteine erreichen, u.a.:

Im März erwarb Genmab eine Antikörper-Produktionsanlage von PDL BioPharma zum Preis von 1,2 Mrd. DKK (240 Mio. USD zum Zeitpunkt des Kaufs).

Im Januar meldete Genmab die Entwicklung eines neuen vorklinischen Produkts namens HuMax-CD32b. Der Antikörper könnte möglicherweise über therapeutisches Potenzial bei der Behandlung chronischer lymphatischer B-Zellen-Leukämie, kleinzelliger lymphatischer Lymphome, Burkitt-Lymphome, follikulärer Lymphome und diffuser grosszelliger B-Zellen-Lymphome verfügen.

Im Rahmen der Zusammenarbeit mit GlaxoSmithKline erreichten wir im Januar den dritten Meilenstein, als der erste Patient im Rahmen des Phase-III-RA-Programms behandelt wurde und wir eine Zahlung über 87 Mio. DKK (ca. 18 Mio. USD) erhielten.

Ausblick: Genmab behält seine Finanzprognose für das Jahr bei und erwartet weiterhin einen operativen Verlust von 900 Mio. bis 1 Mrd. DKK (ca. 187 bis 208 Mio. USD)sowie einen Nettoverlust im Bereich von 800 bis 900 Mio. DKK (ca. 167 bis 187 Mio. USD). Es wird erwartet, dass der Umsatz für 2008 ca. 1,0 Mrd. DKK (ca. 208 Mio. USD) betragen wird.

Zum Stichtag 31. Dezember 2007 verfügte Genmab über Barmittel und befristete börsengängige Wertpapiere in Höhe von 3,7 Mrd. DKK. Für 2008 erwarten wir, dass sich durch unsere Geschäftstätigkeiten sowie durch den Kauf der Produktionsanlage in Minnesota für 1,2 Mrd. DKK eine Barliquidität von 1,7 bis 1,8 Mrd. DKK (ca. 360 Mio. bis 382 Mio. USD) zum Jahresende ergibt.

mfg ipollit

Was aber der Evotec Schrott darin zu suchen hat, erschließt sich mir net. Evotec wird sterben wie GPC.

Ansonsten auf alle Fälle Adolor Corp (ADLR)..

Und Alnylam (ALNY) gehört eigentlich auch rein! Jedenfalls wenn Isis dabei ist.

Herz5!

Ansonsten auf alle Fälle Adolor Corp (ADLR)..

Und Alnylam (ALNY) gehört eigentlich auch rein! Jedenfalls wenn Isis dabei ist.

Herz5!

Trading Spotlight

Antwort auf Beitrag Nr.: 34.639.011 von ipollit am 03.08.08 19:38:58aktuell positive PIII-Daten von HuMax-CD20 bei CLL... Ziel war eine Ansprechrate von 25%, erreicht wurde eine deutlich höhere. Damit wäre eine Zulassung für diese erste Indikation im nächsten Jahr möglich.

***********

01.08.2008 | 14:30 Uhr

Genmab und GlaxoSmithKline melden positive Top-Line-Ergebnisse der Pivotstudie mit Ofatumumab zur Behandlung von chronischer lymphatischer Leukämie

Kopenhagen (ots/PRNewswire) - - Zusammenfassung: Pivotstudie der Phase III für Ofatumumab bei refraktärer CLL erreicht primären Endpunkt

Genmab A/S (OMX: GEN) und GlaxoSmithKline (LSE und NYSE: GSK) meldeten heute, dass eine vorläufige Analyse der Pivotstudie der Phase III positive Ergebnisse der wesentlichen Eckpunkte (Top-Line-Ergebnisse) ergeben hätte. Im Rahmen der Studie wurde der Einsatz von Ofatumumab (HuMax-CD20(R)) bei der Behandlung von zwei Patientengruppen mit chronischer lymphatischer Leukämie (CLL) bewertet, für die es bisher kaum Therapieoptionen gibt. Zum Zeitpunkt der vorläufigen Analyse wurde bei beiden Populationen der primäre Endpunkt der Studie erreicht; auch die Ergebnisse der sekundären Endpunkte unterstützen den primären Endpunkt.

In dieser vorläufigen Analyse wurde die Aktivität von Ofatumumab bei 154 Patienten bewertet; bei 138 dieser Patienten mit refraktärer CLL waren die Ergebnisse tatsächlich auswertbar. Etwa die Hälfte der an der Studie teilnehmenden Patienten (59) waren sowohl für Fludarabin als auch für Alemtuzumab refraktär. Im Rahmen der Analyse wurde auch eine zweite Gruppe (79) untersucht, die Fludarabin-refraktär waren und aufgrund grosser Tumore in den Lymphknoten als ungeeignete Kandidaten für Alemtuzumab angesehen wurden. In der Patientengruppe, die sowohl Fludarabin- als auch Alemtuzumab-refraktär waren, wurde eine objektive Ansprechrate von 51 % (p < 0.0001), bestehend aus 30 partiellen Reaktionen (PR), erreicht. In der Fludarabin-refraktären und für Alemtuzumab ungeeigneten Patientengruppe wurde eine objektive Ansprechrate von 44 % (p < 0.0001), darunter 1 vollständige Reaktion (CR) und 34 PR, festgestellt. Dass diese objektiven Ansprechraten, wie festgestellt erreicht wurden, geht aus Bewertungen eines unabhängigen Komitees hervor und unterliegt der Prüfung und Bestätigung durch die Zulassungsbehörden.

Ofatumumab wurde von CLL-Patienten in der Studie im Allgemeinen gut vertragen. Die am häufigsten festgestellten Nebenwirkungen (mit einer Häufigkeit von mehr als 15 %) waren: Pyrexie, Durchfall, Müdigkeit, Husten, Neutropenie, Anämie und Pneumonie. Es traten keine unerwarteten Sicherheitsrisiken auf. Bei keinem der 14 auf humane Antihuman-Antikörper (HAHA) getesteten Patienten wurden diese 12 Monate später nachgewiesen.

Eine Vorbesprechung zur Biologics License Application (BLA) wurde bei der FDA beantragt, bei der diese Ergebnisse erörtert werden sollen, so dass möglicherweise schon 2008 eine BLA eingereicht werden kann. Auch eine Einreichung bei den Zulassungsbehörden der EU kann möglicherweise im selben Zeitrahmen realisiert werden. Die vollständigen Daten werden zu gegebener Zeit im Rahmen einer wissenschaftlichen Fachkonferenz vorgestellt werden.

"Wir sind sehr erfreut, positive Ergebnisse bezüglich der Behandlung der an dieser Studie teilnehmenden CLL-Patienten bekannt geben zu können", so Dr. Lisa N. Drakeman, Chief Executive Officer von Genmab. "Auch für Genmab ist dies ein bedeutender Schritt. Wir stehen nun kurz vor der Einreichung des ersten Antrags auf Marktzulassung für einen Genmab-Antikörper und freuen uns darauf, bei der Einreichung der Unterlagen mit GSK zusammenzuarbeiten."

"Diese sehr vielversprechenden Ergebnisse weisen darauf hin, dass Ofatumumab das Potenzial hat, CLL-Patienten mit einer äusserst refraktären Erkrankung und eingeschränkten Behandlungsmöglichkeiten Vorteile zu bieten", sagte Kathy Rouan, Vice President und Leiterin der Medizinischen Entwicklung bei GSK. "GSK und Genmab arbeiten gemeinsam an einem umfassenden Entwicklungsprogramm für CLL und für Nicht-Hodgkins-Lymphome (NHL). Wir hoffen, dass diese sowohl für Patienten als auch für deren Ärzte einen bedeutenden Beitrag zur Behandlung dieser bösartigen hämatologischen Tumoren leisten werden."

