5BG Der goldene Stern!!? - 500 Beiträge pro Seite

eröffnet am 03.12.09 20:23:54 von

neuester Beitrag 11.08.17 09:12:41 von

neuester Beitrag 11.08.17 09:12:41 von

Beiträge: 308

ID: 1.154.624

ID: 1.154.624

Aufrufe heute: 0

Gesamt: 41.786

Gesamt: 41.786

Aktive User: 0

ISIN: CA11777Q2099 · WKN: A0M889 · Symbol: 5BG

2,6090

EUR

+0,85 %

+0,0220 EUR

Letzter Kurs 18:11:02 Tradegate

Neuigkeiten

10.05.24 · inv3st.de Anzeige |

09.05.24 · Jörg Schulte Anzeige |

08.05.24 · globenewswire |

17.04.24 · wO Chartvergleich |

Werte aus der Branche Rohstoffe

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,0000 | +809,09 | |

| 1,7000 | +14,09 | |

| 1,0350 | +9,02 | |

| 3,8360 | +8,79 | |

| 0,5500 | +7,84 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 0,7300 | -8,75 | |

| 14.900,00 | -9,70 | |

| 0,6800 | -11,69 | |

| 0,7700 | -25,96 | |

| 47,85 | -97,97 |

Hallo, an alle die diese Aktie gekauft haben, beobachten, überlegen zu kaufen.

Ich würde gerne mehr zu dieser Aktie erfahren und Eure Meinung hören.

Auch im Minenportal ist die Darstellung sehr dürftig.

Gruss Raupe

Ich würde gerne mehr zu dieser Aktie erfahren und Eure Meinung hören.

Auch im Minenportal ist die Darstellung sehr dürftig.

Gruss Raupe

Kauf dir den aktuellen Aktionär.

.....gibts noch mehr Details als im Aktionär...? Da liest es sich ja ganz interessant...

Antwort auf Beitrag Nr.: 38.505.922 von ThorVestor am 03.12.09 21:40:21

Danke,für die schnelle Antwort!

Danke,für die schnelle Antwort!

B2Gold gab am Dienstag bekannt, dass die Produktion von Gold und Silber aus der Tagebaumine Orosi begonnen hat und gestern der erste Dore-Barren gegossen wurde. Die Erzverarbeitung hatte am 15.12.2009 begonnen.

Schätzungen zufolge sollen in der Mine in den ersten sieben Betriebsjahren zwischen 80.000 und 90.000 oz pro Jahr produziert werden. B2Gold geht von Cashkosten von 465 USD/oz aus.

Im ersten Quartal des Jahres 2007 setzte der Vorbesitzer, Central Sun Mining, die Arbeiten in der Orosi Mine aus. Man stellte fest, dass die Goldausbeute der Mine von etwa 40% mit Haufenlaugung durch konventionellen Mühlenbetrieb auf etwa 90% gesteigert werden könnte.

Die neue Anlage ist jetzt komplett und soll während der nächsten Monate auf einen Durchsatz von bis zu 3.500 t/Tag anlaufen. Die Verarbeitungsmenge soll dann auf 5.500 t/d gesteigert werden.

© Redaktion MinenPortal.de

Schätzungen zufolge sollen in der Mine in den ersten sieben Betriebsjahren zwischen 80.000 und 90.000 oz pro Jahr produziert werden. B2Gold geht von Cashkosten von 465 USD/oz aus.

Im ersten Quartal des Jahres 2007 setzte der Vorbesitzer, Central Sun Mining, die Arbeiten in der Orosi Mine aus. Man stellte fest, dass die Goldausbeute der Mine von etwa 40% mit Haufenlaugung durch konventionellen Mühlenbetrieb auf etwa 90% gesteigert werden könnte.

Die neue Anlage ist jetzt komplett und soll während der nächsten Monate auf einen Durchsatz von bis zu 3.500 t/Tag anlaufen. Die Verarbeitungsmenge soll dann auf 5.500 t/d gesteigert werden.

© Redaktion MinenPortal.de

Trading Spotlight

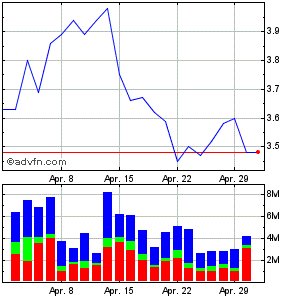

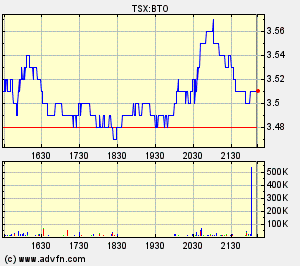

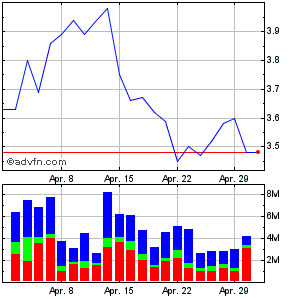

B2GOLD CORP - BTO:TSX 3.20 +0.22 +7.38%

Smile

Smile

B2Gold ist eine der wenigen Goldaktien, die aktuell kurz vor einem neuen ATH stehen:

Eindrucksvoll der Anteil institutioneller Investoren:

Institutional Holders BTO

% Shares Owned: 68.36%

# of Holders: 45

Total Shares Held: 233,340,429

3 Mo. Net Change: 3,254,397

# New Positions: 4

# Closed Positions: 2

# Increased Positions: 19

# Reduced Positions: 8

# Net Buyers: 11

http://www.reuters.com/finance/stocks/financialHighlights?rp…

Institutional Holders BTO

% Shares Owned: 68.36%

# of Holders: 45

Total Shares Held: 233,340,429

3 Mo. Net Change: 3,254,397

# New Positions: 4

# Closed Positions: 2

# Increased Positions: 19

# Reduced Positions: 8

# Net Buyers: 11

http://www.reuters.com/finance/stocks/financialHighlights?rp…

Antwort auf Beitrag Nr.: 41.614.214 von Videomart am 07.06.11 15:50:00und jetzt kurz über ATH an der TSX

Antwort auf Beitrag Nr.: 41.616.094 von schnick-schnack am 07.06.11 20:11:05...und das hat seinen Grund:

B2Gold Corp. Announces Positive Initial Exploration Drill Results from the Cebollati Project in Uruguay

VANCOUVER, BRITISH COLUMBIA -- (Marketwire) -- 06/07/11 --

http://www.finanznachrichten.de/nachrichten-2011-06/20458546…

B2Gold Corp. Announces Positive Initial Exploration Drill Results from the Cebollati Project in Uruguay

VANCOUVER, BRITISH COLUMBIA -- (Marketwire) -- 06/07/11 --

http://www.finanznachrichten.de/nachrichten-2011-06/20458546…

B2GOLD CORP - BTO:TSX 3,61 0,30 +9,06%

Smile

Smile

Da wär noch...

Notice of B2Gold's 2011 First Quarter Results Conference Call/Webcast Notice of 2010 Annual General and Special Meeting, Conference Call/Webcast

Press Release Source: B2Gold Corp. On Friday June 3, 2011, 9:00 am EDT

VANCOUVER, BRITISH COLUMBIA--(Marketwire - 06/03/11) - B2Gold Corp. (TSX:BTO - News)(OTCQX: BGLPF) ("B2Gold" or the "Company") will release its 2011 first quarter results before the North American markets open on Friday June 10, 2011...

http://finance.yahoo.com/news/Notice-of-B2Golds-2011-First-i…

Notice of B2Gold's 2011 First Quarter Results Conference Call/Webcast Notice of 2010 Annual General and Special Meeting, Conference Call/Webcast

Press Release Source: B2Gold Corp. On Friday June 3, 2011, 9:00 am EDT

VANCOUVER, BRITISH COLUMBIA--(Marketwire - 06/03/11) - B2Gold Corp. (TSX:BTO - News)(OTCQX: BGLPF) ("B2Gold" or the "Company") will release its 2011 first quarter results before the North American markets open on Friday June 10, 2011...

http://finance.yahoo.com/news/Notice-of-B2Golds-2011-First-i…

TSX to announce index changes

Changes to the S&P/TSX composite index are expected to be announced June 10, after a quarterly review.

UBS Securities Canada strategist Garry Cooper says 13 stocks have a strong possibility of being added, and one, Ritchie Bros. Auctioneers Inc. (RBA-T25.12-0.23-0.91%), deleted.

The candidates for addition:

•Athabasca Oil Sands Corp. (ATH-T16.54-0.26-1.55%)

•Meg Energy Corp. (MEG-T50.29-1.13-2.20%)

•Tourmaline Oil Corp. (TOU-T29.99-0.10-0.33%)

•Tahoe Resources Inc. (THO-T20.500.020.10%)

•Capital Power Corp. (CPX-T26.190.200.77%)

•Romarco Minerals Inc. (R-T1.99-0.02-1.00%)

•Extorre Gold Mines Ltd. (XG-T11.400.312.80%)

•Wi-Lan Inc. (WIN-T7.00----%)

•San Gold Corp. (SGR-T3.10-0.02-0.64%)

•Bonterra Energy Corp. (BNE-T62.20-0.30-0.48%)

•B2Gold Corp. (BTO-T3.550 .195.65%)

•Paramount Resources Ltd. (POU-T28.70-0.53-1.81%)

•Endeavour Silver Corp. (EDR-T7.95-0.27-3.28%)

http://www.theglobeandmail.com/report-on-business/top-busine…

B2Gold meldet Rekord-Quartalszahlen

Freitag, 10. Juni 2011 | 16:00

Die kanadische B2Gold hat am Freitag die Zahlen für das erste Viertel dieses Jahres vorgelegt. Diese zeigen eine deutlich steigende Tendenz.

