(PSDV) Mkap $30 M //3x Zugelassene Produkte// 1x Phase 3 = Verzehnfachung möglich - 500 Beiträge pro Seite

eröffnet am 05.12.12 14:02:11 von

neuester Beitrag 27.10.14 22:02:34 von

neuester Beitrag 27.10.14 22:02:34 von

Beiträge: 72

ID: 1.178.176

ID: 1.178.176

Aufrufe heute: 0

Gesamt: 16.481

Gesamt: 16.481

Aktive User: 0

ISIN: US74440J1016 · WKN: A0Q4DQ

Neuigkeiten

| Titel |

|---|

16.05.24 · globenewswire |

08.05.24 · globenewswire |

06.05.24 · globenewswire |

16.04.24 · globenewswire |

02.04.24 · globenewswire |

Werte aus der Branche Pharmaindustrie

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 1,5800 | +54,90 | |

| 0,5850 | +18,90 | |

| 112,75 | +16,48 | |

| 16,236 | +13,54 | |

| 816,90 | +11,17 |

| Wertpapier | Kurs | Perf. % |

|---|---|---|

| 16,100 | -15,26 | |

| 0,6550 | -16,56 | |

| 22,000 | -19,97 | |

| 3,7600 | -26,27 | |

| 0,7500 | -35,34 |

Heute möchte ich euch die wahrscheinlich unterbewerteste Aktie im gesamten Biotech Sektor vorstellen .

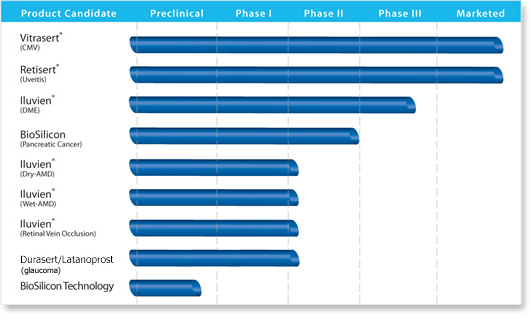

Psivida(PSDV) hat sich auf Augenkrankheiten spezialisiert und hat bereits 3x Zugelassene Produkte und weitere kandidaten in Phase 3 und Phase 2 .

Iluvien für DME (diabetischen Makulaödems) ist das jüngst Zugelassene Produkt . Iluvien ist das erste Wirkstoff das für die DME zugelassen ist und genau hier schlummert das riesige Potential .

Iluvien ist zwar schon in Europa zugelassen aber der Verkauf startet erst nächsten Quartal in Deutschland und dann folgen England ,Frankreich usw in den folgenden monaten .

PSDV und Partner ALIM wollen nächsten Quartal erneut die Zulassung für Iluvien in USA beantragen nachdem FDA diese schonmal abgelehnt hatte . Die Chancen auf Zulassung sind diesmal gut .

Was noch ?

Pfizer ist hier einer der größten Investoren mit 1.9 M aktien und auch Partner von PSDV . Das gemeinsame Produkt befindet sich gerade in Phase 2 .

Die Marktkap beträgt unglaublich lächerliche $30 M und davon sind knapp $18 M durch Cash gedeckt und ein weiterer pluspunkt ist das PSDV NULL schulden hat .

Psivida (PSDV)

Market Cap: $30 M

Cash: $17.65 M

Price: $1.30

Shares Out: 23.3

MEHR INFOS FOLGEN ....

Psivida(PSDV) hat sich auf Augenkrankheiten spezialisiert und hat bereits 3x Zugelassene Produkte und weitere kandidaten in Phase 3 und Phase 2 .

Iluvien für DME (diabetischen Makulaödems) ist das jüngst Zugelassene Produkt . Iluvien ist das erste Wirkstoff das für die DME zugelassen ist und genau hier schlummert das riesige Potential .

Iluvien ist zwar schon in Europa zugelassen aber der Verkauf startet erst nächsten Quartal in Deutschland und dann folgen England ,Frankreich usw in den folgenden monaten .

PSDV und Partner ALIM wollen nächsten Quartal erneut die Zulassung für Iluvien in USA beantragen nachdem FDA diese schonmal abgelehnt hatte . Die Chancen auf Zulassung sind diesmal gut .

Was noch ?

Pfizer ist hier einer der größten Investoren mit 1.9 M aktien und auch Partner von PSDV . Das gemeinsame Produkt befindet sich gerade in Phase 2 .

Die Marktkap beträgt unglaublich lächerliche $30 M und davon sind knapp $18 M durch Cash gedeckt und ein weiterer pluspunkt ist das PSDV NULL schulden hat .

Psivida (PSDV)

Market Cap: $30 M

Cash: $17.65 M

Price: $1.30

Shares Out: 23.3

MEHR INFOS FOLGEN ....

Hier ein paar folien von der Rodman Präsentation (sep 2012)

Umsatzzahlen die erwartet werden und das in nur 4 EU länder .Weitere EU länder werden hinzu kommen was natürlich noch mehr Umsatz bedeutet

Überblick Pfizer Deal

Finanzen

Umsatzzahlen die erwartet werden und das in nur 4 EU länder .Weitere EU länder werden hinzu kommen was natürlich noch mehr Umsatz bedeutet

Überblick Pfizer Deal

Finanzen

Und zu guter letzt ein Überblick auf die Investoren . Wie ihr unten seht sind einige Institutionellen damit beschäftigt die super günstigen aktien zu akkumulieren .

http://data.cnbc.com/quotes/PSDV/tab/8

Buyers 12/2/12 ---(5,053,134) <<<<<<<

Sellers 12/2/12 --- (588,820)

Top Institutional Holders

Allan Gray ...2.8M

Orbis Investment ...2.2M

Pfizer Inc ...1.9M

North Run ...960.0K

Palo Alto ...813.7K

Ashton (Paul) ...457.5K

Morgan Stanley ...274.2K

Dimensional Fund ...257.9K

The Pennsylvania ...133.4K

Janney ...131.4K

http://data.cnbc.com/quotes/PSDV/tab/8

Buyers 12/2/12 ---(5,053,134) <<<<<<<

Sellers 12/2/12 --- (588,820)