Ofatumumab ist ein in der Entwicklung befindlicher, vollständig humaner, monoklonaler Antikörper der nächsten Generation, der sich an das kleine Schleifen-Epitop (spezifische Antikörper-Bindungsposition) auf dem CD20-Rezeptor auf der Oberfläche von B-Zellen bindet. Im Rahmen einer Vereinbarung zwischen Genmab und GlaxoSmithKline zur gemeinsamen Entwicklung und Vermarktung von Ofatumumab wird dieser Wirkstoff derzeit zur Behandlung der CLL, des follikulären Nicht-Hodgkin-Lymphoms, des diffusen grosszelligen B-Zellen-Lymphoms, der rheumatoiden Arthritis und der rezidivierenden, remittierenden multiplen Sklerose entwickelt. Ofatumumab ist bisher noch in keinem Land zugelassen.

mfg ipollit

***********

01.08.2008 | 14:30 Uhr

Genmab und GlaxoSmithKline melden positive Top-Line-Ergebnisse der Pivotstudie mit Ofatumumab zur Behandlung von chronischer lymphatischer Leukämie

Kopenhagen (ots/PRNewswire) - - Zusammenfassung: Pivotstudie der Phase III für Ofatumumab bei refraktärer CLL erreicht primären Endpunkt

Genmab A/S (OMX: GEN) und GlaxoSmithKline (LSE und NYSE: GSK) meldeten heute, dass eine vorläufige Analyse der Pivotstudie der Phase III positive Ergebnisse der wesentlichen Eckpunkte (Top-Line-Ergebnisse) ergeben hätte. Im Rahmen der Studie wurde der Einsatz von Ofatumumab (HuMax-CD20(R)) bei der Behandlung von zwei Patientengruppen mit chronischer lymphatischer Leukämie (CLL) bewertet, für die es bisher kaum Therapieoptionen gibt. Zum Zeitpunkt der vorläufigen Analyse wurde bei beiden Populationen der primäre Endpunkt der Studie erreicht; auch die Ergebnisse der sekundären Endpunkte unterstützen den primären Endpunkt.

In dieser vorläufigen Analyse wurde die Aktivität von Ofatumumab bei 154 Patienten bewertet; bei 138 dieser Patienten mit refraktärer CLL waren die Ergebnisse tatsächlich auswertbar. Etwa die Hälfte der an der Studie teilnehmenden Patienten (59) waren sowohl für Fludarabin als auch für Alemtuzumab refraktär. Im Rahmen der Analyse wurde auch eine zweite Gruppe (79) untersucht, die Fludarabin-refraktär waren und aufgrund grosser Tumore in den Lymphknoten als ungeeignete Kandidaten für Alemtuzumab angesehen wurden. In der Patientengruppe, die sowohl Fludarabin- als auch Alemtuzumab-refraktär waren, wurde eine objektive Ansprechrate von 51 % (p < 0.0001), bestehend aus 30 partiellen Reaktionen (PR), erreicht. In der Fludarabin-refraktären und für Alemtuzumab ungeeigneten Patientengruppe wurde eine objektive Ansprechrate von 44 % (p < 0.0001), darunter 1 vollständige Reaktion (CR) und 34 PR, festgestellt. Dass diese objektiven Ansprechraten, wie festgestellt erreicht wurden, geht aus Bewertungen eines unabhängigen Komitees hervor und unterliegt der Prüfung und Bestätigung durch die Zulassungsbehörden.

Ofatumumab wurde von CLL-Patienten in der Studie im Allgemeinen gut vertragen. Die am häufigsten festgestellten Nebenwirkungen (mit einer Häufigkeit von mehr als 15 %) waren: Pyrexie, Durchfall, Müdigkeit, Husten, Neutropenie, Anämie und Pneumonie. Es traten keine unerwarteten Sicherheitsrisiken auf. Bei keinem der 14 auf humane Antihuman-Antikörper (HAHA) getesteten Patienten wurden diese 12 Monate später nachgewiesen.

Eine Vorbesprechung zur Biologics License Application (BLA) wurde bei der FDA beantragt, bei der diese Ergebnisse erörtert werden sollen, so dass möglicherweise schon 2008 eine BLA eingereicht werden kann. Auch eine Einreichung bei den Zulassungsbehörden der EU kann möglicherweise im selben Zeitrahmen realisiert werden. Die vollständigen Daten werden zu gegebener Zeit im Rahmen einer wissenschaftlichen Fachkonferenz vorgestellt werden.

"Wir sind sehr erfreut, positive Ergebnisse bezüglich der Behandlung der an dieser Studie teilnehmenden CLL-Patienten bekannt geben zu können", so Dr. Lisa N. Drakeman, Chief Executive Officer von Genmab. "Auch für Genmab ist dies ein bedeutender Schritt. Wir stehen nun kurz vor der Einreichung des ersten Antrags auf Marktzulassung für einen Genmab-Antikörper und freuen uns darauf, bei der Einreichung der Unterlagen mit GSK zusammenzuarbeiten."

"Diese sehr vielversprechenden Ergebnisse weisen darauf hin, dass Ofatumumab das Potenzial hat, CLL-Patienten mit einer äusserst refraktären Erkrankung und eingeschränkten Behandlungsmöglichkeiten Vorteile zu bieten", sagte Kathy Rouan, Vice President und Leiterin der Medizinischen Entwicklung bei GSK. "GSK und Genmab arbeiten gemeinsam an einem umfassenden Entwicklungsprogramm für CLL und für Nicht-Hodgkins-Lymphome (NHL). Wir hoffen, dass diese sowohl für Patienten als auch für deren Ärzte einen bedeutenden Beitrag zur Behandlung dieser bösartigen hämatologischen Tumoren leisten werden."

Ofatumumab ist ein in der Entwicklung befindlicher, vollständig humaner, monoklonaler Antikörper der nächsten Generation, der sich an das kleine Schleifen-Epitop (spezifische Antikörper-Bindungsposition) auf dem CD20-Rezeptor auf der Oberfläche von B-Zellen bindet. Im Rahmen einer Vereinbarung zwischen Genmab und GlaxoSmithKline zur gemeinsamen Entwicklung und Vermarktung von Ofatumumab wird dieser Wirkstoff derzeit zur Behandlung der CLL, des follikulären Nicht-Hodgkin-Lymphoms, des diffusen grosszelligen B-Zellen-Lymphoms, der rheumatoiden Arthritis und der rezidivierenden, remittierenden multiplen Sklerose entwickelt. Ofatumumab ist bisher noch in keinem Land zugelassen.

mfg ipollit

Antwort auf Beitrag Nr.: 34.639.011 von ipollit am 03.08.08 19:38:5801.07.2008 | 07:44 Uhr

Genmab erreicht Meilenstein in der Ofatumumab-Zusammenarbeit

Kopenhagen (ots/PRNewswire) - - Zusammenfassung: Genmab hat einen Meilenstein in seiner Ofatumumab-Zusammenarbeit mit GlaxoSmithKline erreicht.

Genmab A/S (OMX: GEN) hat heute bekannt gegeben, dass es im Rahmen seiner Zusammenarbeit mit GlaxoSmithKline (GSK) einen Entwicklungs-Meilenstein für Ofatumumab (HuMax-CD20(R)) erreicht hat. Eine Meilenstein-Zahlung von schätzungsweise 29 Millionen DKK (schätzungsweise 6 Millionen USD) wurde durch die Behandlung des ersten Patienten ausgelöst, der an der Phase II-Studie von Ofatumumab zur Behandlung von schubförmig remittierender Multipler Sklerose (RRMS) teilgenommen hat.

"Unsere Zusammenarbeit mit GSK macht weiter Fortschritte, da beide Unternehmen darauf hinarbeiten, neue Behandlungsmöglichkeiten für Patienten anzubieten", erklärte Lisa N. Drakeman, Ph.D., Geschäftsführerin von Genmab. "Wir freuen uns, in der ersten Studie von Ofatumumab bei RRMS, einer unberechenbaren und starke Einschränkungen mit sich bringenden Erkrankung, mit der Behandlung von Patienten zu beginnen."

Ofatumumab ist ein in der Entwicklung befindlicher, vollständig menschlicher, monoklonaler Antikörper der nächsten Generation, der sich an ein ausgeprägtes, kleines, schleifenförmiges Epitop auf dem CD20-Rezeptor auf der Oberfläche von B-Zellen bindet. Dieses Epitop unterscheidet sich von den anderen Anti-CD20-Antikörpern, die zurzeit verfügbar sind oder sich in der Entwicklung befinden. Ofatumumab wird im Rahmen einer gemeinsamen Entwicklungs- und Vermarktungsvereinbarung zwischen Genmab und GSK entwickelt.

mfg ipollit

Genmab erreicht Meilenstein in der Ofatumumab-Zusammenarbeit

Kopenhagen (ots/PRNewswire) - - Zusammenfassung: Genmab hat einen Meilenstein in seiner Ofatumumab-Zusammenarbeit mit GlaxoSmithKline erreicht.

Genmab A/S (OMX: GEN) hat heute bekannt gegeben, dass es im Rahmen seiner Zusammenarbeit mit GlaxoSmithKline (GSK) einen Entwicklungs-Meilenstein für Ofatumumab (HuMax-CD20(R)) erreicht hat. Eine Meilenstein-Zahlung von schätzungsweise 29 Millionen DKK (schätzungsweise 6 Millionen USD) wurde durch die Behandlung des ersten Patienten ausgelöst, der an der Phase II-Studie von Ofatumumab zur Behandlung von schubförmig remittierender Multipler Sklerose (RRMS) teilgenommen hat.