Es sind Rekordziffern, die B2Gold (WKN: A0M889) am Freitag für das erste Quartal vorgelegt hat. Der kanadische Goldkonzern meldet eine Förderung von 38.754 Unzen Gold, weit mehr als doppelt so viel wie im Vorjahreszeitraum. Der Umsatz wurde neben der steigenden Produktion auch durch höhere Verkaufspreise positiv beeinflusst. Für die höhere Unzenzahl ist die Produktion auf dem Goldprojekt La Libertad in Nicaragua verantwortlich. 53,5 Millionen Dollar hat man insgesamt umgesetzt nach lediglich 17,1 Millionen Dollar im Vorjahresquartal.

Auf bereinigter Basis ist auch das Ergebnis des Konzerns klar gestiegen. Hatte man im ersten Quartal 2010 noch einen Verlust von 3,3 Millionen Dollar zu verbuchen, so hat man nun einen Gewinn von 18,1 Millionen Dollar bzw. 5 Cent je B2Gold-Aktie erwirtschaftet. Der Cashflow ist zugleich von 0,6 Millionen Dollar auf 26,1 Millionen Dollar vergrößert worden.

Einen konkreten Ausblick auf die Zahlen des Gesamtjahres legt B2Gold am Freitag nicht vor.

http://cnrp.marketwire.com/cnrp_files/20110610-0610bto.pdf

Freitag, 10. Juni 2011 | 16:00

Die kanadische B2Gold hat am Freitag die Zahlen für das erste Viertel dieses Jahres vorgelegt. Diese zeigen eine deutlich steigende Tendenz.

Es sind Rekordziffern, die B2Gold (WKN: A0M889) am Freitag für das erste Quartal vorgelegt hat. Der kanadische Goldkonzern meldet eine Förderung von 38.754 Unzen Gold, weit mehr als doppelt so viel wie im Vorjahreszeitraum. Der Umsatz wurde neben der steigenden Produktion auch durch höhere Verkaufspreise positiv beeinflusst. Für die höhere Unzenzahl ist die Produktion auf dem Goldprojekt La Libertad in Nicaragua verantwortlich. 53,5 Millionen Dollar hat man insgesamt umgesetzt nach lediglich 17,1 Millionen Dollar im Vorjahresquartal.

Auf bereinigter Basis ist auch das Ergebnis des Konzerns klar gestiegen. Hatte man im ersten Quartal 2010 noch einen Verlust von 3,3 Millionen Dollar zu verbuchen, so hat man nun einen Gewinn von 18,1 Millionen Dollar bzw. 5 Cent je B2Gold-Aktie erwirtschaftet. Der Cashflow ist zugleich von 0,6 Millionen Dollar auf 26,1 Millionen Dollar vergrößert worden.

Einen konkreten Ausblick auf die Zahlen des Gesamtjahres legt B2Gold am Freitag nicht vor.

http://cnrp.marketwire.com/cnrp_files/20110610-0610bto.pdf

B2GOLD CORP - BTO:TSX 3,68 CAD 0,32 +9,52% (ATH 3,72)

TD Securities stuft B2Gold auf buy

Rating-Update:

Toronto (aktiencheck.de AG) - Steven Green, Analyst von TD Securities, stuft die Aktie von B2Gold (ISIN CA11777Q2099/ WKN A0M889) unverändert mit "buy" ein. Das Kursziel werde von 3,75 auf 4,25 USD angehoben. (Analyse vom 13.06.11) (14.06.2011/ac/a/u)

http://www.wallstreet-online.de/nachricht/3177763-td-securit…" target="_blank" rel="nofollow ugc noopener">

http://www.wallstreet-online.de/nachricht/3177763-td-securit…

Rating-Update:

Toronto (aktiencheck.de AG) - Steven Green, Analyst von TD Securities, stuft die Aktie von B2Gold (ISIN CA11777Q2099/ WKN A0M889) unverändert mit "buy" ein. Das Kursziel werde von 3,75 auf 4,25 USD angehoben. (Analyse vom 13.06.11) (14.06.2011/ac/a/u)

http://www.wallstreet-online.de/nachricht/3177763-td-securit…" target="_blank" rel="nofollow ugc noopener">

http://www.wallstreet-online.de/nachricht/3177763-td-securit…

Institutional Holders

% Shares Owned: 75.77%

# of Holders: 50

Total Shares Held: 259,026,290

3 Mo. Net Change: -6,630,419

# New Positions: 4

# Closed Positions: 3

# Increased Positions: 19

# Reduced Positions: 12

# Net Buyers: 7

http://www.reuters.com/finance/stocks/financialHighlights?sy…

% Shares Owned: 75.77%

# of Holders: 50

Total Shares Held: 259,026,290

3 Mo. Net Change: -6,630,419

# New Positions: 4

# Closed Positions: 3

# Increased Positions: 19

# Reduced Positions: 12

# Net Buyers: 7

http://www.reuters.com/finance/stocks/financialHighlights?sy…

geiler chart .....

Das ist seit fast zwei Jahren die beste Goldaktie, die ich beobachte, und "kein Schwein" interessiert sich dafür!

Auch heute wieder ein beeindruckendes Volumen...

Anfang 2010 war BTO zusammen mit Detour Gold einer der "Top-Picks" des Jahres bei Haywood Securities.

Die Jungs scheinen ein verdammt gutes Näschen für aussichtsreiche Werte zu haben...

Auch heute wieder ein beeindruckendes Volumen...

Anfang 2010 war BTO zusammen mit Detour Gold einer der "Top-Picks" des Jahres bei Haywood Securities.

Die Jungs scheinen ein verdammt gutes Näschen für aussichtsreiche Werte zu haben...

schau dir mal CNR Condor Res. an

die sind noch am Anfang + haben z.T. gemeinsame Projekte bzw. Liegenschaften direkt neben B2G

ich habe B2G auch erst darüber kennen gelernt ...

die sind noch am Anfang + haben z.T. gemeinsame Projekte bzw. Liegenschaften direkt neben B2G

ich habe B2G auch erst darüber kennen gelernt ...

B2Gold founders sell C$22.6m stake in company

B2Gold said founding members sold 13 percent worth of their shares in the gold producer to diversify their portfolios, but that they do not intend to sell more shares.

Author: Kip Keen

Posted: Thursday , 07 Jul 2011

http://www.mineweb.com/mineweb/view/mineweb/en/page34?oid=13…

B2Gold said founding members sold 13 percent worth of their shares in the gold producer to diversify their portfolios, but that they do not intend to sell more shares.

Author: Kip Keen

Posted: Thursday , 07 Jul 2011

http://www.mineweb.com/mineweb/view/mineweb/en/page34?oid=13…

B2Gold Reports Heavy Rains and Flooding at the Limon Mine in Nicaragua,

Resulting in a Temporary Shutdown of the Underground Workings

Vancouver, June 21, 2011

http://cnrp.marketwire.com/cnrp_files/20110621-bto621.pdf

B2Gold Reports Fatality at the Limon Mine in Nicaragua

Vancouver, June 24, 2011

http://cnrp.marketwire.com/cnrp_files/20110623-bto624b.pdf

Resulting in a Temporary Shutdown of the Underground Workings

Vancouver, June 21, 2011

http://cnrp.marketwire.com/cnrp_files/20110621-bto621.pdf

B2Gold Reports Fatality at the Limon Mine in Nicaragua

Vancouver, June 24, 2011

http://cnrp.marketwire.com/cnrp_files/20110623-bto624b.pdf

Läuft doch

B2Gold Corp. Reports Second Quarter 2011 Gold Production and Provides Limon Mine Update

VANCOUVER, BRITISH COLUMBIA -- (Marketwire) -- 07/28/11 -- B2Gold Corp. (TSX: BTO)(OTCQX: BGLPF) ("B2Gold" or the "Company"), is pleased to announce its gold production and record revenue for the second quarter of 2011 as well as provide an update on the status at the Limon Mine. All dollar figures are in United States dollars unless otherwise indicated.

2011 Second Quarter Highlights

-- Record gold revenue of $54.5 million

-- Gold production of 36,760 ounces exceeding budget

-- Gold sales of 36,030 ounces

Second Quarter 2011 Gold Production

B2Gold's consolidated gold production for the second quarter of 2011 from La Libertad and Limon Mines in Nicaragua was 36,760 ounces of gold, exceeding the Company's second quarter budget of 33,835 ounces.

Gold production at La Libertad Mine was 24,568 ounces compared to budget of 21,927 ounces, mainly due to higher recoveries, higher mill throughput and the processing of higher grade ore. Gold recoveries in the quarter were 90% exceeding the budget of 87%. Mill throughput averaged 5,475 tonnes of ore per day versus the budget of 5,363 tonnes of ore per day at an average feed grade of 1.71 grams of gold per tonne versus budget of 1.61 grams of gold per tonne.

The Limon Mine also performed better than budget producing 12,192 ounces of gold compared to budget of 11,908 ounces. The higher than budget gold production was due to a combination of factors as mill head grade and recovery were slightly better than budget.

Total gold revenue for the second quarter was a record $54.5 million on sales of 36,030 ounces, compared to $53.5 million on sales of 38,754 ounces in the 2011 first quarter. This increase in revenue was attributable to a higher average realized gold price in the second quarter of $1,513 per ounce, which exceeded the first quarter average realized gold price of $1,381. This also compares favorably to the average spot gold price of $1,504 per ounce for the quarter.

The Company remains in a strong financial position with over $78 million in cash at the end of the quarter. B2Gold has no debt and remains unhedged.