Top Institutional Holders

Allan Gray ...2.8M

Orbis Investment ...2.2M

Pfizer Inc ...1.9M

North Run ...960.0K

Palo Alto ...813.7K

Ashton (Paul) ...457.5K

Morgan Stanley ...274.2K

Dimensional Fund ...257.9K

The Pennsylvania ...133.4K

Janney ...131.4K

Antwort auf Beitrag Nr.: 43.893.383 von Biohero am 05.12.12 14:26:15und um uns diese unentdeckte "Perle" vorzustellen eröffnest du diesen

thread, obwohl es bereits hier einen thread mit mehr als

10 000 beiträgen (!) gibt, indem die investierten ihre verluste

salben...

die rodman - bewertungen kann man nmM. vergessen...das

kann ich aus langjähriger erfahrung mit sicherheit sagen...

und wann kommt jetzt die verzehnfachung - bitte den ball flach halten!

und dann kläre doch mal die interessierten hier auf wieviel tatächlich

in $ die company letztes jahr als gewinn ihrer bilanz zuschreiben

konnte aus den bereits zugelassenen produkten;

... und wie hoch ihre anteile an den gesamtumsätzen/gewinnen

sind

thread, obwohl es bereits hier einen thread mit mehr als

10 000 beiträgen (!) gibt, indem die investierten ihre verluste

salben...

die rodman - bewertungen kann man nmM. vergessen...das

kann ich aus langjähriger erfahrung mit sicherheit sagen...

und wann kommt jetzt die verzehnfachung - bitte den ball flach halten!

und dann kläre doch mal die interessierten hier auf wieviel tatächlich

in $ die company letztes jahr als gewinn ihrer bilanz zuschreiben

konnte aus den bereits zugelassenen produkten;

... und wie hoch ihre anteile an den gesamtumsätzen/gewinnen

sind

Antwort auf Beitrag Nr.: 43.894.231 von Gustl24 am 05.12.12 16:59:36und wann kommt jetzt die verzehnfachung - bitte den ball flach halten!

oben steht verzehnfachung MÖGLICH erst lesen dann screiben .Verzehnfachung würde gerade mal eine Marktkap von $300 M und das ist durchaus realistisch .

die rodman - bewertungen kann man nmM

das ist keine rodman bewertung sondern stamm von Alimera selbst nur die präsentation ist von rodman

......

oben steht verzehnfachung MÖGLICH erst lesen dann screiben .Verzehnfachung würde gerade mal eine Marktkap von $300 M und das ist durchaus realistisch .

die rodman - bewertungen kann man nmM

das ist keine rodman bewertung sondern stamm von Alimera selbst nur die präsentation ist von rodman

......

Trading Spotlight

Der Deal vorgestern mit Quintiles ist super wenn jemand Iluvien gutin Europa vermarkten kann dann die ..

Über Quintiles

Quintiles ist der weltweit führende Anbieter von biopharmazeutischen Dienstleistungen. Mit einem Netz von mehr als 27.000 Fachmitarbeitern in mehr als 80 Ländern war das Unternehmen an der Entwicklung oder Kommerzialisierung aller der Top 50 meistverkauften Arzneimittel auf dem Markt beteiligt. Dank unserer ausgedehnten Expertise in den Bereichen Therapie, wissenschaftliche Forschung und Analyse sind wir Kunden der Biopharma- und Gesundheitswissenschaftsbranche behilflich, sich durch das zunehmend komplexe Gelände hindurchzunavigieren, die Prognosen zu erleichtern und die Ergebnisse zu verbessern.

...........

Alimera Sciences Signs Agreement With Quintiles for European Commercial Launch of ILUVIEN®

ATLANTA, Dec. 4, 2012 /PRNewswire/ -- Alimera Sciences, Inc., (ALIM) (Alimera), a biopharmaceutical company that specializes in the research, development and commercialization of prescription ophthalmic pharmaceuticals, today announced it has signed a Master Services Agreement with Quintiles Commercial Europe Ltd. (Quintiles) for the commercial launch of ILUVIEN® in certain European countries. ILUVIEN is Alimera's product for the treatment of chronic diabetic macular edema considered insufficiently responsive to available therapies.

"We believe this strategic collaboration with Quintiles will be pivotal in achieving a successful launch of ILUVIEN in Europe, and at the outset, our initial launch market of Germany," said Dan Myers, president and chief executive officer, Alimera. "Quintiles' broad track-record in the implementation and execution of multi-country, European commercialization projects made the organization an ideal services provider for Alimera in support of the commercial launch of ILUVIEN in Europe."

Services provided by Quintiles under the Master Services Agreement may include marketing, brand management, sales promotion and detailing, market access, regulatory, medical science liaison and communications and advisory services in certain European countries. Under this agreement, Alimera and Quintiles will enter into individual project orders that will specify the services to be provided.

The German Project Order, the first under the Master Services Agreement, was signed November 28, 2012. Under this project order, Quintiles Commercial Germany GmbH will provide services related to recruitment, employment, deployment and administration of the ILUVIEN commercialization team in Germany through December 31, 2015. Alimera and Quintiles expect to sign additional project orders for similar services in the United Kingdom and France. Quintiles began interviewing and hiring personnel in Germany, the United Kingdom and France in September in anticipation of the execution of project orders in all three countries.

"This relationship leverages Quintiles' core commercial talent and strengths. In addition, as the healthcare landscape has become more complex, it is increasingly important to engage with multiple stakeholders across the patient pathway. We have the broad expertise and experience to make this happen," said Chris Pepler, senior vice president, Commercial Solutions at Quintiles. "As Alimera Sciences enters these critical markets, we are excited to partner with them to help drive the success of ILUVIEN in the European ophthalmic market."

About Quintiles

Quintiles is the world's leading provider of biopharmaceutical services. With a network of more than 27,000 professionals working in more than 80 countries, Quintiles has helped develop or commercialize all of the top 50 best selling drugs on the market. With extensive therapeutic, scientific and analytics expertise, Quintiles helps biopharmaceutical and health sciences customers navigate the increasingly complex landscape with more predictability to enable better outcomes.