"Unsere Zusammenarbeit mit GSK macht weiter Fortschritte, da beide Unternehmen darauf hinarbeiten, neue Behandlungsmöglichkeiten für Patienten anzubieten", erklärte Lisa N. Drakeman, Ph.D., Geschäftsführerin von Genmab. "Wir freuen uns, in der ersten Studie von Ofatumumab bei RRMS, einer unberechenbaren und starke Einschränkungen mit sich bringenden Erkrankung, mit der Behandlung von Patienten zu beginnen."

Ofatumumab ist ein in der Entwicklung befindlicher, vollständig menschlicher, monoklonaler Antikörper der nächsten Generation, der sich an ein ausgeprägtes, kleines, schleifenförmiges Epitop auf dem CD20-Rezeptor auf der Oberfläche von B-Zellen bindet. Dieses Epitop unterscheidet sich von den anderen Anti-CD20-Antikörpern, die zurzeit verfügbar sind oder sich in der Entwicklung befinden. Ofatumumab wird im Rahmen einer gemeinsamen Entwicklungs- und Vermarktungsvereinbarung zwischen Genmab und GSK entwickelt.

mfg ipollit

Antwort auf Beitrag Nr.: 34.639.023 von -Salem- am 03.08.08 19:45:12Richtig, Alnylam habe ich auch auf meiner Liste gehabt, war mir dann aber doch zu teuer (1,44 Mrd USD MK!!!). Angeblich sollen sie zwar das Maß bezüglich RNAi sein, aber ob diese Technologie wirklich die Wunderwaffe ist, muss sich noch zeigen. Über 1 Mrd USD MK und so gut wie nichts in der klinischen Pipeline riecht mir etwas zu sehr nach Hype.

Statt ADLR würde ich eher PGNX nehmen, oder?

Evotec? Ist für mich im Moment der einzige deutsche Biotech, der interessant ist. Halte ich für äußerst vielversprechend mit einer spannenden CNS-Pipeline: u.a. Schlafmittel, Raucherentwöhnungsmittel und Alzheimer-Medikament... alles potentielle Blockbuster, teilweise schon mit POC. Und ausreichend Cash für die nächste Zeit.

mfg ipollit

Statt ADLR würde ich eher PGNX nehmen, oder?

Evotec? Ist für mich im Moment der einzige deutsche Biotech, der interessant ist. Halte ich für äußerst vielversprechend mit einer spannenden CNS-Pipeline: u.a. Schlafmittel, Raucherentwöhnungsmittel und Alzheimer-Medikament... alles potentielle Blockbuster, teilweise schon mit POC. Und ausreichend Cash für die nächste Zeit.

mfg ipollit

Antwort auf Beitrag Nr.: 34.639.011 von ipollit am 03.08.08 19:38:58hier ein Überlick über potentiell anstehende Events in der nächsten Zeit: Die CLL PIII-Daten sind bereits bekannt.

•Ofatumumab: Phase III data for the CLL indication (expected in August 2008).

•Ofatumumab: Phase III data for the FL indication (expected in September/October 2008).

•Zalutumumab: Interim phase-III data for the head and neck cancer indication (expected in Q4 2008).

•Ofatumumab: Approval of the CLL indication (expected in Q4, 2008).

•Zalutumumab: Partnership agreement.

•Unibody: Technology update

•Unibody: Partnership agreement.

•Zanolimumab: Phase III data for the CTCL indication (expected in 2009, 2H).

mfg ipollit

•Ofatumumab: Phase III data for the CLL indication (expected in August 2008).

•Ofatumumab: Phase III data for the FL indication (expected in September/October 2008).

•Zalutumumab: Interim phase-III data for the head and neck cancer indication (expected in Q4 2008).

•Ofatumumab: Approval of the CLL indication (expected in Q4, 2008).

•Zalutumumab: Partnership agreement.

•Unibody: Technology update

•Unibody: Partnership agreement.

•Zanolimumab: Phase III data for the CTCL indication (expected in 2009, 2H).

mfg ipollit

Und warum fehlt Actelion?

Antwort auf Beitrag Nr.: 34.639.625 von Matze900 am 03.08.08 23:32:19Actelion... Weil ich nicht beurteilen konnte, welchen Einfluss Letairis und Thelin auf die Tracleer-Umsätze haben werden. Actelion ist von Tracleer noch ziemlich abhängig. Die MK ist mit 6,7 Mrd USD auch nicht so niedrig, dass es geradezu ein Schnäppchen ist. Werde ich mir aber nochmal genauer ansehen. Sollte Tracleer stabil wachsen, dann ist Actelion vor dem Hintergrund von Almorexant allerdings eine Investition wert.

mfg ipollit

mfg ipollit

Antwort auf Beitrag Nr.: 34.642.261 von ipollit am 04.08.08 13:21:45

Published: 07:00 04.08.2008 GMT+2 /HUGIN /Source: Actelion Pharmaceuticals Ltd /SWX: ATLN /ISIN: CH0010532478

Tracleer® (bosentan) receives EU approval for treatment of patients with mildly symptomatic Pulmonary Arterial Hypertension

ALLSCHWIL/BASEL, SWITZERLAND - 04 August 2008 - Actelion Ltd (SWX: ATLN) announced today that Tracleer® (bosentan), a dual endothelin receptor antagonist, has been approved in the European Union for the treatment of patients with mildly symptomatic pulmonary arterial hypertension (PAH WHO functional class FC II). Since 2002, Tracleer® has been approved and available in the European Union for PAH patients with WHO FC III.

Tracleer® is the first PAH treatment ever to be investigated in a clinical study that exclusively enrolled patients with mildly symptomatic WHO FC II. This 185-patient randomized, double-blind, placebo-controlled study provided the basis for this EU approval. The indication extension reads: "Some improvements have also been shown in patients with PAH WHO functional class II (see section 5.1)" 1

Jean-Paul Clozel, M.D. and Chief Executive Officer of Actelion, commented: "The EARLY study has demonstrated that even patients with mild symptoms are at risk of rapid deterioration. I am very proud that Actelion - together with the scientific community - has been able to demonstrate the important role of Tracleer® in delaying disease progression in these patients. Our dual endothelin receptor antagonist Tracleer® is the only PAH medicine to have demonstrated a delay in disease progression in three independent placebo-controlled, randomized clinical studies. Actelion will now communicate these important clinical findings to encourage early diagnosis and intervention."

The results from EARLY (Endothelin Antagonist tRial in miLdlY symptomatic PAH patients) published in "The Lancet" in June2, document the relentlessly progressive nature of PAH, even in its early stages, and highlight the need for earlier treatment and intervention in PAH management. The PAH progression was evident from the deterioration in all evaluated parameters in the placebo group, including the rate of clinical worsening events. The primary endpoints for the EARLY trial were changes in pulmonary vascular resistance (PVR) and exercise capacity as measured by a 6-minute walk test (6MWD). PAH progression was assessed by evaluating two secondary endpoints which were time to clinical worsening and change in WHO functional class.

The key results of the EARLY study were:

PVR improved significantly, with a reduction of 22.6 percent (p <0.0001) after six months of bosentan compared with placebo.

6MWD increased by a mean of 19 meters (p = 0.0758). Statistical significance was not seen in the 6MWD. However, this may reflect the fact that, on average, enrolled patients had a relatively well-preserved mean exercise capacity at baseline, which can be difficult to further improve.

A significant 77 percent risk reduction in time to clinical worsening (p = 0.011) was seen after six months of bosentan treatment compared with placebo. Time to clinical worsening was defined by symptomatic progression of PAH, hospitalization for PAH or death. Patients receiving bosentan had a lower incidence of worsening functional class (3.4 percent compared to 13.2 percent when receiving placebo,

p = 0.0285), providing further evidence of delayed PAH progression.

A subgroup of patients who received concomitant sildenafil showed improvements in PVR and 6MWD consistent with the overall results.

The safety and tolerability profile of bosentan in the EARLY study was consistent with that observed in previous placebo-controlled clinical trials.3,4

There are four WHO functional classes (FC) for PAH with class I being the least severe and class IV being the most advanced. These reflect the impact on a patient's life in terms of symptoms and physical activity. WHO FC II patients are defined as patients with PAH resulting in slight limitation of physical activity, they are comfortable at rest and ordinary physical activity causes undue dyspnea or fatigue, chest pain or near syncope.5 Despite being mildly symptomatic, these patients still suffer from a severe and rapidly progressive disease.

Regulatory proceedings to extend the label for bosentan to include PAH patients in WHO FC II are ongoing in the US and other territories worldwide.