B2Gold is projecting another record year for consolidated gold production in 2011 and is increasing full year production guidance to be between 135,000 to 145,000 ounces of gold, an increase of 5,000 from previous guidance. The increase in guidance is mainly due to higher gold recoveries (expected to average 90%) and ore grades at La Libertad Mine experienced through the first half of 2011 and which is expected to continue into the second half of the year. La Libertad production guidance has been increased to 93,000 to 99,000 ounces of gold in 2011. Consolidated operating cash costs for 2011 are projected to remain on budget of between $540 to $560 per ounce of gold.

Limon Mine Update

As the Company reported on June 24, 2011, the Limon Mine suffered a force majeur event that resulted in a fatality. The event was the consequence of an extreme rainfall and surface water runoff that exceeded design capacity. One of the open pits (Pit 2) was flooded when surface water management structures were overwhelmed and subsequently the water found its way through old workings into a portion of the active underground mine.

Since the accident mine management has worked with the Representative unions and the Company's Health and Safety Committee to develop a rehabilitation program that will ensure that a similar event cannot occur in the future and allow safe return to production of first, Pit 2, and then, Santa Pancha underground mine. Management is currently implementing the work recommended in the plan, which is fully supported by all groups at the mine, both labour and management. The Company remains committed to ensuring the highest standards for occupational health and safety.

Currently mine management is reviewing the rehabilitation plan with the Nicaraguan Ministry of Labour. The intent is to have Pit 2 return to production in August and Santa Pancha in September.

In the meantime ore processing has continued, first from stockpiles then from operations at Babilonia Pit and Pit 4 surface operations. These pits are the result of the successful ongoing development work with B2Gold Exploration and El Limon Engineering. In the near term gold grades will be slightly lower than budget but management anticipates that 2011 budgeted production, estimated at between 42,000 and 46,000 ounces of gold will be met.

Exploration Update

The Company's extensive 2011 exploration programs on numerous projects are well underway. Drilling continues on La Libertad and Limon properties in Nicaragua, the Gramalote property in Colombia and the Cebollati property in Uruguay. In total, B2Gold's combined 2011 exploration and pre-feasibility budgets total approximately $39 million and will fund approximately 84,000 metres of diamond drilling. The Company expects to release drilling results from its exploration projects over the next several weeks.

2011 Second Quarter Results Conference Call and Webcast

B2Gold will be releasing its second quarter 2011 financial results on Thursday August 11, 2011. A conference call and webcast will be held on Friday August 12, 2011 at 10:00 am Pacific Time.

You may access the call by dialing the operator at 416-695-7848 or toll free 1-800-766-6630 prior to the scheduled start time or you may listen to the call via webcast by following the link on the Company's website at www.b2gold.com.

A playback version of the call will be available for one week after the call by dialing 905-694-9451 or toll free 1-800-408-3053 (pass code: 1251652).

ON BEHALF OF B2GOLD CORP.

Clive T. Johnson, President and Chief Executive Officer

For more information on B2Gold please visit the Company web site at www.b2gold.com.

The securities described herein have not been and will not be registered under the United States Securities Act of 1933, as amended, and may not be offered or sold in the United States absent registration or an applicable exemption from registration requirements.

Some of the statements contained in this release are forward-looking statements, such as estimates and statements that describe the Company's future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. Since forward-looking statements address future events and conditions, by their very nature, they involve inherent risks and uncertainties. Actual results in each case could differ materially from those currently anticipated in such statements.

The Toronto Stock Exchange neither approves nor disapproves the information contained in this News Release.

Contacts:

B2Gold Corp.

Ian MacLean

Vice President, Investor Relations

604-681-8371

B2Gold Corp.

Kerry Suffolk

Manager, Investor Relations

604-681-8371

www.b2gold.com

© 2011 MarketWir

VANCOUVER, BRITISH COLUMBIA -- (Marketwire) -- 07/28/11 -- B2Gold Corp. (TSX: BTO)(OTCQX: BGLPF) ("B2Gold" or the "Company"), is pleased to announce its gold production and record revenue for the second quarter of 2011 as well as provide an update on the status at the Limon Mine. All dollar figures are in United States dollars unless otherwise indicated.

2011 Second Quarter Highlights

-- Record gold revenue of $54.5 million

-- Gold production of 36,760 ounces exceeding budget

-- Gold sales of 36,030 ounces

Second Quarter 2011 Gold Production

B2Gold's consolidated gold production for the second quarter of 2011 from La Libertad and Limon Mines in Nicaragua was 36,760 ounces of gold, exceeding the Company's second quarter budget of 33,835 ounces.

Gold production at La Libertad Mine was 24,568 ounces compared to budget of 21,927 ounces, mainly due to higher recoveries, higher mill throughput and the processing of higher grade ore. Gold recoveries in the quarter were 90% exceeding the budget of 87%. Mill throughput averaged 5,475 tonnes of ore per day versus the budget of 5,363 tonnes of ore per day at an average feed grade of 1.71 grams of gold per tonne versus budget of 1.61 grams of gold per tonne.

The Limon Mine also performed better than budget producing 12,192 ounces of gold compared to budget of 11,908 ounces. The higher than budget gold production was due to a combination of factors as mill head grade and recovery were slightly better than budget.

Total gold revenue for the second quarter was a record $54.5 million on sales of 36,030 ounces, compared to $53.5 million on sales of 38,754 ounces in the 2011 first quarter. This increase in revenue was attributable to a higher average realized gold price in the second quarter of $1,513 per ounce, which exceeded the first quarter average realized gold price of $1,381. This also compares favorably to the average spot gold price of $1,504 per ounce for the quarter.

The Company remains in a strong financial position with over $78 million in cash at the end of the quarter. B2Gold has no debt and remains unhedged.

B2Gold is projecting another record year for consolidated gold production in 2011 and is increasing full year production guidance to be between 135,000 to 145,000 ounces of gold, an increase of 5,000 from previous guidance. The increase in guidance is mainly due to higher gold recoveries (expected to average 90%) and ore grades at La Libertad Mine experienced through the first half of 2011 and which is expected to continue into the second half of the year. La Libertad production guidance has been increased to 93,000 to 99,000 ounces of gold in 2011. Consolidated operating cash costs for 2011 are projected to remain on budget of between $540 to $560 per ounce of gold.

Limon Mine Update

As the Company reported on June 24, 2011, the Limon Mine suffered a force majeur event that resulted in a fatality. The event was the consequence of an extreme rainfall and surface water runoff that exceeded design capacity. One of the open pits (Pit 2) was flooded when surface water management structures were overwhelmed and subsequently the water found its way through old workings into a portion of the active underground mine.

Since the accident mine management has worked with the Representative unions and the Company's Health and Safety Committee to develop a rehabilitation program that will ensure that a similar event cannot occur in the future and allow safe return to production of first, Pit 2, and then, Santa Pancha underground mine. Management is currently implementing the work recommended in the plan, which is fully supported by all groups at the mine, both labour and management. The Company remains committed to ensuring the highest standards for occupational health and safety.

Currently mine management is reviewing the rehabilitation plan with the Nicaraguan Ministry of Labour. The intent is to have Pit 2 return to production in August and Santa Pancha in September.

In the meantime ore processing has continued, first from stockpiles then from operations at Babilonia Pit and Pit 4 surface operations. These pits are the result of the successful ongoing development work with B2Gold Exploration and El Limon Engineering. In the near term gold grades will be slightly lower than budget but management anticipates that 2011 budgeted production, estimated at between 42,000 and 46,000 ounces of gold will be met.

Exploration Update

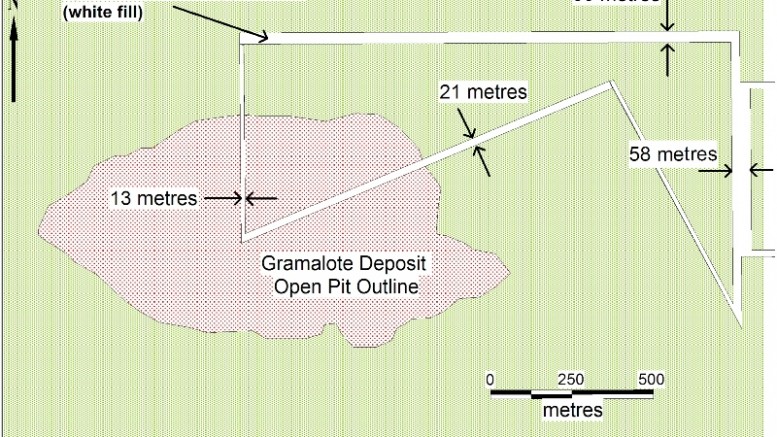

The Company's extensive 2011 exploration programs on numerous projects are well underway. Drilling continues on La Libertad and Limon properties in Nicaragua, the Gramalote property in Colombia and the Cebollati property in Uruguay. In total, B2Gold's combined 2011 exploration and pre-feasibility budgets total approximately $39 million and will fund approximately 84,000 metres of diamond drilling. The Company expects to release drilling results from its exploration projects over the next several weeks.

2011 Second Quarter Results Conference Call and Webcast

B2Gold will be releasing its second quarter 2011 financial results on Thursday August 11, 2011. A conference call and webcast will be held on Friday August 12, 2011 at 10:00 am Pacific Time.

You may access the call by dialing the operator at 416-695-7848 or toll free 1-800-766-6630 prior to the scheduled start time or you may listen to the call via webcast by following the link on the Company's website at www.b2gold.com.

A playback version of the call will be available for one week after the call by dialing 905-694-9451 or toll free 1-800-408-3053 (pass code: 1251652).

ON BEHALF OF B2GOLD CORP.

Clive T. Johnson, President and Chief Executive Officer

For more information on B2Gold please visit the Company web site at www.b2gold.com.

The securities described herein have not been and will not be registered under the United States Securities Act of 1933, as amended, and may not be offered or sold in the United States absent registration or an applicable exemption from registration requirements.