Über Quintiles

Quintiles ist der weltweit führende Anbieter von biopharmazeutischen Dienstleistungen. Mit einem Netz von mehr als 27.000 Fachmitarbeitern in mehr als 80 Ländern war das Unternehmen an der Entwicklung oder Kommerzialisierung aller der Top 50 meistverkauften Arzneimittel auf dem Markt beteiligt. Dank unserer ausgedehnten Expertise in den Bereichen Therapie, wissenschaftliche Forschung und Analyse sind wir Kunden der Biopharma- und Gesundheitswissenschaftsbranche behilflich, sich durch das zunehmend komplexe Gelände hindurchzunavigieren, die Prognosen zu erleichtern und die Ergebnisse zu verbessern.

...........

Alimera Sciences Signs Agreement With Quintiles for European Commercial Launch of ILUVIEN®

ATLANTA, Dec. 4, 2012 /PRNewswire/ -- Alimera Sciences, Inc., (ALIM) (Alimera), a biopharmaceutical company that specializes in the research, development and commercialization of prescription ophthalmic pharmaceuticals, today announced it has signed a Master Services Agreement with Quintiles Commercial Europe Ltd. (Quintiles) for the commercial launch of ILUVIEN® in certain European countries. ILUVIEN is Alimera's product for the treatment of chronic diabetic macular edema considered insufficiently responsive to available therapies.

"We believe this strategic collaboration with Quintiles will be pivotal in achieving a successful launch of ILUVIEN in Europe, and at the outset, our initial launch market of Germany," said Dan Myers, president and chief executive officer, Alimera. "Quintiles' broad track-record in the implementation and execution of multi-country, European commercialization projects made the organization an ideal services provider for Alimera in support of the commercial launch of ILUVIEN in Europe."

Services provided by Quintiles under the Master Services Agreement may include marketing, brand management, sales promotion and detailing, market access, regulatory, medical science liaison and communications and advisory services in certain European countries. Under this agreement, Alimera and Quintiles will enter into individual project orders that will specify the services to be provided.

The German Project Order, the first under the Master Services Agreement, was signed November 28, 2012. Under this project order, Quintiles Commercial Germany GmbH will provide services related to recruitment, employment, deployment and administration of the ILUVIEN commercialization team in Germany through December 31, 2015. Alimera and Quintiles expect to sign additional project orders for similar services in the United Kingdom and France. Quintiles began interviewing and hiring personnel in Germany, the United Kingdom and France in September in anticipation of the execution of project orders in all three countries.

"This relationship leverages Quintiles' core commercial talent and strengths. In addition, as the healthcare landscape has become more complex, it is increasingly important to engage with multiple stakeholders across the patient pathway. We have the broad expertise and experience to make this happen," said Chris Pepler, senior vice president, Commercial Solutions at Quintiles. "As Alimera Sciences enters these critical markets, we are excited to partner with them to help drive the success of ILUVIEN in the European ophthalmic market."

About Quintiles

Quintiles is the world's leading provider of biopharmaceutical services. With a network of more than 27,000 professionals working in more than 80 countries, Quintiles has helped develop or commercialize all of the top 50 best selling drugs on the market. With extensive therapeutic, scientific and analytics expertise, Quintiles helps biopharmaceutical and health sciences customers navigate the increasingly complex landscape with more predictability to enable better outcomes.

PSDV hat die Zulassung in Spanien erhalten , die Markteinführung beginnt in diesem Quartal mit Deutschland dann folgt UK ,Frankreich usw .

Der richtige Kurstreiber wird aber die US Zulassung sein der Antrag dafür soll in diesem Quartal and die FDA geschickt werden danach dauert es ca 6 monate bis zur Zulassung falls FDA nicht ablehnt .

pSivida Corp. Announces Spain Grants ILUVIEN® Marketing Approval for Chronic Diabetic Macular Edema

pSivida Corp. (NASDAQ:PSDV - News), a leader in developing sustained release, drug delivery products for treatment of back-of-the-eye diseases, announced today that the Spanish Agency of Drugs and Medical Devices (Agencia Espanola de Medicamentos y Productos Sanitarios) granted marketing authorization to ILUVIEN® for the treatment of vision impairment associated with chronic diabetic macular edema (DME) considered insufficiently responsive to available therapies.

The Spanish authorization is the sixth national approval for ILUVIEN in the EU, preceded by Austria, the United Kingdom, Portugal, France and Germany. pSivida’s licensee Alimera Sciences, Inc. reported that it continues to work closely with the Italian regulatory authorities to secure marketing authorization in Italy. These marketing authorizations follow the completion of the Decentralized Regulatory Procedure (DCP) in the European Union (EU), in which the Medicines and Healthcare products Regulatory Agency (MHRA) in the United Kingdom, serving as the Reference Member State (RMS), delivered a positive outcome for ILUVIEN along with six Concerned Member States (CMS).

Dr. Paul Ashton, President and CEO, said, “We are pleased that ILUVIEN has now been granted marketing authorizations in six of the seven EU countries in which approval has been sought and look forward to its commercial launch in the EU.”

Alimera reported that it continues to expect the initial commercial launch of ILUVIEN in Germany during the first quarter of 2013 with its European management team now on board.

The International Diabetes Federation estimates that more than three million people are currently living with diabetes in Spain, approximately 160,000 of whom Alimera estimates suffer from vision loss associated with DME.

Der richtige Kurstreiber wird aber die US Zulassung sein der Antrag dafür soll in diesem Quartal and die FDA geschickt werden danach dauert es ca 6 monate bis zur Zulassung falls FDA nicht ablehnt .

pSivida Corp. Announces Spain Grants ILUVIEN® Marketing Approval for Chronic Diabetic Macular Edema

pSivida Corp. (NASDAQ:PSDV - News), a leader in developing sustained release, drug delivery products for treatment of back-of-the-eye diseases, announced today that the Spanish Agency of Drugs and Medical Devices (Agencia Espanola de Medicamentos y Productos Sanitarios) granted marketing authorization to ILUVIEN® for the treatment of vision impairment associated with chronic diabetic macular edema (DME) considered insufficiently responsive to available therapies.

The Spanish authorization is the sixth national approval for ILUVIEN in the EU, preceded by Austria, the United Kingdom, Portugal, France and Germany. pSivida’s licensee Alimera Sciences, Inc. reported that it continues to work closely with the Italian regulatory authorities to secure marketing authorization in Italy. These marketing authorizations follow the completion of the Decentralized Regulatory Procedure (DCP) in the European Union (EU), in which the Medicines and Healthcare products Regulatory Agency (MHRA) in the United Kingdom, serving as the Reference Member State (RMS), delivered a positive outcome for ILUVIEN along with six Concerned Member States (CMS).