###

About Pulmonary Arterial Hypertension (PAH)

PAH is a syndrome characterized by a progressive increase in pulmonary vascular resistance (PVR) leading to right ventricular failure and premature death.6 If untreated, PAH carries a very poor prognosis with a median survival of 2.8 years after diagnosis.7

There are four WHO functional classes for PAH with class I being the least severe and class IV being the most advanced. These reflect the impact on a patient's life in terms of symptoms and physical activity. Class II patients are defined as patients with pulmonary hypertension resulting in mild limitation of physical activity, they are comfortable at rest and ordinary physical activity causes undue dyspnea or fatigue, chest pain or near syncope.5

The pathogenesis of PAH involves the increased production of vasoactive compounds, such as endothelin. Endothelin is produced by the endothelial cells and is essential for maintenance of normal vascular tone and function. Tracleer® was the first in a new class of treatments for PAH known as endothelin receptor antagonists. Tracleer® is a dual antagonist as it blocks both ETA and ETB receptors preventing the deleterious effects of endothelin.

Online information on PAH is available at www.pah-info.com. PAH-info.com is part of an international PAH awareness campaign supported by Actelion Pharmaceuticals and has been created to provide information to healthcare professionals and patients.

About Tracleer® in Pulmonary Arterial Hypertension (PAH)

Tracleer® is an oral dual endothelin receptor antagonist, which is currently licensed for the treatment of PAH; in the United States in PAH Functional Class III and IV to improve exercise capacity and decrease the rate of clinical worsening and in Europe in PAH Functional Class III to improve exercise capacity and symptoms as well as PAH Functional Class II where some improvements have also been shown. In the EU, Tracleer® is also indicated to reduce the number of new digital ulcers in patients with systemic sclerosis and ongoing digital ulcer disease. Regulatory review for the inclusion of functional class II in the Tracleer® label is ongoing on a worldwide basis.

Tracleer® has been made commercially available by Actelion subsidiaries in the United States, the European Union, Japan, Australia, Canada, Switzerland and other markets worldwide since 2001. In these seven years of clinical experience, more than 50,000 patients have been treated with Tracleer®.

Other clinical studies with Tracleer® in specific patient populations

Actelion also conducted clinical trials to further describe the role of bosentan in treating PAH in specific patient populations, such as patients with congenital heart disease (with Eisenmenger syndrome; BREATHE-5) and patients infected with HIV (BREATHE-4). Study results are reflected in the Tracleer® product label. Clinical studies with bosentan in children suffering from PAH (BREATHE-3, FUTURE-1 and -2) have been conducted. A dedicated paediatric formulation with bosentan has been submitted to European Health Authority and is currently under assessment.

About Tracleer® in Digital Ulcers (DU)

DUs are a manifestation of the underlying vasculopathy which is central to the pathophysiology of systemic sclerosis (SSc) and pivotal in the development of PAH in SSc, one of the leading causes of death in SSc. Endothelin, a pathogenic mediator, is implicated in the underlying vasculopathy in SSc.

DUs can be a frequent, persistent and debilitating complication of SSc. They are caused by a reduction in the lumen of small bloody vessels that decreases blood flow to the fingers and toes causing open sores. DUs are painful, with a debilitating impact on patients' daily life, often making it impossible to work and undertake even simple day-to-day activities, particularly those associated with fingertip function. Reducing the occurrence of new DUs is an important and achievable treatment goal in SSc.

In the EU, Tracleer® is indicated to reduce the number of new digital ulcers in patients with systemic sclerosis and ongoing digital ulcer disease. Tracleer® has been shown to improve hand function (i.e. dressing and hygiene) in patients with scleroderma-induced digital ulcers.

Requires attention to two significant safety concerns: Potential for serious liver injury (including rare cases of liver failure and unexplained hepatic cirrhosis in a setting of close monitoring) - Liver monitoring of all patients is essential prior to initiation of treatment and monthly thereafter. High potential for major birth defects - pregnancy must be excluded and prevented by two forms of birth control; monthly pregnancy tests should be obtained. Because of these risks, Tracleer® is only supplied through a controlled distribution.

References

1. Tracleer® SPC

2. Galiè N, Rubin LJ, Hoeper MM et al. Treatment of patients with mildly symptomatic pulmonary arterial hypertension with bosentan (EARLY study): a double-blind, randomised controlled trial. Lancet 2008;371: 2093-2100.

3. Channick RN, Simonneau G, Sitbon O et al. Effects of the dual endothelin-receptor antagonist bosentan in patients with pulmonary hypertension: a randomised placebo-controlled study. Lancet 2001;358:1119-23 (Study 351).

4. Rubin LJ, Badesch DB, Barst RJ et al. Bosentan therapy for pulmonary arterial hypertension. NEJM 2002;346:896-903 (BREATHE-1).

5. Barst RJ, McGoon M, Torbicki A et al. Diagnosis and differential assessment of pulmonary arterial hypertension. J Am Coll Cardiol 2004;43 (Suppl S):40S-47S.

6. Sitbon O, Humbert M, Jais X et al. Long-term response to calcium channel blockers in idiopathic pulmonary arterial hypertension. Circulation 2005;111:3105-3111.

7. D'Alonzo GE, Barst RJ, Ayres SM et al. Survival in patients with primary pulmonary hypertension: Results from a national prospective registry. Ann Intern Med 1991;115:343-349.

Actelion Ltd

Actelion Ltd is a biopharmaceutical company with its corporate headquarters in Allschwil/Basel, Switzerland. Actelion's first drug Tracleer®, an orally available dual endothelin receptor antagonist, has been approved as a therapy for pulmonary arterial hypertension. Actelion markets Tracleer® through its own subsidiaries in key markets worldwide, including the United States (based in South San Francisco), the European Union, Japan, Canada, Australia and Switzerland. Actelion, founded in late 1997, is a leading player in innovative science related to the endothelium - the single layer of cells separating every blood vessel from the blood stream. Actelion's over 1700 employees focus on the discovery, development and marketing of innovative drugs for significant unmet medical needs. Actelion shares are traded on the SWX Swiss Exchange (ticker symbol: ATLN).

For further information please contact:

Medical Media Contact

Kris Matta-Noaman

Packer Forbes

+44 208 772 1551

kris@packerforbes.com

Investor Contact

Roland Haefeli

Vice President, Head of Investor Relations & Public Affairs

Actelion Pharmaceuticals Ltd, Gewerbestrasse 16, CH-4123 Allschwil

+41 61 565 62 62

+1 650 624 69 36

http://www.actelion.com

Published: 07:00 04.08.2008 GMT+2 /HUGIN /Source: Actelion Pharmaceuticals Ltd /SWX: ATLN /ISIN: CH0010532478

Tracleer® (bosentan) receives EU approval for treatment of patients with mildly symptomatic Pulmonary Arterial Hypertension

ALLSCHWIL/BASEL, SWITZERLAND - 04 August 2008 - Actelion Ltd (SWX: ATLN) announced today that Tracleer® (bosentan), a dual endothelin receptor antagonist, has been approved in the European Union for the treatment of patients with mildly symptomatic pulmonary arterial hypertension (PAH WHO functional class FC II). Since 2002, Tracleer® has been approved and available in the European Union for PAH patients with WHO FC III.

Tracleer® is the first PAH treatment ever to be investigated in a clinical study that exclusively enrolled patients with mildly symptomatic WHO FC II. This 185-patient randomized, double-blind, placebo-controlled study provided the basis for this EU approval. The indication extension reads: "Some improvements have also been shown in patients with PAH WHO functional class II (see section 5.1)" 1

Jean-Paul Clozel, M.D. and Chief Executive Officer of Actelion, commented: "The EARLY study has demonstrated that even patients with mild symptoms are at risk of rapid deterioration. I am very proud that Actelion - together with the scientific community - has been able to demonstrate the important role of Tracleer® in delaying disease progression in these patients. Our dual endothelin receptor antagonist Tracleer® is the only PAH medicine to have demonstrated a delay in disease progression in three independent placebo-controlled, randomized clinical studies. Actelion will now communicate these important clinical findings to encourage early diagnosis and intervention."

The results from EARLY (Endothelin Antagonist tRial in miLdlY symptomatic PAH patients) published in "The Lancet" in June2, document the relentlessly progressive nature of PAH, even in its early stages, and highlight the need for earlier treatment and intervention in PAH management. The PAH progression was evident from the deterioration in all evaluated parameters in the placebo group, including the rate of clinical worsening events. The primary endpoints for the EARLY trial were changes in pulmonary vascular resistance (PVR) and exercise capacity as measured by a 6-minute walk test (6MWD). PAH progression was assessed by evaluating two secondary endpoints which were time to clinical worsening and change in WHO functional class.

The key results of the EARLY study were:

PVR improved significantly, with a reduction of 22.6 percent (p <0.0001) after six months of bosentan compared with placebo.

6MWD increased by a mean of 19 meters (p = 0.0758). Statistical significance was not seen in the 6MWD. However, this may reflect the fact that, on average, enrolled patients had a relatively well-preserved mean exercise capacity at baseline, which can be difficult to further improve.