Some of the statements contained in this release are forward-looking statements, such as estimates and statements that describe the Company's future plans, objectives or goals, including words to the effect that the Company or management expects a stated condition or result to occur. Since forward-looking statements address future events and conditions, by their very nature, they involve inherent risks and uncertainties. Actual results in each case could differ materially from those currently anticipated in such statements.

The Toronto Stock Exchange neither approves nor disapproves the information contained in this News Release.

Contacts:

B2Gold Corp.

Ian MacLean

Vice President, Investor Relations

604-681-8371

B2Gold Corp.

Kerry Suffolk

Manager, Investor Relations

604-681-8371

www.b2gold.com

© 2011 MarketWir

News Release

B2Gold Reports on Second Quarter 2011 Results

Vancouver, August 11, 2011

http://cnrp.marketwire.com/cnrp_files/20110811-bto811.pdf

B2Gold Reports on Second Quarter 2011 Results

Vancouver, August 11, 2011

http://cnrp.marketwire.com/cnrp_files/20110811-bto811.pdf

Expert Analysis

Steven Green, TD Newcrest (7/29/11) "B2Gold Corp. released Q2 production results that were above our estimates, due to higher grades at La Libertad and higher recoveries and grades at Limon; in addition, the company raised 2011 production guidance by 5 Koz. to 135–145 Koz. . .we have increased our production estimates accordingly and are maintaining a Buy recommendation. . .B2Gold continues to deliver solid operating results and has above-average exploration upside, in our view."

Richard Gray, Cormark Securities (7/29/11) "B2Gold Corp. provides exploration upside on the back of a proven management team with an excellent track record for discovering, developing and operating gold mines in challenging environments. . .Q2 production of 36,760 oz. was well above our estimate for the quarter of 31,900 oz. . .we continue to recommend the stock as our Top Pick and believe the company provides one of the sector's best combinations of production growth, attractive valuation and exploration upside."

Steven Butler, Canaccord Genuity (7/28/11) "B2Gold Corp.'s consolidated production guidance for 2011 has been revised upwards by 5 Koz. to 135–145 Koz., based on higher expected recoveries and grades at La Libertad. We reiterate our Buy rating, based on production growth and reserve upside from a solid production platform, rerating and valuation upside on derisking the Gramalote project and the potential for a further increase in guidance following the incorporation of higher-grade colluvium material from Jabali into the mine plan."

Ron Struthers, Struthers Resource Stock Report (7/20/11) "The future looks very bright for B2Gold. . .there is potential for high grade discoveries at Limon to enhance production levels, considering historical mined grades in the largely unexplored district; the company's Gramalote JV has great potential for a larger resource and advancement through a prefeasibility study that could materially add value to the stock. They also have significant upside to potentially sizeable discoveries at the Cebollati project in Uruguay and Trebol/Pavon JV in Nicaragua, where the limited exploration undertaken to date has returned encouraging results.

http://www.theaureport.com/pub/co/819" target="_blank" rel="nofollow ugc noopener">

http://www.theaureport.com/pub/co/819

Steven Green, TD Newcrest (7/29/11) "B2Gold Corp. released Q2 production results that were above our estimates, due to higher grades at La Libertad and higher recoveries and grades at Limon; in addition, the company raised 2011 production guidance by 5 Koz. to 135–145 Koz. . .we have increased our production estimates accordingly and are maintaining a Buy recommendation. . .B2Gold continues to deliver solid operating results and has above-average exploration upside, in our view."

Richard Gray, Cormark Securities (7/29/11) "B2Gold Corp. provides exploration upside on the back of a proven management team with an excellent track record for discovering, developing and operating gold mines in challenging environments. . .Q2 production of 36,760 oz. was well above our estimate for the quarter of 31,900 oz. . .we continue to recommend the stock as our Top Pick and believe the company provides one of the sector's best combinations of production growth, attractive valuation and exploration upside."

Steven Butler, Canaccord Genuity (7/28/11) "B2Gold Corp.'s consolidated production guidance for 2011 has been revised upwards by 5 Koz. to 135–145 Koz., based on higher expected recoveries and grades at La Libertad. We reiterate our Buy rating, based on production growth and reserve upside from a solid production platform, rerating and valuation upside on derisking the Gramalote project and the potential for a further increase in guidance following the incorporation of higher-grade colluvium material from Jabali into the mine plan."

Ron Struthers, Struthers Resource Stock Report (7/20/11) "The future looks very bright for B2Gold. . .there is potential for high grade discoveries at Limon to enhance production levels, considering historical mined grades in the largely unexplored district; the company's Gramalote JV has great potential for a larger resource and advancement through a prefeasibility study that could materially add value to the stock. They also have significant upside to potentially sizeable discoveries at the Cebollati project in Uruguay and Trebol/Pavon JV in Nicaragua, where the limited exploration undertaken to date has returned encouraging results.

http://www.theaureport.com/pub/co/819" target="_blank" rel="nofollow ugc noopener">

http://www.theaureport.com/pub/co/819

Erneutes ATH und erstmalig über 4 Can$!!

Eine der besten Aktien zur Zeit... und kaum einer bekommt's mit!

Eine der besten Aktien zur Zeit... und kaum einer bekommt's mit!

B2Gold Corp. and Radius Gold Inc. Provide Nicaragua Update: Trebol East Trench Returns 18.00 Metres at 2.56 Grams Per Tonne Gold

VANCOUVER, BRITISH COLUMBIA -- (Marketwire) -- 08/23/11

http://www.finanznachrichten.de/nachrichten-2011-08/21149720…

VANCOUVER, BRITISH COLUMBIA -- (Marketwire) -- 08/23/11

http://www.finanznachrichten.de/nachrichten-2011-08/21149720…

1,7 Mio Stücke in nur 2 Stunden, unglaublich...

Antwort auf Beitrag Nr.: 42.002.593 von Videomart am 25.08.11 16:30:30...sorry, es war sogar nur eine Stunde!!

"The Gold Report"

Expert Analysis

Canaccord Morning Coffee (8/24/11) "B2Gold Corp. and Radius Gold announced trenching results from their Trebol project in northeastern Nicaragua. . .new trench results appear to be outlining a north-south trending mineralized zone at least 1.5 km. long: Trench 91, which lies at the southern end of the trend, returned 18m at 2.56 g/t gold; roughly 1 km. north, trench 93 returned 19m at 1.54 g/t gold. . .this news continues a solid string of results from B2Gold, as the company continues to ramp up production from its La Libertad and La Limon mines in Nicaragua along with exploration upside from its Cebollati property in Uruguay."

Michael Gray, Macquarie Capital Markets (8/15/11) "B2Gold Corp. reported Q211 results with adjusted earnings per share of $0.06, in line with our estimate. . .gold production of 36.8 Koz. was pre-released and 12% higher than our 33.0 Koz. estimate while cash operating costs of $507/oz. were 18% lower than our estimate of $616/oz. The company achieved higher than expected gold production at lower cash operating costs while providing investors exposure to key exploration upside. . .we reiterate our Outperform recommendation. . .B2Gold is one of our top picks amongst the mid-tier gold producers."

Richard Gray, Cormark Securities (8/12/11) "B2Gold Corp. has been the rare gold producer that has lowered its cash costs as the gold price has increased without the help of any by-product credits; this has driven a dramatic increase in margins for the company, a trend we expect to continue in Q311 with gold trading where it is now. With further upside coming from the drilling and development at Gramalote, we continue to recommend the stock as our Top Pick and believe the company provides one of the sector's best combinations of production growth, attractive valuation and exploration upside."

Steven Green, TD Newcrest (7/29/11) "B2Gold Corp. released Q2 production results that were above our estimates, due to higher grades at La Libertad and higher recoveries and grades at Limon; in addition, the company raised 2011 production guidance by 5 Koz. to 135–145 Koz. . .we have increased our production estimates accordingly and are maintaining a Buy recommendation. . .B2Gold continues to deliver solid operating results and has above-average exploration upside, in our view."

Richard Gray, Cormark Securities (7/29/11) "B2Gold Corp. provides exploration upside on the back of a proven management team with an excellent track record for discovering, developing and operating gold mines in challenging environments. . .Q2 production of 36,760 oz. was well above our estimate for the quarter of 31,900 oz. . .we continue to recommend the stock as our Top Pick and believe the company provides one of the sector's best combinations of production growth, attractive valuation and exploration upside."

http://www.theaureport.com/pub/co/819

Expert Analysis

Canaccord Morning Coffee (8/24/11) "B2Gold Corp. and Radius Gold announced trenching results from their Trebol project in northeastern Nicaragua. . .new trench results appear to be outlining a north-south trending mineralized zone at least 1.5 km. long: Trench 91, which lies at the southern end of the trend, returned 18m at 2.56 g/t gold; roughly 1 km. north, trench 93 returned 19m at 1.54 g/t gold. . .this news continues a solid string of results from B2Gold, as the company continues to ramp up production from its La Libertad and La Limon mines in Nicaragua along with exploration upside from its Cebollati property in Uruguay."

Michael Gray, Macquarie Capital Markets (8/15/11) "B2Gold Corp. reported Q211 results with adjusted earnings per share of $0.06, in line with our estimate. . .gold production of 36.8 Koz. was pre-released and 12% higher than our 33.0 Koz. estimate while cash operating costs of $507/oz. were 18% lower than our estimate of $616/oz. The company achieved higher than expected gold production at lower cash operating costs while providing investors exposure to key exploration upside. . .we reiterate our Outperform recommendation. . .B2Gold is one of our top picks amongst the mid-tier gold producers."

Richard Gray, Cormark Securities (8/12/11) "B2Gold Corp. has been the rare gold producer that has lowered its cash costs as the gold price has increased without the help of any by-product credits; this has driven a dramatic increase in margins for the company, a trend we expect to continue in Q311 with gold trading where it is now. With further upside coming from the drilling and development at Gramalote, we continue to recommend the stock as our Top Pick and believe the company provides one of the sector's best combinations of production growth, attractive valuation and exploration upside."