Dr. Paul Ashton, President and CEO, said, “We are pleased that ILUVIEN has now been granted marketing authorizations in six of the seven EU countries in which approval has been sought and look forward to its commercial launch in the EU.”

Alimera reported that it continues to expect the initial commercial launch of ILUVIEN in Germany during the first quarter of 2013 with its European management team now on board.

The International Diabetes Federation estimates that more than three million people are currently living with diabetes in Spain, approximately 160,000 of whom Alimera estimates suffer from vision loss associated with DME.

Sind das dann heute die Auswirkungen von den news? Wäre schön wenn so ist, da können wir ja auf eine grüne nächste Woche hoffen. Schönes WE allen die noch hier sind.

Sind das dann heute die Auswirkungen von den news? Wäre schön wenn so ist, da können wir ja auf eine grüne nächste Woche hoffen. Schönes WE allen die noch hier sind.  Gruss tz

Gruss tz

Antwort auf Beitrag Nr.: 44.094.283 von taenzerin am 01.02.13 18:45:28PSDV präseniert am 6 Februar nach Börsenschluss die Zahlen

Siehe Google Übersetzung

pSivida Corp (NASDAQ: PSDV) (ASX: PVA), ein führendes Unternehmen in der Entwicklung verzögerter Freisetzung, Drug-Delivery-Produkte für die Behandlung von Rücken-of-the-Augenkrankheiten, gab heute bekannt, dass seine Finanzergebnisse für das zweite Quartal des Geschäftsjahres 2013 wird nach dem Börsenschluss am Mittwoch, 6. Februar 2013, gefolgt am selben Tag von einem Konferenzgespräch und Live-Webcast für 04.30 ET geplant freigegeben werden.

Bin schon länger mit EP 1.31 $ an Board

Siehe Google Übersetzung

pSivida Corp (NASDAQ: PSDV) (ASX: PVA), ein führendes Unternehmen in der Entwicklung verzögerter Freisetzung, Drug-Delivery-Produkte für die Behandlung von Rücken-of-the-Augenkrankheiten, gab heute bekannt, dass seine Finanzergebnisse für das zweite Quartal des Geschäftsjahres 2013 wird nach dem Börsenschluss am Mittwoch, 6. Februar 2013, gefolgt am selben Tag von einem Konferenzgespräch und Live-Webcast für 04.30 ET geplant freigegeben werden.

Bin schon länger mit EP 1.31 $ an Board

Gestern Freitag Tageshöchst 2.58$

Mit etwas Geduld werden wir hier viel höhere Kurse sehen

Alimera has also reported that, based on a June 2012 meeting with the FDA, it intends to respond in the first quarter of 2013 to issues raised by the FDA in its Complete Response Letter using data from Alimera's two previously completed pivotal Phase III clinical trials, focusing on the population of patients with chronic DME, the same indication for which marketing approval for ILUVIEN has been granted in various EU countries. Approval in the U.S. would entitle pSivida to a $25 million milestone payment from Alimera and 20% of net profits, as defined, from U.S. sales of ILUVIEN by Alimera.

http://www.google.com/finance?q=NASDAQ%3APSDV&ei=2KUoUcCuL6S…

Mit etwas Geduld werden wir hier viel höhere Kurse sehen

Alimera has also reported that, based on a June 2012 meeting with the FDA, it intends to respond in the first quarter of 2013 to issues raised by the FDA in its Complete Response Letter using data from Alimera's two previously completed pivotal Phase III clinical trials, focusing on the population of patients with chronic DME, the same indication for which marketing approval for ILUVIEN has been granted in various EU countries. Approval in the U.S. would entitle pSivida to a $25 million milestone payment from Alimera and 20% of net profits, as defined, from U.S. sales of ILUVIEN by Alimera.

http://www.google.com/finance?q=NASDAQ%3APSDV&ei=2KUoUcCuL6S…

Die Institutionellen decken sich vor den wichtigen News wie z.b. der neue Antrag für die US-Zulassung und die bevorstehende Markteinführungen von Iluven in Europa die für dieses Quartal anstehen .

http://data.cnbc.com/quotes/PSDV/tab/8

Buyers 2/24/13 (5,125,140) $6.70 22.6% <<< INSTIS DECKEN SICH EIN

Sellers 2/24/13 (635,955) $1.63 2.3%

http://data.cnbc.com/quotes/PSDV/tab/8

Buyers 2/24/13 (5,125,140) $6.70 22.6% <<< INSTIS DECKEN SICH EIN

Sellers 2/24/13 (635,955) $1.63 2.3%

Antwort auf Beitrag Nr.: 44.179.545 von Biohero am 24.02.13 15:10:36pSivida Corp Announces New ILUVIEN(R) PDUFA Date of October 17 2013

http://www.marketwatch.com/story/psivida-corp-announces-new-…

http://www.marketwatch.com/story/psivida-corp-announces-new-…

Ich bleibe dabei Am 17 Okober ist der PDUFA FDA Termin

Der RunUp ist erst in der Anfangsphase mit etwas Geduld + Nerven sind 6,7,8 $ nicht unrealistisch od was meinst Du Biohero

od was meinst Du Biohero

http://www.biorunup.com/categories/FDA_Calendar

Am 17 Okober ist der PDUFA FDA TerminDer RunUp ist erst in der Anfangsphase mit etwas Geduld + Nerven sind 6,7,8 $ nicht unrealistisch

od was meinst Du Biohero

http://www.biorunup.com/categories/FDA_Calendar

was war heute?

Das ding geht ja wirklich unglaublich nach Norden...

Das ding geht ja wirklich unglaublich nach Norden...

Am Freitag so 10 minuten vor Börsenschluß ist ein sogenannter $heff der einige Anhänger hat eingestiegen und diejenigen die es nicht oder zu spät mitgekriegt haben sind gestern eingestiegen .

Jetzt ist Vorsicht angebracht denn es ist bekannt das er schnell gewinne mitnimmt und natürlich die meisten seiner lemminge ihm folgen beim Verkauf das kann die Aktie schnell mal 10-20% in die tiefe reissen erst recht bei so einem low floater .