A significant 77 percent risk reduction in time to clinical worsening (p = 0.011) was seen after six months of bosentan treatment compared with placebo. Time to clinical worsening was defined by symptomatic progression of PAH, hospitalization for PAH or death. Patients receiving bosentan had a lower incidence of worsening functional class (3.4 percent compared to 13.2 percent when receiving placebo,

p = 0.0285), providing further evidence of delayed PAH progression.

A subgroup of patients who received concomitant sildenafil showed improvements in PVR and 6MWD consistent with the overall results.

The safety and tolerability profile of bosentan in the EARLY study was consistent with that observed in previous placebo-controlled clinical trials.3,4

There are four WHO functional classes (FC) for PAH with class I being the least severe and class IV being the most advanced. These reflect the impact on a patient's life in terms of symptoms and physical activity. WHO FC II patients are defined as patients with PAH resulting in slight limitation of physical activity, they are comfortable at rest and ordinary physical activity causes undue dyspnea or fatigue, chest pain or near syncope.5 Despite being mildly symptomatic, these patients still suffer from a severe and rapidly progressive disease.

Regulatory proceedings to extend the label for bosentan to include PAH patients in WHO FC II are ongoing in the US and other territories worldwide.

###

About Pulmonary Arterial Hypertension (PAH)

PAH is a syndrome characterized by a progressive increase in pulmonary vascular resistance (PVR) leading to right ventricular failure and premature death.6 If untreated, PAH carries a very poor prognosis with a median survival of 2.8 years after diagnosis.7

There are four WHO functional classes for PAH with class I being the least severe and class IV being the most advanced. These reflect the impact on a patient's life in terms of symptoms and physical activity. Class II patients are defined as patients with pulmonary hypertension resulting in mild limitation of physical activity, they are comfortable at rest and ordinary physical activity causes undue dyspnea or fatigue, chest pain or near syncope.5

The pathogenesis of PAH involves the increased production of vasoactive compounds, such as endothelin. Endothelin is produced by the endothelial cells and is essential for maintenance of normal vascular tone and function. Tracleer® was the first in a new class of treatments for PAH known as endothelin receptor antagonists. Tracleer® is a dual antagonist as it blocks both ETA and ETB receptors preventing the deleterious effects of endothelin.

Online information on PAH is available at www.pah-info.com. PAH-info.com is part of an international PAH awareness campaign supported by Actelion Pharmaceuticals and has been created to provide information to healthcare professionals and patients.

About Tracleer® in Pulmonary Arterial Hypertension (PAH)

Tracleer® is an oral dual endothelin receptor antagonist, which is currently licensed for the treatment of PAH; in the United States in PAH Functional Class III and IV to improve exercise capacity and decrease the rate of clinical worsening and in Europe in PAH Functional Class III to improve exercise capacity and symptoms as well as PAH Functional Class II where some improvements have also been shown. In the EU, Tracleer® is also indicated to reduce the number of new digital ulcers in patients with systemic sclerosis and ongoing digital ulcer disease. Regulatory review for the inclusion of functional class II in the Tracleer® label is ongoing on a worldwide basis.

Tracleer® has been made commercially available by Actelion subsidiaries in the United States, the European Union, Japan, Australia, Canada, Switzerland and other markets worldwide since 2001. In these seven years of clinical experience, more than 50,000 patients have been treated with Tracleer®.

Other clinical studies with Tracleer® in specific patient populations

Actelion also conducted clinical trials to further describe the role of bosentan in treating PAH in specific patient populations, such as patients with congenital heart disease (with Eisenmenger syndrome; BREATHE-5) and patients infected with HIV (BREATHE-4). Study results are reflected in the Tracleer® product label. Clinical studies with bosentan in children suffering from PAH (BREATHE-3, FUTURE-1 and -2) have been conducted. A dedicated paediatric formulation with bosentan has been submitted to European Health Authority and is currently under assessment.

About Tracleer® in Digital Ulcers (DU)

DUs are a manifestation of the underlying vasculopathy which is central to the pathophysiology of systemic sclerosis (SSc) and pivotal in the development of PAH in SSc, one of the leading causes of death in SSc. Endothelin, a pathogenic mediator, is implicated in the underlying vasculopathy in SSc.

DUs can be a frequent, persistent and debilitating complication of SSc. They are caused by a reduction in the lumen of small bloody vessels that decreases blood flow to the fingers and toes causing open sores. DUs are painful, with a debilitating impact on patients' daily life, often making it impossible to work and undertake even simple day-to-day activities, particularly those associated with fingertip function. Reducing the occurrence of new DUs is an important and achievable treatment goal in SSc.

In the EU, Tracleer® is indicated to reduce the number of new digital ulcers in patients with systemic sclerosis and ongoing digital ulcer disease. Tracleer® has been shown to improve hand function (i.e. dressing and hygiene) in patients with scleroderma-induced digital ulcers.

Requires attention to two significant safety concerns: Potential for serious liver injury (including rare cases of liver failure and unexplained hepatic cirrhosis in a setting of close monitoring) - Liver monitoring of all patients is essential prior to initiation of treatment and monthly thereafter. High potential for major birth defects - pregnancy must be excluded and prevented by two forms of birth control; monthly pregnancy tests should be obtained. Because of these risks, Tracleer® is only supplied through a controlled distribution.

References

1. Tracleer® SPC

2. Galiè N, Rubin LJ, Hoeper MM et al. Treatment of patients with mildly symptomatic pulmonary arterial hypertension with bosentan (EARLY study): a double-blind, randomised controlled trial. Lancet 2008;371: 2093-2100.

3. Channick RN, Simonneau G, Sitbon O et al. Effects of the dual endothelin-receptor antagonist bosentan in patients with pulmonary hypertension: a randomised placebo-controlled study. Lancet 2001;358:1119-23 (Study 351).

4. Rubin LJ, Badesch DB, Barst RJ et al. Bosentan therapy for pulmonary arterial hypertension. NEJM 2002;346:896-903 (BREATHE-1).

5. Barst RJ, McGoon M, Torbicki A et al. Diagnosis and differential assessment of pulmonary arterial hypertension. J Am Coll Cardiol 2004;43 (Suppl S):40S-47S.

6. Sitbon O, Humbert M, Jais X et al. Long-term response to calcium channel blockers in idiopathic pulmonary arterial hypertension. Circulation 2005;111:3105-3111.

7. D'Alonzo GE, Barst RJ, Ayres SM et al. Survival in patients with primary pulmonary hypertension: Results from a national prospective registry. Ann Intern Med 1991;115:343-349.

Actelion Ltd

Actelion Ltd is a biopharmaceutical company with its corporate headquarters in Allschwil/Basel, Switzerland. Actelion's first drug Tracleer®, an orally available dual endothelin receptor antagonist, has been approved as a therapy for pulmonary arterial hypertension. Actelion markets Tracleer® through its own subsidiaries in key markets worldwide, including the United States (based in South San Francisco), the European Union, Japan, Canada, Australia and Switzerland. Actelion, founded in late 1997, is a leading player in innovative science related to the endothelium - the single layer of cells separating every blood vessel from the blood stream. Actelion's over 1700 employees focus on the discovery, development and marketing of innovative drugs for significant unmet medical needs. Actelion shares are traded on the SWX Swiss Exchange (ticker symbol: ATLN).

For further information please contact:

Medical Media Contact

Kris Matta-Noaman

Packer Forbes

+44 208 772 1551

kris@packerforbes.com

Investor Contact

Roland Haefeli

Vice President, Head of Investor Relations & Public Affairs

Actelion Pharmaceuticals Ltd, Gewerbestrasse 16, CH-4123 Allschwil

+41 61 565 62 62

+1 650 624 69 36

http://www.actelion.com

Antwort auf Beitrag Nr.: 34.643.067 von Fruehrentner am 04.08.08 15:08:52off topic... nur eben, da ich Actelion nicht im Depot habe:

Zürich (aktiencheck.de AG) - Andrew C. Weiss, Analyst von Vontobel Research, bewertet die Aktie von Actelion (ISIN CH0010532478 / WKN 936767) in der aktuellen Ausgabe von "Vontobel Morning Focus" nach wie vor mit "hold".

Actelion habe heute Morgen bekannt gegeben, aufgrund der EARLY-Daten die Zulassung für Tracleer der Funktionsklasse II erhalten zu haben. Tracleer habe bereits die Zulassung für die Behandlung der Funktionsklasse III und IV-PAH-Patienten (Patienten mit leichter symptomatischer pulmonaler arterieller Hypertonie) erhalten. Das Pricing sei also bereits verhandelt worden.