Steven Green, TD Newcrest (7/29/11) "B2Gold Corp. released Q2 production results that were above our estimates, due to higher grades at La Libertad and higher recoveries and grades at Limon; in addition, the company raised 2011 production guidance by 5 Koz. to 135–145 Koz. . .we have increased our production estimates accordingly and are maintaining a Buy recommendation. . .B2Gold continues to deliver solid operating results and has above-average exploration upside, in our view."

Richard Gray, Cormark Securities (7/29/11) "B2Gold Corp. provides exploration upside on the back of a proven management team with an excellent track record for discovering, developing and operating gold mines in challenging environments. . .Q2 production of 36,760 oz. was well above our estimate for the quarter of 31,900 oz. . .we continue to recommend the stock as our Top Pick and believe the company provides one of the sector's best combinations of production growth, attractive valuation and exploration upside."

http://www.theaureport.com/pub/co/819

Outperformance by gold bullion makes gold stocks very cheap - Charles Oliver

It's a good time to stock up on gold stocks says Charles Oliver, senior portfolio manager with Sprott Asset Management, who sees a number of the equities trading at their lowest prices of the decade. Gold Report interview

Author: Brian Sylvester

Posted: Tuesday , 23 Aug 2011

http://www.mineweb.com/mineweb/view/mineweb/en/page33?oid=13…

It's a good time to stock up on gold stocks says Charles Oliver, senior portfolio manager with Sprott Asset Management, who sees a number of the equities trading at their lowest prices of the decade. Gold Report interview

Author: Brian Sylvester

Posted: Tuesday , 23 Aug 2011

http://www.mineweb.com/mineweb/view/mineweb/en/page33?oid=13…

B2gold Corp (BTO.TO)

Institutional Holders

% Shares Owned: 54.89%

# of Holders: 50

Total Shares Held: 188,181,720

3 Mo. Net Change: 1,331,726

# New Positions: 8

# Closed Positions: 1

# Increased Positions: 24

# Reduced Positions: 5

# Net Buyers: 19

http://www.reuters.com/finance/stocks/financialHighlights?sy…

Institutional Holders

% Shares Owned: 54.89%

# of Holders: 50

Total Shares Held: 188,181,720

3 Mo. Net Change: 1,331,726

# New Positions: 8

# Closed Positions: 1

# Increased Positions: 24

# Reduced Positions: 5

# Net Buyers: 19

http://www.reuters.com/finance/stocks/financialHighlights?sy…

05.09.2011 (CIBC WORLD MARKETS)

...

Der positive Goldpreistrend dürfte sich weiter fortsetzen. Es wäre wenig überraschend, wenn die Unsicherheiten wegen der Schuldenkrise und den Währungsschwankungen zu weiteren Anstiegen führen würden. Die Preisannahmen seien für 2011 und 2012 auf 1.625 USD sowie 2.000 USD pro Unze angehoben worden. In 2013 werde mit einem weiteren Anstieg auf 2.200 USD gerechnet. Der Silberpreis dürfte bis 2013 nur schrittweise und weniger stark vorankommen als der Goldpreis, da hier das Nachfrage/Angebots-Verhältnis knapper sei.

Die aktuellen Bewegungen beim Goldpreis würden oft mit einer Blase verglichen, wie Ende der 70er Jahre. Diese Einschätzung werde jedoch nicht geteilt, da derzeit komplett andere Bedingungen herrschen würden. Der Kauf von Goldaktien dürfte vorteilhafter sein als ein Goldbarren-Investment. Die Cash flow-Multiplen würden sich fast auf historischen Tiefstständen befinden. Goldaktien würden fast zu den gleichen NAV-Multiplen gehandelt wie Basismetall-Titel. Dabei seien wegen der monetären Aspekte besondere Prämien gerechtfertigt.

Zu den besten Performern dürften kleinere Gold-Titel zählen, bei denen Wachstum, wenn auch noch nicht geliefert, vom Markt belohnt werde. Die Schere zwischen Value und Wachstum gehe immer weiter auseinander.

...

http://www.onvista.de/analysen/empfehlungen/artikel/05.09.20…

...

Der positive Goldpreistrend dürfte sich weiter fortsetzen. Es wäre wenig überraschend, wenn die Unsicherheiten wegen der Schuldenkrise und den Währungsschwankungen zu weiteren Anstiegen führen würden. Die Preisannahmen seien für 2011 und 2012 auf 1.625 USD sowie 2.000 USD pro Unze angehoben worden. In 2013 werde mit einem weiteren Anstieg auf 2.200 USD gerechnet. Der Silberpreis dürfte bis 2013 nur schrittweise und weniger stark vorankommen als der Goldpreis, da hier das Nachfrage/Angebots-Verhältnis knapper sei.

Die aktuellen Bewegungen beim Goldpreis würden oft mit einer Blase verglichen, wie Ende der 70er Jahre. Diese Einschätzung werde jedoch nicht geteilt, da derzeit komplett andere Bedingungen herrschen würden. Der Kauf von Goldaktien dürfte vorteilhafter sein als ein Goldbarren-Investment. Die Cash flow-Multiplen würden sich fast auf historischen Tiefstständen befinden. Goldaktien würden fast zu den gleichen NAV-Multiplen gehandelt wie Basismetall-Titel. Dabei seien wegen der monetären Aspekte besondere Prämien gerechtfertigt.

Zu den besten Performern dürften kleinere Gold-Titel zählen, bei denen Wachstum, wenn auch noch nicht geliefert, vom Markt belohnt werde. Die Schere zwischen Value und Wachstum gehe immer weiter auseinander.

...

http://www.onvista.de/analysen/empfehlungen/artikel/05.09.20…

B2gold Corp (BTO.TO)

Institutional Holders

% Shares Owned: 68.88%

# of Holders: 54

Total Shares Held: 236,134,091

3 Mo. Net Change: 1,527,531

# New Positions: 8

# Closed Positions: 2

# Increased Positions: 26

# Reduced Positions: 8

# Net Buyers: 18

http://www.reuters.com/finance/stocks/financialHighlights?sy…

Institutional Holders

% Shares Owned: 68.88%

# of Holders: 54

Total Shares Held: 236,134,091

3 Mo. Net Change: 1,527,531

# New Positions: 8

# Closed Positions: 2

# Increased Positions: 26

# Reduced Positions: 8

# Net Buyers: 18

http://www.reuters.com/finance/stocks/financialHighlights?sy…

Gold auf ATH: 1920US$!!

absolut geiler chart ......

wenn man jetzt noch von Anfang an dabei wäre ......

wenn man jetzt noch von Anfang an dabei wäre ......

Insttutional Holders

% Shares Owned: 69.23%

# of Holders: 54

Total Shares Held: 237,357,271

3 Mo. Net Change: 2,750,711

# New Positions: 8

# Closed Positions: 2

# Increased Positions: 29

# Reduced Positions: 8

# Net Buyers: 21

http://www.reuters.com/finance/stocks/financialHighlights?sy…

% Shares Owned: 69.23%

# of Holders: 54

Total Shares Held: 237,357,271

3 Mo. Net Change: 2,750,711

# New Positions: 8

# Closed Positions: 2

# Increased Positions: 29

# Reduced Positions: 8

# Net Buyers: 21

http://www.reuters.com/finance/stocks/financialHighlights?sy…

ATH!!!

Institutional Holders

% Shares Owned: 71.50%

# of Holders: 58

Total Shares Held: 245,135,220

3 Mo. Net Change: 4,924,909

# New Positions: 8

# Closed Positions: 2

# Increased Positions: 32

# Reduced Positions: 8

# Net Buyers: 24

http://www.reuters.com/finance/stocks/financialHighlights?sy…

% Shares Owned: 71.50%

# of Holders: 58

Total Shares Held: 245,135,220

3 Mo. Net Change: 4,924,909

# New Positions: 8

# Closed Positions: 2

# Increased Positions: 32

# Reduced Positions: 8

# Net Buyers: 24

http://www.reuters.com/finance/stocks/financialHighlights?sy…

B2Gold Corp. Announces Further Positive Exploration Drill Results

from the Cebollati Project in Uruguay

Vancouver, September 16 , 2011

http://cnrp.marketwire.com/cnrp_files/20110915-bto0916.pdf

from the Cebollati Project in Uruguay

Vancouver, September 16 , 2011

http://cnrp.marketwire.com/cnrp_files/20110915-bto0916.pdf

Expert Analysis

Catherine Gignac, Northland Capital Partners:

16 September 2011

"B2Gold Corp. is a junior gold producer that is poised for resource expansion and long-term production; we expect a near seven-fold increase in gold production from its two Nicaraguan mines from 2009 to 2011. . .we anticipate significant upside to our price target from the delineation of high-grade targets on the company's mine properties. Management’s exceptional track record of discovery, exploration and development positions the company well ahead of its peers, in our view."

http://www.theaureport.com/pub/co/819#quote

Catherine Gignac, Northland Capital Partners:

16 September 2011

"B2Gold Corp. is a junior gold producer that is poised for resource expansion and long-term production; we expect a near seven-fold increase in gold production from its two Nicaraguan mines from 2009 to 2011. . .we anticipate significant upside to our price target from the delineation of high-grade targets on the company's mine properties. Management’s exceptional track record of discovery, exploration and development positions the company well ahead of its peers, in our view."

http://www.theaureport.com/pub/co/819#quote

Chinesische Goldnachfrage: Anstieg erwartet

15:27 21.09.11

http://www.ariva.de/news/Chinesische-Goldnachfrage-Anstieg-e…

15:27 21.09.11

http://www.ariva.de/news/Chinesische-Goldnachfrage-Anstieg-e…

Insider Trades by Symbol - TSX Venture Exchange

Company Name: B2Gold Corp.