Die Aktie hat gutes Potential aber jetzt sind auch die ganzen Zocker drin . Ich denke $4.50-5.50 bis vor der Entscheidung sollten drin sein ,wer das risiko eingehen will und die FDA Entscheidung mitmachen will könnte weitere $2-3 plus pro aktie machen falls positiv denn Psivida erhält $25 Million meeilenstein zahlung von Alimera für die Zulassung ABER umgekehrt also sollte die Zulassung nicht erfolgen dann gute nacht erst recht weil Cash nur noch für ca 3 weitere Quartale reicht .Es ist auch gut möglich das eine KE schon vor der Zulassung kommt also gewinne mitnehmen wäre nicht verkehrt .

“We are very pleased that the FDA has accepted Alimera Sciences’ recently resubmitted New Drug Application for ILUVIEN® for chronic Diabetic Macular Edema (DME) and has set a PDUFA target date of October 17, 2013. Approval in the U.S. would entitle pSivida to a $25 million milestone payment from Alimera and 20% of net profits, as defined, from U.S. sales of ILUVIEN by Alimera,” said Dr. Paul Ashton, President and CEO of pSivida.

Hier ist die seite von diesem $heff

http://investorshub.advfn.com/$heffs-$tation-of-$tocks-&-$ol…

Jetzt ist Vorsicht angebracht denn es ist bekannt das er schnell gewinne mitnimmt und natürlich die meisten seiner lemminge ihm folgen beim Verkauf das kann die Aktie schnell mal 10-20% in die tiefe reissen erst recht bei so einem low floater .

Die Aktie hat gutes Potential aber jetzt sind auch die ganzen Zocker drin . Ich denke $4.50-5.50 bis vor der Entscheidung sollten drin sein ,wer das risiko eingehen will und die FDA Entscheidung mitmachen will könnte weitere $2-3 plus pro aktie machen falls positiv denn Psivida erhält $25 Million meeilenstein zahlung von Alimera für die Zulassung ABER umgekehrt also sollte die Zulassung nicht erfolgen dann gute nacht erst recht weil Cash nur noch für ca 3 weitere Quartale reicht .Es ist auch gut möglich das eine KE schon vor der Zulassung kommt also gewinne mitnehmen wäre nicht verkehrt .

“We are very pleased that the FDA has accepted Alimera Sciences’ recently resubmitted New Drug Application for ILUVIEN® for chronic Diabetic Macular Edema (DME) and has set a PDUFA target date of October 17, 2013. Approval in the U.S. would entitle pSivida to a $25 million milestone payment from Alimera and 20% of net profits, as defined, from U.S. sales of ILUVIEN by Alimera,” said Dr. Paul Ashton, President and CEO of pSivida.

Hier ist die seite von diesem $heff

http://investorshub.advfn.com/$heffs-$tation-of-$tocks-&-$ol…

Die kleine KE ist durch

http://www.bizjournals.com/boston/blog/bioflash/2013/07/eye-…

Bis zum 17 Oktober müsste es Kursmässig jetzt wieder steigen (Biorunup)

http://www.google.com/finance?q=NASDAQ%3APSDV&ei=34_7UZCtC-a…

http://www.bizjournals.com/boston/blog/bioflash/2013/07/eye-…

Bis zum 17 Oktober müsste es Kursmässig jetzt wieder steigen (Biorunup)

http://www.google.com/finance?q=NASDAQ%3APSDV&ei=34_7UZCtC-a…

Antwort auf Beitrag Nr.: 45.169.217 von multimediaperle am 02.08.13 13:00:02http://www.bizjournals.com/boston/blog/bioflash/2013/07/eye-…

http://www.google.com/finance?q=NASDAQ%3APSDV&ei=lJv7UdjEJaq…

http://www.google.com/finance?q=NASDAQ%3APSDV&ei=lJv7UdjEJaq…

Antwort auf Beitrag Nr.: 44.868.777 von Biohero am 18.06.13 11:53:16Dieser $heff Guru hatte sich am 15 August wieder in PSDV eingekauft mit EP 3.33$

Bin selber noch immer mit meinem EP 1.31$ mit an Board

Hoffe auf einen Runup Aktie hat Nachhol Potential

Verkausziel ist 4.80$ u das vor dem FDA Entscheid

Bin selber noch immer mit meinem EP 1.31$ mit an Board

Hoffe auf einen Runup Aktie hat Nachhol Potential

Verkausziel ist 4.80$

u das vor dem FDA Entscheid

Bin heute wieder in PSDV eingestiegen ,das Unternehmen hat nun genug Cash und die Zulassung wird diesmal auch höchst wahrscheinlich erfolgen .

Trotzdem werde ich schnell verkaufen um die $4.50-5 .

Trotzdem werde ich schnell verkaufen um die $4.50-5 .

Volumen ist ordentlich für PSDV verhältnisse denke die $4 Marke wird bald fallen ..

Je näher wir dem Oktober kommen desto mehr zocker werden reinkommen deshalb ist der aktuelle kurs ein guter einstiegspunkt .

Je näher wir dem Oktober kommen desto mehr zocker werden reinkommen deshalb ist der aktuelle kurs ein guter einstiegspunkt .

Bei Zulassung erhält PSDV $25 M von ALIM das bedeutet Cashbestand würde direkt auf knapp $50 M verbessern bei einer Marktkap von nur $80 M ist und wäre die Aktie massivst Unterbewertet .

Es gibt 2 Million DME Patienten stellt sich ALIM etwas geschickt an dann hat Iluvien Blockbuster Potential . Sollte FDA iluvien zulassen dann hat PSDV das potential über die $10++ zu wandern .

Es gibt keinen besseren FDA Play für dieses Jahr mehr außer PSDV das könnte viele Zocker anlocken .

1m DME patients in US

1m DME patients in EU

Marktkap: $81 M

Cash: $24 M

Kurs: $3.50

Shares Out: 26.8 M ( 10.4 M shares held by Insiders & Institutions)

Präsentation (juli 2013)

http://files.shareholder.com/downloads/PSDV/2650105451x0x677…

Upon US approval of Iluvien, pSivida would be entitled to receive a $25 million milestone payment from Alimera and 20 percent of net profits, as defined, on sales of the drug by Alimera.