Die EU-Zulassung sei erwartet worden, da das CHMP Ende Juni eine positive Stellungnahme abgegeben habe, aber die Zulassung erfolge etwas schneller als die Analysten gedacht hätten. Sie seien von einer EU-Zulassung im September 2008 ausgegangen.

Die Daten der EARLY-Studie seien im Juni 2008 in der Fachzeitschrift "The Lancet" veröffentlicht worden. Diese Studiendaten hätten dazu gedient, die Indikationserweiterung für Tracleer zu erhalten, und es sei die einzige Studie, die den Einsatz eines Endothelin-Rezeptor-Antagonisten (in diesem Fall Tracleer) ausschließlich bei PAH der Funktionsklasse II untersucht habe.

Mit dieser Zulassung erhalte Actelion Zugang zu einem neuen Pool möglicher Patienten, die eine PAH-Behandlung benötigen würden. Der Abnehmermarkt könnte sich möglicherweise verdoppeln. Aber da die Patienten nur leichte Symptome zeigen würden, werde es schwierig sein, diese neuen Patienten zu finden, eine solide ärztliche Ausbildung werde erforderlich sein. Die Analysten würden derzeit auf aktuelle Informationen von der US-Gesundheitsbehörde FDA bezüglich der EARLY-Daten zum Tracleer-Label warten.

Die Zulassung der EARLY-Daten für das Tracleer-Label sei weitherum erwartet worden. Die Analysten würden bezüglich Marktakzeptanz von Tracleer konservative Schätzungen machen, was einer langsamen Marktdurchdringung bei dieser Indikation entspreche, zumal das Finden von Patienten eine hohe ärztliche Ausbildung erfordere. Zuvor hätten sie auch von Gilead erwartet, dass der Konzern bei der Vermarktung von Letairis größere Anstrengungen unternehmen und so zur Markterweiterung von Actelion beitragen würde. Doch angesichts der schwachen Marketing-Unterstützung würden sie davon ausgehen, dass Actelion die meiste Knochenarbeit bei der ärztlichen Ausbildung selbst erledigen müsse.

mfg ipollit

Zürich (aktiencheck.de AG) - Andrew C. Weiss, Analyst von Vontobel Research, bewertet die Aktie von Actelion (ISIN CH0010532478 / WKN 936767) in der aktuellen Ausgabe von "Vontobel Morning Focus" nach wie vor mit "hold".

Actelion habe heute Morgen bekannt gegeben, aufgrund der EARLY-Daten die Zulassung für Tracleer der Funktionsklasse II erhalten zu haben. Tracleer habe bereits die Zulassung für die Behandlung der Funktionsklasse III und IV-PAH-Patienten (Patienten mit leichter symptomatischer pulmonaler arterieller Hypertonie) erhalten. Das Pricing sei also bereits verhandelt worden.

Die EU-Zulassung sei erwartet worden, da das CHMP Ende Juni eine positive Stellungnahme abgegeben habe, aber die Zulassung erfolge etwas schneller als die Analysten gedacht hätten. Sie seien von einer EU-Zulassung im September 2008 ausgegangen.

Die Daten der EARLY-Studie seien im Juni 2008 in der Fachzeitschrift "The Lancet" veröffentlicht worden. Diese Studiendaten hätten dazu gedient, die Indikationserweiterung für Tracleer zu erhalten, und es sei die einzige Studie, die den Einsatz eines Endothelin-Rezeptor-Antagonisten (in diesem Fall Tracleer) ausschließlich bei PAH der Funktionsklasse II untersucht habe.

Mit dieser Zulassung erhalte Actelion Zugang zu einem neuen Pool möglicher Patienten, die eine PAH-Behandlung benötigen würden. Der Abnehmermarkt könnte sich möglicherweise verdoppeln. Aber da die Patienten nur leichte Symptome zeigen würden, werde es schwierig sein, diese neuen Patienten zu finden, eine solide ärztliche Ausbildung werde erforderlich sein. Die Analysten würden derzeit auf aktuelle Informationen von der US-Gesundheitsbehörde FDA bezüglich der EARLY-Daten zum Tracleer-Label warten.

Die Zulassung der EARLY-Daten für das Tracleer-Label sei weitherum erwartet worden. Die Analysten würden bezüglich Marktakzeptanz von Tracleer konservative Schätzungen machen, was einer langsamen Marktdurchdringung bei dieser Indikation entspreche, zumal das Finden von Patienten eine hohe ärztliche Ausbildung erfordere. Zuvor hätten sie auch von Gilead erwartet, dass der Konzern bei der Vermarktung von Letairis größere Anstrengungen unternehmen und so zur Markterweiterung von Actelion beitragen würde. Doch angesichts der schwachen Marketing-Unterstützung würden sie davon ausgehen, dass Actelion die meiste Knochenarbeit bei der ärztlichen Ausbildung selbst erledigen müsse.

mfg ipollit

Regeneron - REGN

http://www.regeneron.com/

Marktkapitalisierung: 1,73 Mrd USD

Cash: 743 Mio USD

Schulden: 200 Mio USD

Umsatz 2008e/2009e: 222 / 240 Mio USD

Gewinn: (keine Gewinne)

zugelassene Produkte: ARCALYST

Partner: u.a. Sanofi Aventis (ist zu 19% an Regeneron beteiligt), Bayer

Technologien: AK, Trap

Regeneron ist eines der ältesten Biotechs ähnlich wie Amgen oder Genentech, war aber bei weitem nicht so erfolgreich.

Pipeline:

Aflibercept (VEGF-Trap):

Es handelt sich dabei um einen sogenannten Zytokin-Fänger (Trap), wenn ich das richtig übersetzt habe. Damit werden ähnlich wie mit z.B. Antikörpern Signalmoleküle eingefangen und somit davon abgehalten, ihren spezifischen Rezeptor zu aktivieren, der irgendetwas auslöst. Im Falle von VEGF-Trap wird der Wachstumsfaktor VEGF-A gebunden, den Krebszellen benötigen, um ihre Blutversorgung wachsen zu lassen. Damit basiert Aflibercept auf dem gleichen Wirkprinzip wie der Antikörper Avastin und steht damit in dessen Konkurrenz. Aflibercept ist mit Sanofi verpartnert, die die Entwicklung mit finanzieren. Indikationen sind alle Krebsarten, bei denen Avastin ebenfalls zu Einsatz kommt (Avastin ist das erfolgreichste Krebsmedikament mit mehreren Mrd USD Umsatz). Die Pipeline unten ist nicht ganz vollständig. Aktuelle Studien sind:

PIII-Studien:

- first-line metastatic hormone resistant prostate cancer in combination with taxotere/prednisone

- second-line non-small cell lung cancer in combination with taxotere

- first-line metastatic pancreatic cancer in combination with gemcitabine-based regimen

- second-line metastatic colorectal cancer in combination with FOLFIRI (Folinic Acid, Fluorouracil and irinotecan)

Monotherapie PIIs:

- Advanced ovarian cancer (AOC)

- Non-small cell lung adenocarcinoma (NSCLA)

- Advanced ovarian cancer patients with symptomatic malignant ascites (SMA)

weitere PIIs:

- Metastatic breast cancer

- Metastatic or unresectable kidney cancer

- Recurrent ovarian cancer

- Recurrent malignant gliomas

- Relapsed/refractory multiple myeloma

- Metastatic colorectal cancer

VEGF Trap Eye:

Ebenfalls ein Trap, der VEGF-A und PLGF bindet. Ähnlich wie Genentech's Lucentis soll es bei AMD (altersbedingte Veränderungen der Netzhaut im Auge, die zur Blindheit führen), sowie Varianten davon zum Einsatz kommen. Der Partner ist in diesem Fall Bayer. Gegen wet AMD befindet es sich in PIII, DME (im Zusammenhang mit Diabetes) ist ebenfalls geplant.

Rilonacept:

Ist gegen eine seltene Erkrankung als ARCALYST bereits zugelassen. Wird zurzeit gegen die größere Indikation der Gicht in PII getestet.

REGN88:

Ist der erste Antikörper-Kandidat, der von der umfangreichen Kooperation mit Sanofi in die Klinik gegangen ist. Er richtet sich gegen IL-6 und soll bei Rheumatischer Arthritis angewendet werden. Entwickelt wurde er mit der REGN-Technologie VelocImmune, die spezielle Knockout-Mäuse für die Antikörper-Gewinnung verwendet.

29.11.2007 11:22

Sanofi-Aventis will Regeneron-Beteiligung auf 19% ausweiten

DJ Sanofi-Aventis (News/Aktienkurs) will Regeneron-Beteiligung auf 19% ausweiten

PARIS (Dow Jones)--Der Pharmakonzern Sanofi-Aventis SA will seinen Anteil am US-Konkurrenten Regeneron Pharmaceuticals Inc (News) auf 19% von aktuell 4% erhöhen. Zu diesem Zweck sollen 12 Mio neu emittierte Regeneron-Aktien zum Stückpreis von 26 USD gekauft werden, teilte die in Paris ansässige Sanofi-Aventis am Donnerstag mit. Die Transaktion stehe noch unter dem Vorbehalt der Zustimmung der Kartellbehörden.