Last Updated: September 22, 2011

Date: 09/22/2011

Symbol: BTO

Insider Buys Volume: 15,800

Insider Sells Volume: 0

Insider Buys Value $: 60,040.00

Insider Sells Value $: 0.00

Insider Buys Transaction: 2

Insider Sells Transaction: 0

Currency: CAD

http://www.tmxmoney.com/HttpController?GetPage=SearchInsider…

Company Name: B2Gold Corp.

Last Updated: September 22, 2011

Date: 09/22/2011

Symbol: BTO

Insider Buys Volume: 15,800

Insider Sells Volume: 0

Insider Buys Value $: 60,040.00

Insider Sells Value $: 0.00

Insider Buys Transaction: 2

Insider Sells Transaction: 0

Currency: CAD

http://www.tmxmoney.com/HttpController?GetPage=SearchInsider…

Expert Analysis

Richard Gray, Cormark Securities (9/20/11) "We expect B2Gold Corp. to see an upside rerating as it proves itself a stable gold producer. . .the company has provided consecutive updates to the market, each day highlighting its exploration and project development efforts from the company's primary growth projects: New higher grade resource definition from Jabali at La Libertad, the latest drill results from the early-stage Cebollati project in Uruguay and the joint-venture progress at Gramalote in Colombia. . .as La Libertad continues to produce more ounces, and with further upside coming through the drill bit, we continue to recommend the stock as our Top Pick and believe the company provides one of the sector's best combinations of production growth, attractive valuation and exploration upside."

Michael Berry, Morning Notes (9/20/11) "B2Gold announced further drill results and a pre-feasibility update from the company's Gramalote Project in Colombia. Pre-feasibility and exploration work recommenced at the Gramalote Project in the H2/10 with drilling for metallurgical samples, exploration drilling and preliminary engineering investigations with a total of 25,572.85m of drilling completed in 72 holes. B2Gold and AngloGold Ashanti are funding a 2011 pre-feasibility and exploration budget of US$37.6M. Highlights from the 2011 pre-feasibility and exploration work include positive metallurgical test results showing in excess of 90% recovery, encouraging drill results from the outside targets and consistent grade from the infill drilling on the Gramalote Ridge resource. Meanwhile, highlights from the drill results include GR-121, which yielded 180m of 1.09 g/t gold and hole GR-116, which returned 142m of 1.49 g/t gold. The Gramalote property is 51% owned by AngloGold Ashanti and 49% B2Gold."

Michael Gray, Macquarie Capital Markets (9/19/11) "B2Gold Corp. reported a prefeasibility update and exploration results at its Gramalote joint venture project. . .initial results suggest the ore is amenable to leaching and gravity as well as flotation, with recoveries in excess of 90%. . .the amenable metallurgy supports increasing the value per oz. in our model. . .with ongoing drilling at the fringes of the deposit and to depth there is upside potential to document a substantially larger resource by pulling a deeper pit using higher gold prices. Exploration drilling of five satellite targets within 4 km. of the current resource is ongoing. . .four of the five [holes] returned significant results. . .this update is a key development and we now model an extra 1 Moz.—we reiterate our Outperform recommendation and CAD$4.75 target."

Morning Coffee (9/19/11) "B2Gold Corp. reported further positive drill results from its Cebollati gold project in Uruguay. . .the company has new holes following up on the initial drill holes, which confirmed the presence of significant gold-bearing, replacement-style mineralization within multiple zones. Highlights from the drill results include hole UC11-019, which yielded 11.15m of 11.59 g/t gold with a broader intercept of 23.85m of 5.69 g/t gold. . .tighter-spaced drilling confirmed the existence of zones of continuous, shallow mineralization within the Windmill and Southern zones, which are open along strike and to depth."

http://www.theaureport.com/pub/co/819#quote

Richard Gray, Cormark Securities (9/20/11) "We expect B2Gold Corp. to see an upside rerating as it proves itself a stable gold producer. . .the company has provided consecutive updates to the market, each day highlighting its exploration and project development efforts from the company's primary growth projects: New higher grade resource definition from Jabali at La Libertad, the latest drill results from the early-stage Cebollati project in Uruguay and the joint-venture progress at Gramalote in Colombia. . .as La Libertad continues to produce more ounces, and with further upside coming through the drill bit, we continue to recommend the stock as our Top Pick and believe the company provides one of the sector's best combinations of production growth, attractive valuation and exploration upside."

Michael Berry, Morning Notes (9/20/11) "B2Gold announced further drill results and a pre-feasibility update from the company's Gramalote Project in Colombia. Pre-feasibility and exploration work recommenced at the Gramalote Project in the H2/10 with drilling for metallurgical samples, exploration drilling and preliminary engineering investigations with a total of 25,572.85m of drilling completed in 72 holes. B2Gold and AngloGold Ashanti are funding a 2011 pre-feasibility and exploration budget of US$37.6M. Highlights from the 2011 pre-feasibility and exploration work include positive metallurgical test results showing in excess of 90% recovery, encouraging drill results from the outside targets and consistent grade from the infill drilling on the Gramalote Ridge resource. Meanwhile, highlights from the drill results include GR-121, which yielded 180m of 1.09 g/t gold and hole GR-116, which returned 142m of 1.49 g/t gold. The Gramalote property is 51% owned by AngloGold Ashanti and 49% B2Gold."

Michael Gray, Macquarie Capital Markets (9/19/11) "B2Gold Corp. reported a prefeasibility update and exploration results at its Gramalote joint venture project. . .initial results suggest the ore is amenable to leaching and gravity as well as flotation, with recoveries in excess of 90%. . .the amenable metallurgy supports increasing the value per oz. in our model. . .with ongoing drilling at the fringes of the deposit and to depth there is upside potential to document a substantially larger resource by pulling a deeper pit using higher gold prices. Exploration drilling of five satellite targets within 4 km. of the current resource is ongoing. . .four of the five [holes] returned significant results. . .this update is a key development and we now model an extra 1 Moz.—we reiterate our Outperform recommendation and CAD$4.75 target."

Morning Coffee (9/19/11) "B2Gold Corp. reported further positive drill results from its Cebollati gold project in Uruguay. . .the company has new holes following up on the initial drill holes, which confirmed the presence of significant gold-bearing, replacement-style mineralization within multiple zones. Highlights from the drill results include hole UC11-019, which yielded 11.15m of 11.59 g/t gold with a broader intercept of 23.85m of 5.69 g/t gold. . .tighter-spaced drilling confirmed the existence of zones of continuous, shallow mineralization within the Windmill and Southern zones, which are open along strike and to depth."

http://www.theaureport.com/pub/co/819#quote

Institutional Holders

Shares Owned: 75.24%

# of Holders: 60

Total Shares Held: 258,914,916

3 Mo. Net Change: 13,224,065

# New Positions: 9

# Closed Positions: 3

# Increased Positions: 33

# Reduced Positions: 10

# Net Buyers: 23

http://www.reuters.com/finance/stocks/financialHighlights?sy…

Shares Owned: 75.24%

# of Holders: 60

Total Shares Held: 258,914,916

3 Mo. Net Change: 13,224,065

# New Positions: 9

# Closed Positions: 3

# Increased Positions: 33

# Reduced Positions: 10

# Net Buyers: 23

http://www.reuters.com/finance/stocks/financialHighlights?sy…

Der Anteil der "Instis" bei BTO ist z.Zt. höher als der bei Kinross...

http://www.reuters.com/finance/stocks/financialHighlights?sy…

http://www.reuters.com/finance/stocks/financialHighlights?sy…

Gold to Move 'Above $2,000 in Coming Months': UBS

Thursday September 29, 2011, 10:07 am EDT

Gold's recent sell-off belies its long term attractiveness and investors should avoid the panic and stay faithful to the precious metal, Dominic Schnider, Commodities expert at UBS Wealth Management told CNBC Thursday.

"The structural problems still remain and Greece is really going to call for higher prices and higher demand.

So we are looking at $2,000 and above in some of the months to come," Schnider said.

He dismissed notions that the gold bubble was close to bursting but cautioned that investors should expect more falls in the short term.

"In the short term you might see some further downside in the price but the demand side is still there," he said.

Gold has lost much of its sheen in recent days as part of a wider metals sell off and the strength of the US dollar in the face of stock market volatility over wider macro-economic woes.

An arrest in the rise of the metal saw a number of commentators claiming that the gold sell-off could see the price of the precious metal plummet to below the $1,500 level.

Marc Faber, author of the Gloom Boom, and Doom Report, told CNBC earlier this week that he would not be surprised if a 40 percent price correction occurred, causing gold to bottom out at $1,100 to $1,200.

Schnider added that gold would remain a safe haven because market volatility was so sharp but an increased desire by investors for liquidity could hamper its revival to the upside.

"If there is a liquidity crunch then even gold is going to have difficulty holding off and then cash is king. Gold is being driven weaker because of investors' desire for more liquidity," Schnider said.

Hampering another rally in gold prices is the strength of the dollar trade, but Schnider said demand for the dollar would be short term.

"It's all about the fear trade and risk aversion is shooting up and gold should be supportive on the one hand but if you seek liquidity it's all about the U.S. dollar. The dollar strength is just short term because the structural story remains unpleasant," Schnider said.

http://finance.yahoo.com/news/Gold-to-Move-Above-2000-in-cnb…

Thursday September 29, 2011, 10:07 am EDT

Gold's recent sell-off belies its long term attractiveness and investors should avoid the panic and stay faithful to the precious metal, Dominic Schnider, Commodities expert at UBS Wealth Management told CNBC Thursday.