DME is a potentially blinding disease that affects over one million people in the United States. Currently there are no FDA approved drugs for the treatment of DME.The U.S. market for DME is $1.5 billion to $4 billion.

Es gibt 2 Million DME Patienten stellt sich ALIM etwas geschickt an dann hat Iluvien Blockbuster Potential . Sollte FDA iluvien zulassen dann hat PSDV das potential über die $10++ zu wandern .

Es gibt keinen besseren FDA Play für dieses Jahr mehr außer PSDV das könnte viele Zocker anlocken .

1m DME patients in US

1m DME patients in EU

Marktkap: $81 M

Cash: $24 M

Kurs: $3.50

Shares Out: 26.8 M ( 10.4 M shares held by Insiders & Institutions)

Präsentation (juli 2013)

http://files.shareholder.com/downloads/PSDV/2650105451x0x677…

Upon US approval of Iluvien, pSivida would be entitled to receive a $25 million milestone payment from Alimera and 20 percent of net profits, as defined, on sales of the drug by Alimera.

DME is a potentially blinding disease that affects over one million people in the United States. Currently there are no FDA approved drugs for the treatment of DME.The U.S. market for DME is $1.5 billion to $4 billion.

Ca 2 monat alter artikel aber trotzdem interessant ...

http://www.massdevice.com/news/psivida-gains-big-buyout-rumo…

pSivida stands to reap revenues of $315 million annually from sales of its Iluvien drug/device combination for treating diabetic macular edema.

"Therefore, based on the above projections, presuming that pSivida will get 315 million in revenue, the share price target of pSivida should be way north of $15.00," he wrote.

"The lack of ample eye care investment options is definitely a problem in biotech. There are simply not any options to invest in back of the eye disease devices. Therefore, making it a very valuable biotech, which deserves a high valuation based on this. pSidiva is a huge takeover target for big pharma who want to dominate the ocular market. Pfizer (NYSE:PFE) and Bausch & Lomb come to mind, as Pfizer owns over 10% of pSidiva already, and pSidiva is licensing Vitrasert and Durasert to Bausch & Lomb. It would be in both companies interest to buyout pSidiva to dominate the ocular market," according to the article.

http://www.massdevice.com/news/psivida-gains-big-buyout-rumo…

pSivida stands to reap revenues of $315 million annually from sales of its Iluvien drug/device combination for treating diabetic macular edema.

"Therefore, based on the above projections, presuming that pSivida will get 315 million in revenue, the share price target of pSivida should be way north of $15.00," he wrote.

"The lack of ample eye care investment options is definitely a problem in biotech. There are simply not any options to invest in back of the eye disease devices. Therefore, making it a very valuable biotech, which deserves a high valuation based on this. pSidiva is a huge takeover target for big pharma who want to dominate the ocular market. Pfizer (NYSE:PFE) and Bausch & Lomb come to mind, as Pfizer owns over 10% of pSidiva already, and pSidiva is licensing Vitrasert and Durasert to Bausch & Lomb. It would be in both companies interest to buyout pSidiva to dominate the ocular market," according to the article.

Jetzt sind die auch von TheStreet auf PSDV aufmerksam geworden ....

Alimera, pSivida Eye Drug Warrants FDA Approval On Third Try

BY David Sobek | 08/28/13 - 09:30 AM EDT

http://www.thestreet.com/story/12020867/1/alimera-psivida-ey…

Alimera, pSivida Eye Drug Warrants FDA Approval On Third Try

BY David Sobek | 08/28/13 - 09:30 AM EDT

http://www.thestreet.com/story/12020867/1/alimera-psivida-ey…

Chart Signale zeigen alle richtung norden ,52W hoch liegt bei rund $4.10 ich denke die wird sehr bald schon fallen .

Auf dem unteren Chartbild sieht man das PSDV seit fast ende Juni sich in einer Seitwärtsbewegung um die $3.50 befindet das bedeutet das wir vor einem signifikanten Sprung stehen ähnlich wie von Januar bis Juni .

Nur noch rund 40 Tage bis FDA -Entscheidung ...

http://www.stoxline.com/quote.php?symbol=psdv

http://www.barchart.com/quotes/stocks/PSDV

Auf dem unteren Chartbild sieht man das PSDV seit fast ende Juni sich in einer Seitwärtsbewegung um die $3.50 befindet das bedeutet das wir vor einem signifikanten Sprung stehen ähnlich wie von Januar bis Juni .

Nur noch rund 40 Tage bis FDA -Entscheidung ...

http://www.stoxline.com/quote.php?symbol=psdv

http://www.barchart.com/quotes/stocks/PSDV

Wenn wir glück haben knacken wir heute noch die $4...

Mal sehen was ob es was neues morgen auf der Rodman Präsentation gibt ..

PSDV..9/10 12:05pm EST..Rodman & Renshaw's Annual Global Investment Conference. http://bit.ly/17D9THZ

PSDV..9/10 12:05pm EST..Rodman & Renshaw's Annual Global Investment Conference. http://bit.ly/17D9THZ

Da scheint bei rund $3.80 ein kleiner widerstand zu sein aber sobald dieser gebrochen ist werden wir schnell ein neues 52W hoch sehen .

Sieht super aus heute aktuell $3.92 mal sehen ob die $4 Makre hute fällt ..

Die $4 ist gefallen jetzt hoffen wir das PSDV drüber schließt was sehr bullish wäre .