Beide Unternehmen haben zudem eine Kooperationsvereinbarung zur gemeinsamen Entwicklung therapeutischer Antikörper unterzeichnet. Sanofi wird Regeneron demnach in den kommenden fünf Jahren insgesamt 85 Mio USD zahlen. Hinzu komme eine Zahlung von bis zu 475 Mio USD, die in den Forschungsetat des US-Konzerns fließen wird.

Im Gegenzug werde der in den USA erzielte Gewinn hälftig unter beiden Pharmakonzernen aufgeteilt. Der in anderen Ländern anfallende Gewinn werde künftig entsprechend vertraglich geregelten Konditionen verteilt.

mfg ipollit

http://www.regeneron.com/

Marktkapitalisierung: 1,73 Mrd USD

Cash: 743 Mio USD

Schulden: 200 Mio USD

Umsatz 2008e/2009e: 222 / 240 Mio USD

Gewinn: (keine Gewinne)

zugelassene Produkte: ARCALYST

Partner: u.a. Sanofi Aventis (ist zu 19% an Regeneron beteiligt), Bayer

Technologien: AK, Trap

Regeneron ist eines der ältesten Biotechs ähnlich wie Amgen oder Genentech, war aber bei weitem nicht so erfolgreich.

Pipeline:

Aflibercept (VEGF-Trap):

Es handelt sich dabei um einen sogenannten Zytokin-Fänger (Trap), wenn ich das richtig übersetzt habe. Damit werden ähnlich wie mit z.B. Antikörpern Signalmoleküle eingefangen und somit davon abgehalten, ihren spezifischen Rezeptor zu aktivieren, der irgendetwas auslöst. Im Falle von VEGF-Trap wird der Wachstumsfaktor VEGF-A gebunden, den Krebszellen benötigen, um ihre Blutversorgung wachsen zu lassen. Damit basiert Aflibercept auf dem gleichen Wirkprinzip wie der Antikörper Avastin und steht damit in dessen Konkurrenz. Aflibercept ist mit Sanofi verpartnert, die die Entwicklung mit finanzieren. Indikationen sind alle Krebsarten, bei denen Avastin ebenfalls zu Einsatz kommt (Avastin ist das erfolgreichste Krebsmedikament mit mehreren Mrd USD Umsatz). Die Pipeline unten ist nicht ganz vollständig. Aktuelle Studien sind:

PIII-Studien:

- first-line metastatic hormone resistant prostate cancer in combination with taxotere/prednisone

- second-line non-small cell lung cancer in combination with taxotere

- first-line metastatic pancreatic cancer in combination with gemcitabine-based regimen

- second-line metastatic colorectal cancer in combination with FOLFIRI (Folinic Acid, Fluorouracil and irinotecan)

Monotherapie PIIs:

- Advanced ovarian cancer (AOC)

- Non-small cell lung adenocarcinoma (NSCLA)

- Advanced ovarian cancer patients with symptomatic malignant ascites (SMA)

weitere PIIs:

- Metastatic breast cancer

- Metastatic or unresectable kidney cancer

- Recurrent ovarian cancer

- Recurrent malignant gliomas

- Relapsed/refractory multiple myeloma

- Metastatic colorectal cancer

VEGF Trap Eye:

Ebenfalls ein Trap, der VEGF-A und PLGF bindet. Ähnlich wie Genentech's Lucentis soll es bei AMD (altersbedingte Veränderungen der Netzhaut im Auge, die zur Blindheit führen), sowie Varianten davon zum Einsatz kommen. Der Partner ist in diesem Fall Bayer. Gegen wet AMD befindet es sich in PIII, DME (im Zusammenhang mit Diabetes) ist ebenfalls geplant.

Rilonacept:

Ist gegen eine seltene Erkrankung als ARCALYST bereits zugelassen. Wird zurzeit gegen die größere Indikation der Gicht in PII getestet.

REGN88:

Ist der erste Antikörper-Kandidat, der von der umfangreichen Kooperation mit Sanofi in die Klinik gegangen ist. Er richtet sich gegen IL-6 und soll bei Rheumatischer Arthritis angewendet werden. Entwickelt wurde er mit der REGN-Technologie VelocImmune, die spezielle Knockout-Mäuse für die Antikörper-Gewinnung verwendet.

29.11.2007 11:22

Sanofi-Aventis will Regeneron-Beteiligung auf 19% ausweiten

DJ Sanofi-Aventis (News/Aktienkurs) will Regeneron-Beteiligung auf 19% ausweiten

PARIS (Dow Jones)--Der Pharmakonzern Sanofi-Aventis SA will seinen Anteil am US-Konkurrenten Regeneron Pharmaceuticals Inc (News) auf 19% von aktuell 4% erhöhen. Zu diesem Zweck sollen 12 Mio neu emittierte Regeneron-Aktien zum Stückpreis von 26 USD gekauft werden, teilte die in Paris ansässige Sanofi-Aventis am Donnerstag mit. Die Transaktion stehe noch unter dem Vorbehalt der Zustimmung der Kartellbehörden.

Beide Unternehmen haben zudem eine Kooperationsvereinbarung zur gemeinsamen Entwicklung therapeutischer Antikörper unterzeichnet. Sanofi wird Regeneron demnach in den kommenden fünf Jahren insgesamt 85 Mio USD zahlen. Hinzu komme eine Zahlung von bis zu 475 Mio USD, die in den Forschungsetat des US-Konzerns fließen wird.

Im Gegenzug werde der in den USA erzielte Gewinn hälftig unter beiden Pharmakonzernen aufgeteilt. Der in anderen Ländern anfallende Gewinn werde künftig entsprechend vertraglich geregelten Konditionen verteilt.

mfg ipollit

Änderungen im Depot...

- weitere Reduzierung der Regeneron-Position; REGN ist mir doch zu riskant, um so deutlich übergewichtet zu sein. Ziel sind etwa 10% Depotanteil.

- weitere Reduzierung der Imclone-Position; IMCL steht mit ca. 65 USD deutlich über den gebotenen 60 USD. Ich kann nicht abschätzen, wieviel ein verbessertes Angebot erzielen kann... vielleicht nochmal nochmal 10% über dem aktuellen Kurs? Aber garantiert ist es nicht und der Zeitpunkt ist ebenfalls unklar.

- Aufstockung der Evotec-Position

- Aufbau von Positionen in Rigel (aussichtsreiches orales RA-Mittel in PII) und Incyte (JAK-Hemmer in PII): beide Unternehmen bereits hoch bewertet, zwar mit Chancen aber auch mit dem Risiko eines deutlichen Rückschlags. Daher nur spekulative kleine Positionen.

23,5% Genmab http://finance.yahoo.com/q?s=GEN.CO

13,5% Regeneron http://finance.yahoo.com/q?s=REGN

9,1% Onyx http://finance.yahoo.com/q?s=ONXX

7,0% Evotec http://finance.yahoo.com/q?s=EVT.DE

6,8% OSI Pharma http://finance.yahoo.com/q?s=OSIP

5,9% (KO) Intercell http://finance.yahoo.com/q?s=IJE.F

5,4% Cubist http://finance.yahoo.com/q?s=CBST

5,0% Isis http://finance.yahoo.com/q?s=ISIS

4,8% Vertex http://finance.yahoo.com/q?s=VRTX

3,4% Arena http://finance.yahoo.com/q?s=ARNA

3,1% ViroPharma http://finance.yahoo.com/q?s=VPHM

3,0% Micromet http://finance.yahoo.com/q?s=MITI

2,6% Rigel http://finance.yahoo.com/q?s=RIGL

2,6% Imclone http://finance.yahoo.com/q?s=IMCL

2,5% Incyte http://finance.yahoo.com/q?s=INCY

1,8% Supergen http://finance.yahoo.com/q?s=SUPG

Watchliste: POZN (Spekulation auf keinen völligen Fehlschlag bei der Vermarktung von Treximent, sowie dem Erfolg von PN 400), SGEN (hoch bewertet, scheint aber ein wesentlicher Teil der Genentech-Pipeline zu bilden und die AK-Technologie könnte Potential haben) und MNTA (Generika-Technologie)

mfg ipollit

- weitere Reduzierung der Regeneron-Position; REGN ist mir doch zu riskant, um so deutlich übergewichtet zu sein. Ziel sind etwa 10% Depotanteil.