"The structural problems still remain and Greece is really going to call for higher prices and higher demand.

So we are looking at $2,000 and above in some of the months to come," Schnider said.

He dismissed notions that the gold bubble was close to bursting but cautioned that investors should expect more falls in the short term.

"In the short term you might see some further downside in the price but the demand side is still there," he said.

Gold has lost much of its sheen in recent days as part of a wider metals sell off and the strength of the US dollar in the face of stock market volatility over wider macro-economic woes.

An arrest in the rise of the metal saw a number of commentators claiming that the gold sell-off could see the price of the precious metal plummet to below the $1,500 level.

Marc Faber, author of the Gloom Boom, and Doom Report, told CNBC earlier this week that he would not be surprised if a 40 percent price correction occurred, causing gold to bottom out at $1,100 to $1,200.

Schnider added that gold would remain a safe haven because market volatility was so sharp but an increased desire by investors for liquidity could hamper its revival to the upside.

"If there is a liquidity crunch then even gold is going to have difficulty holding off and then cash is king. Gold is being driven weaker because of investors' desire for more liquidity," Schnider said.

Hampering another rally in gold prices is the strength of the dollar trade, but Schnider said demand for the dollar would be short term.

"It's all about the fear trade and risk aversion is shooting up and gold should be supportive on the one hand but if you seek liquidity it's all about the U.S. dollar. The dollar strength is just short term because the structural story remains unpleasant," Schnider said.

http://finance.yahoo.com/news/Gold-to-Move-Above-2000-in-cnb…

Anteil der "Institutional Holders" gesunken:

% Shares Owned: 53.11%

# of Holders: 42

Total Shares Held: 182,758,516

3 Mo. Net Change: 13,713,255

# New Positions: 8

# Closed Positions: 3

# Increased Positions: 20

# Reduced Positions: 9

# Net Buyers: 11

http://www.reuters.com/finance/stocks/financialHighlights?sy…

% Shares Owned: 53.11%

# of Holders: 42

Total Shares Held: 182,758,516

3 Mo. Net Change: 13,713,255

# New Positions: 8

# Closed Positions: 3

# Increased Positions: 20

# Reduced Positions: 9

# Net Buyers: 11

http://www.reuters.com/finance/stocks/financialHighlights?sy…

Cormark Securities - B2Gold "Top Pick"

08:50 07.10.11

Rating-Update:

Toronto (aktiencheck.de AG) - Mike Kozak, Analyst von Cormark Securities, stuft die Aktie von B2Gold (B2Gold Corp. Aktie) unverändert mit "Top Pick" ein. Das Kursziel werde bei 5,75 Kanadischen Dollar gesehen. (Analyse vom 06.10.11) (07.10.2011/ac/a/u)

http://www.ariva.de/news/B2Gold-Top-Pick-Cormark-Securities-…

Richard Gray, Cormark Securities (10/6/11)

"B2Gold is a gold producer that is expected to see an upside rerating as it proves itself as a stable gold producer, growing production to an anticipated 170,000 oz next year. B2Gold also provides significant exploration upside, on the back of a proven management team with an excellent track record for discovering, developing and operating gold mines in challenging environments."

http://www.theaureport.com/pub/co/819?cover=1

08:50 07.10.11

Rating-Update:

Toronto (aktiencheck.de AG) - Mike Kozak, Analyst von Cormark Securities, stuft die Aktie von B2Gold (B2Gold Corp. Aktie) unverändert mit "Top Pick" ein. Das Kursziel werde bei 5,75 Kanadischen Dollar gesehen. (Analyse vom 06.10.11) (07.10.2011/ac/a/u)

http://www.ariva.de/news/B2Gold-Top-Pick-Cormark-Securities-…

Richard Gray, Cormark Securities (10/6/11)

"B2Gold is a gold producer that is expected to see an upside rerating as it proves itself as a stable gold producer, growing production to an anticipated 170,000 oz next year. B2Gold also provides significant exploration upside, on the back of a proven management team with an excellent track record for discovering, developing and operating gold mines in challenging environments."

http://www.theaureport.com/pub/co/819?cover=1

October 11, 2011 - 8:21 AM EDT

B2Gold Corp. and Auryx Gold Corp. Sign Binding Agreement for Proposed Business Combination

VANCOUVER, BRITISH COLUMBIA--(Marketwire - Oct. 11, 2011)

http://app.quotemedia.com/quotetools/newsStoryPopup.go?story…

B2Gold Corp. and Auryx Gold Corp. Sign Binding Agreement for Proposed Business Combination

VANCOUVER, BRITISH COLUMBIA--(Marketwire - Oct. 11, 2011)

http://app.quotemedia.com/quotetools/newsStoryPopup.go?story…

B2Gold Corp. kauft Auryx Gold Corp. für 160 Mio. CAD

11.10.2011 | 15:10 Uhr

B2Gold Corporation und Auryx Gold Corporation gaben heute bekannt, dass man eine bindende Bereinbarung getroffen habe, wonach es zu einem Zusammenschluss der beiden Unternehmen kommen wird. Je Auryx-Aktie erhalten Aktionäre 0,23 Aktien von B2Gold und 0,001$ in bar - dies entspricht 0,88 CAD je Auryx-Aktie.

Das zusammengeschlossene Unternehmen wird 92% der Anteile an dem Otjikoto-Goldprojekt in Namibia sowie 100% an zwei weiteren Explorationsprojekten in Namibia besitzen.

Der Vorstand von Auryx empfiehlt den Aktionären einstimmig, für die Transaktion mit B2Gold zu stimmen.

http://www.rohstoff-welt.de/news/artikel.php?sid=30653

11.10.2011 | 15:10 Uhr

B2Gold Corporation und Auryx Gold Corporation gaben heute bekannt, dass man eine bindende Bereinbarung getroffen habe, wonach es zu einem Zusammenschluss der beiden Unternehmen kommen wird. Je Auryx-Aktie erhalten Aktionäre 0,23 Aktien von B2Gold und 0,001$ in bar - dies entspricht 0,88 CAD je Auryx-Aktie.

Das zusammengeschlossene Unternehmen wird 92% der Anteile an dem Otjikoto-Goldprojekt in Namibia sowie 100% an zwei weiteren Explorationsprojekten in Namibia besitzen.

Der Vorstand von Auryx empfiehlt den Aktionären einstimmig, für die Transaktion mit B2Gold zu stimmen.

http://www.rohstoff-welt.de/news/artikel.php?sid=30653

Auf ein neues!!

B2Gold Corp. and Auryx Gold Corp. Sign Binding Agreement for Proposed Business Combination

Monday , 24 Oct 2011

http://www.mineweb.com/mineweb/view/mineweb/en/page674?oid=1…

Monday , 24 Oct 2011

http://www.mineweb.com/mineweb/view/mineweb/en/page674?oid=1…

B2Gold sector outperform

Vancouver (aktiencheck.de AG) - Chris Thompson und Ben Asuncion, Analysten von Haywood Securities, stufen die Aktie von B2Gold (ISIN CA11777Q2099/ WKN A0M889) von "sector perform" auf "sector outperform" hoch. Das Kursziel sehe man unverändert bei 4,40 USD. (Analyse vom 12.10.2011) (13.10.2011/ac/a/a)

http://www.finanzen.net/analyse/B2Gold_sector_outperform-Hay…

Vancouver (aktiencheck.de AG) - Chris Thompson und Ben Asuncion, Analysten von Haywood Securities, stufen die Aktie von B2Gold (ISIN CA11777Q2099/ WKN A0M889) von "sector perform" auf "sector outperform" hoch. Das Kursziel sehe man unverändert bei 4,40 USD. (Analyse vom 12.10.2011) (13.10.2011/ac/a/a)

http://www.finanzen.net/analyse/B2Gold_sector_outperform-Hay…

B2Gold sees next mine in Africa following $160m Auryx takeover

In a conference call with analysts and investors, B2Gold President and CEO Clive Johnson outlines a future for Auryx's Otjikoto gold project in Namibia as its next operating mine.

Author: Kip Keen

Posted: Wednesday , 12 Oct 2011

http://www.mineweb.com/mineweb/view/mineweb/en/page67?oid=13…

In a conference call with analysts and investors, B2Gold President and CEO Clive Johnson outlines a future for Auryx's Otjikoto gold project in Namibia as its next operating mine.

Author: Kip Keen

Posted: Wednesday , 12 Oct 2011

http://www.mineweb.com/mineweb/view/mineweb/en/page67?oid=13…

"Gold Miners' Leverage Effect Is Gone. But For How Long?"

"Although the mining stocks should have a leverage effect to a rising price of the metals they have in the ground, we can see that because of the financial crisis this leverage effect has often disappeared.

However, with the crisis in Europe only worsening, and the US on the brink of financial disaster, we think it's just a matter of time before the rating of the perceived "safe haven US Government bonds" will be lowered again.

When this happens, investors have nowhere to go but Gold. When the mass finally realizes that the mining stocks are severely undervalued, the mining companies could start a rally like you will only see once (or maybe twice if you're lucky enough to become old) in your life."

(www.bigtrends.com, October 26, 2011 10:02 PM)

http://www.bigtrends.com/technical-analysis/not-all-gold-sto…

"Although the mining stocks should have a leverage effect to a rising price of the metals they have in the ground, we can see that because of the financial crisis this leverage effect has often disappeared.

However, with the crisis in Europe only worsening, and the US on the brink of financial disaster, we think it's just a matter of time before the rating of the perceived "safe haven US Government bonds" will be lowered again.

When this happens, investors have nowhere to go but Gold. When the mass finally realizes that the mining stocks are severely undervalued, the mining companies could start a rally like you will only see once (or maybe twice if you're lucky enough to become old) in your life."