Antwort auf Beitrag Nr.: 45.440.537 von binda am 13.09.13 00:22:40Die 5 $ werden wird in spätestens zwei drei Wochen sehen

Akuell wird versucht noch möglich Günstig an die Aktien zu kommen

Hab gerade den Chart von CLSN angeschaut dort gab es den Finalen Schluss

Spurt auch erst ganz am Schluss

Also noch etwas Geduld haben u dann abkassieren kann plötzlich sehr schnell gehen an einem Tag 20% Plus Typisch Biorunup

Wünsche allen investierten viel Glück

Akuell wird versucht noch möglich Günstig an die Aktien zu kommen

Hab gerade den Chart von CLSN angeschaut dort gab es den Finalen Schluss

Spurt auch erst ganz am Schluss

Also noch etwas Geduld haben u dann abkassieren kann plötzlich sehr schnell gehen an einem Tag 20% Plus Typisch Biorunup

Wünsche allen investierten viel Glück

Morgen Mittwoch kommen noch die Zahlen

pSivida Corp. Announces Fourth Quarter and Fiscal Year 2013 Financial Results Release Date and Confe

Denke die werden keinen grossen Einfluss auf den Aktienkurs haben

Ev ein kleiner Absacker od es wird gleich voll durchgestaret

http://www.dailyfinance.com/2013/09/18/psivida-corp-announce…

Also ich mache mir keine Sorgen das wir bald die 5$ sehen

Läuft heute schon mal nicht schlecht aktuell 4.11$

pSivida Corp. Announces Fourth Quarter and Fiscal Year 2013 Financial Results Release Date and Confe

Denke die werden keinen grossen Einfluss auf den Aktienkurs haben

Ev ein kleiner Absacker od es wird gleich voll durchgestaret

http://www.dailyfinance.com/2013/09/18/psivida-corp-announce…

Also ich mache mir keine Sorgen das wir bald die 5$ sehen

Läuft heute schon mal nicht schlecht aktuell 4.11$

Bekanntgabe nach Börsenschluss

its financial results for the fourth quarter and fiscal year 2013 will be released after the market close on Wednesday, September 25, 2013

Bin mal gespannt.

its financial results for the fourth quarter and fiscal year 2013 will be released after the market close on Wednesday, September 25, 2013

Bin mal gespannt.

Glaube nicht, dass im Bericht viel Neues stehen wird. Evtl. gibt es weitere positive Ergebnisse in den anderen Forschungsbereichen, neben dem Flagschiff Iluvien

Geld werden sie bis jetzt noch nicht wirklich verdient haben. Auf der anderen Seite schluckt die Forschung ne Menge.

Erst die FDA Zulassung und die dadurch ausgelöste Meilensteinzahlung durch Alimera an Psivida, wird den Kurs beflügeln.

Bis jetzt verrät der Kurs noch nichts

Geld werden sie bis jetzt noch nicht wirklich verdient haben. Auf der anderen Seite schluckt die Forschung ne Menge.

Erst die FDA Zulassung und die dadurch ausgelöste Meilensteinzahlung durch Alimera an Psivida, wird den Kurs beflügeln.

Bis jetzt verrät der Kurs noch nichts

Naja wie befürchtet sehr schwache Zahlen

Ev kann man morgen nochmals günstig rein...nächste Woche ist der Spuck wieder vergessen u es kann endlich auf die 5$ losgehen

http://www.fortmilltimes.com/2013/09/25/2982784/psivida-corp…

http://www.google.com/finance?q=NASDAQ%3APSDV&ei=qElDUqhGh4_…

Ev kann man morgen nochmals günstig rein...nächste Woche ist der Spuck wieder vergessen u es kann endlich auf die 5$ losgehen

http://www.fortmilltimes.com/2013/09/25/2982784/psivida-corp…

http://www.google.com/finance?q=NASDAQ%3APSDV&ei=qElDUqhGh4_…

hab den kurs rücksetzer genutzt um weitere 4k teile zukaufen . Hoffe diese noch vor der FDA Entscheidung mit nettem profit zuverkaufen .

Antwort auf Beitrag Nr.: 45.517.747 von multimediaperle am 25.09.13 22:51:07Sehe PSDV hatte sich nach den Zahlen ganz gut gehalten

Dem weiteren Runup steht nix mehr im Weg der Oktober wird spannend

Dem weiteren Runup steht nix mehr im Weg der Oktober wird spannend

pSivida to Present at 4th Annual Conference on Biosimilars & Biobetters

Psivida (NASDAQ:PSDV)

Intraday Stock Chart

Today : Freitag 27 September 2013

pSivida Corp. (NASDAQ:PSDV), a specialty pharmaceutical company that is a leader in developing sustained release drugs for treatment of back-of-the-eye diseases, will present at the 4th Annual Biosimilars & Biobetters Conference being held October 1 and 2 in London.

Dr. Paul Ashton, president and CEO of pSivida, will discuss “A Simple Route to Biobetters” providing delegates insight into sustained delivery of biologics. Additional case study presentations include speakers from pharmaceutical companies such as Novartis, Pfizer, Eli Lilly & Company, Roche and Merck Millipore, among others.

pSivida is developing Tethadur™, a sustained-release delivery system of nanostructured porous silicon that has the potential to deliver proteins, peptides and antibodies on a pre-determined controlled basis. The conference is expected to touch on catalysts, such as patent expirations, which are propelling increased interest in and development of biological therapeutic programs by the pharmaceutical industry. More information on the conference is available at the conference website: http://www.biosimilars-biobetters.co.uk.

http://de.advfn.com/p.php?pid=nmona&article=59391992

Psivida (NASDAQ:PSDV)

Intraday Stock Chart

Today : Freitag 27 September 2013

pSivida Corp. (NASDAQ:PSDV), a specialty pharmaceutical company that is a leader in developing sustained release drugs for treatment of back-of-the-eye diseases, will present at the 4th Annual Biosimilars & Biobetters Conference being held October 1 and 2 in London.

Dr. Paul Ashton, president and CEO of pSivida, will discuss “A Simple Route to Biobetters” providing delegates insight into sustained delivery of biologics. Additional case study presentations include speakers from pharmaceutical companies such as Novartis, Pfizer, Eli Lilly & Company, Roche and Merck Millipore, among others.

pSivida is developing Tethadur™, a sustained-release delivery system of nanostructured porous silicon that has the potential to deliver proteins, peptides and antibodies on a pre-determined controlled basis. The conference is expected to touch on catalysts, such as patent expirations, which are propelling increased interest in and development of biological therapeutic programs by the pharmaceutical industry. More information on the conference is available at the conference website: http://www.biosimilars-biobetters.co.uk.

http://de.advfn.com/p.php?pid=nmona&article=59391992

Durasert das mit Pfizer entwickelt wird nähert sich dem Abschluß der Phase 1/2 Studie laut Clinicaltrials.gov (s.link) das heißt Pfizer hat nach den Ergebissen 90 tage zeit zu entscheiden ob sie die weltweite Rechte an Durasert übernehmen wollen oder nicht .Wenn ja gibts direkt eine $20 M zahlung und weitere meilenstein zahlungen siehe unten .