- weitere Reduzierung der Imclone-Position; IMCL steht mit ca. 65 USD deutlich über den gebotenen 60 USD. Ich kann nicht abschätzen, wieviel ein verbessertes Angebot erzielen kann... vielleicht nochmal nochmal 10% über dem aktuellen Kurs? Aber garantiert ist es nicht und der Zeitpunkt ist ebenfalls unklar.

- Aufstockung der Evotec-Position

- Aufbau von Positionen in Rigel (aussichtsreiches orales RA-Mittel in PII) und Incyte (JAK-Hemmer in PII): beide Unternehmen bereits hoch bewertet, zwar mit Chancen aber auch mit dem Risiko eines deutlichen Rückschlags. Daher nur spekulative kleine Positionen.

23,5% Genmab http://finance.yahoo.com/q?s=GEN.CO

13,5% Regeneron http://finance.yahoo.com/q?s=REGN

9,1% Onyx http://finance.yahoo.com/q?s=ONXX

7,0% Evotec http://finance.yahoo.com/q?s=EVT.DE

6,8% OSI Pharma http://finance.yahoo.com/q?s=OSIP

5,9% (KO) Intercell http://finance.yahoo.com/q?s=IJE.F

5,4% Cubist http://finance.yahoo.com/q?s=CBST

5,0% Isis http://finance.yahoo.com/q?s=ISIS

4,8% Vertex http://finance.yahoo.com/q?s=VRTX

3,4% Arena http://finance.yahoo.com/q?s=ARNA

3,1% ViroPharma http://finance.yahoo.com/q?s=VPHM

3,0% Micromet http://finance.yahoo.com/q?s=MITI

2,6% Rigel http://finance.yahoo.com/q?s=RIGL

2,6% Imclone http://finance.yahoo.com/q?s=IMCL

2,5% Incyte http://finance.yahoo.com/q?s=INCY

1,8% Supergen http://finance.yahoo.com/q?s=SUPG

Watchliste: POZN (Spekulation auf keinen völligen Fehlschlag bei der Vermarktung von Treximent, sowie dem Erfolg von PN 400), SGEN (hoch bewertet, scheint aber ein wesentlicher Teil der Genentech-Pipeline zu bilden und die AK-Technologie könnte Potential haben) und MNTA (Generika-Technologie)

mfg ipollit

zu Genmab...

die aktuell starke Übergewichtung halte ich für gerechtfertigt, da sich in der Pipeline u.a. mit HuMax-CD20 eine vielversprechende Alternative zum etablierten Blockbuster Rituxan und mit HuMax-Egfr eine Alternative zum Blockbuster Erbitux in der fortgeschrittenen PIII befindet. Rituxan ist eine wesentliche Basis von BiogenIdec (MK 14 Mrd USD) und Erbitux ist Imclone (MK 5,5 Mrd USD). Zudem besteht Übernahme-Phantasie durch GSK.

Im Analystenkommentar unten:

- in der PIII von HuMax-CD20 deutlich bessere Daten (51% und 44% RR) beim refraktionärem CLL als von Rituxan (25% RR) und Campath (33% RR)

- mit fasttrack Zulassung bereits Anfang 2009 möglich; dies würde einen 200 Mio USD Meilenstein an Genmab auslösen

- off-label Einsatz geplant

- GSK soll Produktionskapazitäten reserviert haben, um HuMax-CD20 im Wert von 1,2 bis 2 Mrd USD produzieren zu können

- HuMax-Egfr PIII-Daten bald verfügbar, die für eine Zulassung ausreichen könnten (HuMax-EGFR ist noch nicht verpartnert! Volle Rechte bei Genmab)

********

Bullets Genmab: Spectacular Phase III data HuMax CD20 CLL, BUY maintained by SNS Securities

Yesterday, Genmab announced spectacular Phase III data of HuMax CD20 (ofatumumab) CLL in refractory patients. The overall response rate of the two patients group treated was 51% in patients refractory to fludarabine (chemotherapy) and Campath (competitive antibody against CLL), and 44% in patients to fludarabine alone. Market consensus was around 25% overall response rate.

Also compared to Phase III data of competitive antibodies like Rituxan (25% response rate in refractory CLL patients) and Campath (33% response rate), the data of Genmab are superior. In our view there should be no doubt that this product will be approved by the FDA. We expect Genmab/GSK to go for BLA filing very soon. The filing and the subsequent approval will trigger a milestone that we estimate to be USD 200m. Genmab has a fast track on HuMax CD20 CLL, so the FDA is likely to give approval between 2 and 6 months.

The strong Phase III data on refractory patients also makes a strong case for the off label use of the drug for other groups of patients (first line) and even for other indications like Non Hodgkin’s Lymphoma. It has always been Genmab’s strategy to go for off label use after getting the Phase III data on HuMax CD20 CLL in refractory patients. In the next few weeks, Genmab/GSK will likely start a large Phase III study with HuMax CD20 in first line patients. The first data on this study should coincide with the market launch of the drug in refractory patients. Positive data would support the launch of the product, which we expect to happen end 2009Q1.

The case of a strong and swift market introduction is backed by GSK, who seems to have made reservations on 40,000 liter capacity at Lonza for the production of HuMax CD20. Considering a yield of 3-5 grams per liter, this would mean USD 1.2-2bn.

Later this year, an interim analysis of HuMax EGFr refractory H&N Phase III is to be expected. In April 132 patients were included in the pivotal trial. The last few weeks patient inclusion is about 5-10 persons per week. Counted from April this would mean that now 192-252 patients are enrolled. Two third of patients are receiving the drug. An interim analysis is possible with the data of 116 patients. The longer it takes that we need to wait for the interim analysis, the better the data are expected to be (with higher survival rates, current treatment in refractory has survival rate of about 3-4 months). The recent bid on ImClone by BMS (USD 4.5bn, specifically on its drug Erbitux), also gives an indication what the potential value is for this program.

We believe that the strong data on HuMax CD20 CLL will pave the way for a move from GSK in taking over the company. The time frame seems to be between August and November (between CLL data and interim analysis EGFr). With positive data on CLL, GSK has the hard data in hand to validate a take over. Wating till the announcement of the interim analysis on HuMax EGFr H&N would only increase the price. Pressure to come with interim analysis on EGFr sooner rather than later will increase in the next few months. Good data on 116 patients should be enough to file for approval. For GSK the risks have decreased considerably with the hard data on HuMax CD20. Also bear in mind that for GSK the financial ratio to go for a take over scenario becomes more interesting, since the company still needs to pay milestones up to USD 1bn and royalties up to 50%.

A take over scenario is becoming also more likely considering the ongoing M&A activity in the sector. The biotech companies that have been taken over announced positive Phase III data and /or already have products on the market. Genmab now can also be put in this select group of candidates.

In all, we strongly maintain our Buy rating on the stock. We advice our clients to maintain current holdings or even increase stakes in the company. At the current share price we still see considerable upside potential of 60-100%.

Regards,

Marcel Wijma

Senior Equity Analyst Biotechnology

SNS Securities N.V.

mfg ipollit

die aktuell starke Übergewichtung halte ich für gerechtfertigt, da sich in der Pipeline u.a. mit HuMax-CD20 eine vielversprechende Alternative zum etablierten Blockbuster Rituxan und mit HuMax-Egfr eine Alternative zum Blockbuster Erbitux in der fortgeschrittenen PIII befindet. Rituxan ist eine wesentliche Basis von BiogenIdec (MK 14 Mrd USD) und Erbitux ist Imclone (MK 5,5 Mrd USD). Zudem besteht Übernahme-Phantasie durch GSK.

Im Analystenkommentar unten:

- in der PIII von HuMax-CD20 deutlich bessere Daten (51% und 44% RR) beim refraktionärem CLL als von Rituxan (25% RR) und Campath (33% RR)

- mit fasttrack Zulassung bereits Anfang 2009 möglich; dies würde einen 200 Mio USD Meilenstein an Genmab auslösen

- off-label Einsatz geplant

- GSK soll Produktionskapazitäten reserviert haben, um HuMax-CD20 im Wert von 1,2 bis 2 Mrd USD produzieren zu können

- HuMax-Egfr PIII-Daten bald verfügbar, die für eine Zulassung ausreichen könnten (HuMax-EGFR ist noch nicht verpartnert! Volle Rechte bei Genmab)

********

Bullets Genmab: Spectacular Phase III data HuMax CD20 CLL, BUY maintained by SNS Securities

Yesterday, Genmab announced spectacular Phase III data of HuMax CD20 (ofatumumab) CLL in refractory patients. The overall response rate of the two patients group treated was 51% in patients refractory to fludarabine (chemotherapy) and Campath (competitive antibody against CLL), and 44% in patients to fludarabine alone. Market consensus was around 25% overall response rate.