(www.bigtrends.com, October 26, 2011 10:02 PM)

http://www.bigtrends.com/technical-analysis/not-all-gold-sto…

David Goguen: Four Latin American Junior Takeover Targets Identified

Source: Brian Sylvester of The Gold Report (10/31/11)

http://m.ibtimes.com/gold-silver-copper-copper-gold-241455.h…

Source: Brian Sylvester of The Gold Report (10/31/11)

http://m.ibtimes.com/gold-silver-copper-copper-gold-241455.h…

Not all junior golds created equal

Eric Lam | Nov 2, 2011 – 9:02 AM ET

http://business.financialpost.com/2011/11/02/not-all-junior-…

Eric Lam | Nov 2, 2011 – 9:02 AM ET

http://business.financialpost.com/2011/11/02/not-all-junior-…

Gold equities, bullion provide safe passage through unchartered waters

According to Dundee Securities, gold equities and bullion have provided a safe haven over the last few months

and are expected to continue doing so into 2012

Author: Geoff Candy

Posted: Monday , 28 Nov 2011

http://www.mineweb.com/mineweb/view/mineweb/en/page33?oid=14…

According to Dundee Securities, gold equities and bullion have provided a safe haven over the last few months

and are expected to continue doing so into 2012

Author: Geoff Candy

Posted: Monday , 28 Nov 2011

http://www.mineweb.com/mineweb/view/mineweb/en/page33?oid=14…

The Gold Report Interview with Ron Struthers (11/18/11)

"I have a number of intermediate producers that I like. . .B2Gold Corp [is a] small-to-intermediate producer, because I think there's better value in the smaller producers."

Richard Gray, Cormark Securities (11/11/11)

"B2Gold Corp. is a stable gold producer with exceptional exploration upside, backed by a proven management team with a solid track record for discovering, developing and operating gold mines in challenging environments. . .margins continue to increase for B2Gold, a trend we expect to continue in 2012 as the higher-grade Jabali ore begins to be processed at Libertad. We continue to recommend the stock as our Top Pick and believe the company provides one of the sector's best combinations of production growth, attractive valuation and exploration upside."

Chris Thompson, Haywood Securities (11/11/11)

"B2Gold Corp. reported a positive Q311, driven by gold production more-or-less in line with expectations. . .Limon is primed to rebound from a flood challenged Q311; La Libertad is primed to enjoy a production boost from Jabali grades in 2012. Grades at Limon and La Libertad are expected to improve next year driving production growth from ~142 Koz to ~165 Koz. . .we reiterate our $4.40 target and Sector Outperform rating in anticipation of near-term production growth and development and exploration success."

Steven Green, TD Newcrest (11/11/11)

"We believe that B2Gold Corp. has a strong growth profile with potential for exploration upside in both brownfield and greenfield discoveries; management has been executing well through operational consistency, exploration success and making acquisitions in which they can add value. We are maintaining our Buy recommendation and have increased our target price to $5 from $4.75."

Steven Butler, Canaccord Genuity (11/10/11)

"We reiterate our Buy rating on B2Gold Corp. following the release of Q311 results that were operationally stronger than our expectations. Our recommendation is based on production growth and reserve upside from a solid production platform (La Libertad and Limon), rerating and valuation upside on derisking the Gramalote project and an attractive suite of exploration assets (including Cebollati and Trebol/Pavon). . .we also see further rerating potential on advancing the Otjikoto project, pending successful close of the Auryx acquisition."

http://www.theaureport.com/pub/co/819

PRESS RELEASES 12/1/2011 8:49:39 AM | Marketwire News

B2Gold Corp. Announces Further Positive Exploration Drill Results From La Libertad Mine Property in Nicaragua Increasing the Size of the Jabali Zones, and the Mojon West Deposit

B2Gold Corp. Announces Further Positive Exploration Drill Results From La Libertad Mine Property in Nicaragua Increasing the Size of the Jabali Zones, and the Mojon West Deposit

Südkorea stockt Goldbestände deutlich auf

Sektor Rohstoffe | Asien-News (Macquarie) | Uhrzeit: 12:06

http://www.boerse-go.de//nachricht/Suedkorea-stockt-Goldbest…

Positive Bohrergebnisse versprechen gute Aussichten für B2Gold

Autor: Björn Junker | 05.12.2011, 11:51

http://www.wallstreet-online.de/nachricht/3918960-produktion…

Autor: Björn Junker | 05.12.2011, 11:51

http://www.wallstreet-online.de/nachricht/3918960-produktion…

Canaccord Morning Coffee (12/2/11)

"B2Gold reported more positive drill results from its Jabali zone at its La Libertad mine in Nicaragua.

Highlighted holes include 6.9 m at 26.87 g/t drilled within the eastern end of Jabali zone and 11.4 m of 13.52 g/t drilled in

western part of the Antenna zone. Step-out drilling as far as 100 m west of Jabali returned 9.0 m of 2.99 g/t while west of the

Antenna zone returned 6.9 m of 3.54 g/t, 1.5 m of 13.8 g/t and 3.5 m of 5.23 g/t. Mineralization also hit as much as 250.0 m

beyond the western extent of current main Mojon vein pit, including 5.5 m of 10 g/t. Based on these positive results from Jabali

to date, the company has commenced full permitting, environmental studies and metallurgical test work. Due to the increasing

size of the Jabali Zones, a new resource estimate for the Jabali Central and Antenna deposits will now be completed by March

2012. B2Gold is projected to produce 93,000-99,000 ounces of gold from La Libertad open-pit mine in 2011. The company also

noted that their Auryx Gold (AYX) transaction is proceeding well with 13.5% of outstanding shares having been locked up thus

far with the Board recommending that shareholders approve the transaction. The combination of B2Gold and Auryx will result

in B2Gold acquiring a 92% interest in the Otjikoto gold project in Namibia and a 100% interest in two additional exploration

projects in Namibia. The Otjikoto gold project has forecast life of mine annual production of approximately 100,000 ounces of

gold based on a Preliminary Economic Assessment released by Auryx in September 2011 with significant exploration

upside. The vote is set for December 15, 2011."

http://www.investorvillage.com/uploads/57919/files/DL_MorniC…

"B2Gold reported more positive drill results from its Jabali zone at its La Libertad mine in Nicaragua.

Highlighted holes include 6.9 m at 26.87 g/t drilled within the eastern end of Jabali zone and 11.4 m of 13.52 g/t drilled in

western part of the Antenna zone. Step-out drilling as far as 100 m west of Jabali returned 9.0 m of 2.99 g/t while west of the

Antenna zone returned 6.9 m of 3.54 g/t, 1.5 m of 13.8 g/t and 3.5 m of 5.23 g/t. Mineralization also hit as much as 250.0 m

beyond the western extent of current main Mojon vein pit, including 5.5 m of 10 g/t. Based on these positive results from Jabali

to date, the company has commenced full permitting, environmental studies and metallurgical test work. Due to the increasing

size of the Jabali Zones, a new resource estimate for the Jabali Central and Antenna deposits will now be completed by March

2012. B2Gold is projected to produce 93,000-99,000 ounces of gold from La Libertad open-pit mine in 2011. The company also

noted that their Auryx Gold (AYX) transaction is proceeding well with 13.5% of outstanding shares having been locked up thus

far with the Board recommending that shareholders approve the transaction. The combination of B2Gold and Auryx will result

in B2Gold acquiring a 92% interest in the Otjikoto gold project in Namibia and a 100% interest in two additional exploration

projects in Namibia. The Otjikoto gold project has forecast life of mine annual production of approximately 100,000 ounces of

gold based on a Preliminary Economic Assessment released by Auryx in September 2011 with significant exploration

upside. The vote is set for December 15, 2011."

http://www.investorvillage.com/uploads/57919/files/DL_MorniC…

Chris Thompson, Haywood Securities (1/10/12)

"With its acquisition of Auryx Gold Corp., B2Gold Corp. fortifies its near-term development plans and adds geographic diversity. . .the company lays the foundation by acquiring Auryx for 92% of the Otjikoto project in Namibia to build a +300 Koz/year gold producer by 2015. . .an implied return of +40% justifies our Sector Outperform rating."

Michael Gray, Macquarie Capital Markets (1/23/12)

"B2Gold Corp. reported significant Au-Cu porphyry mineralization assay results in three holes (668m) from its Primavera joint-venture project in northeast Nicaragua. . .highlights are: 1.) 103m at 0.85 g/t Au and 0.324% Cu (starting from surface, hole 1); 2.) 261.7m at 0.78 g/t Au and 0.297% Cu (same pad, hole 2) and 3.) 77.35m at 0.74 g/t Au and 0.311% Cu from a stepout 200m to the southwest (hole 3). We reiterate our Outperform recommendation for the company and our target price of CA$5.50. . .B2Gold is a top pick amongst our intermediate producers."

Steven Butler, Canaccord Genuity (1/24/12)

"We reiterate our Buy rating on B2Gold Corp. following the announcement of Q411 production results, which were at the high end of management's guidance range. . .B2Gold remains a Canaccord Genuity Focus List pick ahead of a number of potentially positive catalysts that we believe should drive valuation upside and rerating potential over the next 12 months. . .consolidated gold production is expected to increase to 185 Koz in 2013 and further to 200 Koz by 2014, with estimated production growth to 450 Koz by 2016 (including Otjikoto and Gramalote)."

Richard Gray, Cormark Securities (1/24/12)

"B2Gold Corp.'s 2011 production of 144,604 oz was in line with guidance and our expectations. . .Otjikoto's timeline to production is being fast tracked and Jabali's contribution to La Libertad production is much larger than previously forecast. . .we continue to recommend the stock as our top pick and believe the company provides one of the sector's best combinations of production growth, attractive valuation and exploration upside."

Steven Green, TD Securities (1/24/12)