Das Durasert implantat enthält den wirkstoff latanoprost(xalantan) ein aktueller Blockbuster und Gold Standard bei Glaukoma das von Pfizer vermarktet wird .PSDV´s durasert implantat ist langwirkend im gegensatz zu Pfizer´s einmal täglich Augentropfen .Da es sich um den selben Wirkstoff handelt dürfte das Studienergebnis höchstwahrscheinlich positiv ausfallen .

http://clinicaltrials.gov/ct2/show/record/NCT01180062

Slow release Latanoprost (Xalatan) in a research and license agreement with Pfizer

pSivida has received regulatory approvals for 3 inserts to treat back-of-the-eye diseases. A sustained-release bioerodible micro-insert designed to slowly deliver latanoprost is its attempt to treat glaucoma, a front-of-the-eye disease. Adherence to treatment is a huge problem among glaucoma subjects and a slow release insert has the potential to solve these compliance issues. This insert is being developed as part of a collaborative research and license agreement between the company and Pfizer (PFE). A phase 2 investigator sponsored proof of concept (POC) study (ClinicalTrials.gov Identifier:NCT01180062) is currently ongoing. Pfizer has the option to exercise an exclusive worldwide license to develop and commercialize the slow release latanoprost within 90 days of receiving the POC final study report in exchange for a $20 million payment, double-digit sales-based royalties and additional development, regulatory and sales performance milestone payments of up to $146.5 million. Note that the primary completion date for this POC study on the clinicaltrials.gov site is listed as September 2013. This is a catalyst that is not on many traders' radars. Given pSivida's experience in developing slow release inserts, there is good reason to have confidence in this slow release biodegradable device for the treatment of glaucoma.

Das Durasert implantat enthält den wirkstoff latanoprost(xalantan) ein aktueller Blockbuster und Gold Standard bei Glaukoma das von Pfizer vermarktet wird .PSDV´s durasert implantat ist langwirkend im gegensatz zu Pfizer´s einmal täglich Augentropfen .Da es sich um den selben Wirkstoff handelt dürfte das Studienergebnis höchstwahrscheinlich positiv ausfallen .

http://clinicaltrials.gov/ct2/show/record/NCT01180062

Slow release Latanoprost (Xalatan) in a research and license agreement with Pfizer

pSivida has received regulatory approvals for 3 inserts to treat back-of-the-eye diseases. A sustained-release bioerodible micro-insert designed to slowly deliver latanoprost is its attempt to treat glaucoma, a front-of-the-eye disease. Adherence to treatment is a huge problem among glaucoma subjects and a slow release insert has the potential to solve these compliance issues. This insert is being developed as part of a collaborative research and license agreement between the company and Pfizer (PFE). A phase 2 investigator sponsored proof of concept (POC) study (ClinicalTrials.gov Identifier:NCT01180062) is currently ongoing. Pfizer has the option to exercise an exclusive worldwide license to develop and commercialize the slow release latanoprost within 90 days of receiving the POC final study report in exchange for a $20 million payment, double-digit sales-based royalties and additional development, regulatory and sales performance milestone payments of up to $146.5 million. Note that the primary completion date for this POC study on the clinicaltrials.gov site is listed as September 2013. This is a catalyst that is not on many traders' radars. Given pSivida's experience in developing slow release inserts, there is good reason to have confidence in this slow release biodegradable device for the treatment of glaucoma.

Psivida´s BrachySil das gegen Pankreaskrebs eingesetzt wird hat die Phase 2 Studie erfolgreich abgeschlossen und beginnt die letzte Globale Studie im 1Q 2014 .

Psivida hat die BrachySil Rechte an Enigma Therapeutics weitergegeben und Enigma selbst wurde vor kurzem von OncoSil aufgekauft .

Wenn BrachySil (heißt jetzt OncoSil) es auf dem Markt schafft dann erhält Psivida 8% royalties und bekommt 20% von den zahlungen bei einer möglichen Auslizenzierung . OncoSil könnte laut eignen angaben schon ende 2015 anfang 2016 auf dem Markt kommen wenn natürlich alles gut geht .

OncoSil Medical's medical device offers hope for pancreatic cancer patients

Wednesday, September 11, 2013 by Proactive Investors

http://www.proactiveinvestors.com.au/companies/news/47809/on…

- OncoSil Medical Limited is a Medical Device company that recently acquired OncoSil™, a medical device technology that is ready for global registration studies.

- OncoSil™ is a localised radiation potential therapy treatment for pancreatic cancer that would meet a major unmet clinical need.

- Pancreatic cancer remains a huge challenge for physicians. The annual global incidence of pancreatic cancer affects more than 280,000 people who have a median 5 year survival rate of less than 5% utilising current drug regimes.

- OncoSil™ has successfully completed Phase II studies for pancreatic cancer, and aims to capture a significant part of the global market for pancreatic drugs that are expected to exceed $1.2 billion by 2015.

- OncoSil™ is a Class III medical device, not a drug thereby requiring significantly less funding and time required undertaking a registration study.

- The capital investment to develop and globally register OncoSil™ as a medical device is a tiny fraction of the cost of developing an effective drug that achieves the same outcome. This provides a much higher return for investors.

- Market studies have indicated the potential for commercialised revenues for OncoSil™ treatment are from US$432 million to $705 million.

- There are share price catalysts for OncoSil Medical which has established an approximate 30 month timeline to undertake a global registration study, and commence formal applications for the right to sell OncoSil™ in major global markets. Each milestone and timeline achieved will further de-risk the company and place it more firmly on the radar of potential acquirers.

Catalysts and Milestones – Valuation inflection points next 6-12 months

- Q3-Q4 2013 – Commence application for Conformité Européenne marking with European Medicines Agency. This is a mandatory conformity marking for products that are sold in the European Economic Area that includes 27 member states and Iceland, Norway and Liechtenstein.

- Q4 2013 – Commence Pre-Investigational Device Exemption “IDE” application with U.S. Food and Drug Administration.

- Q4 2013 – Commence Australian application with Therapeutic Goods Administration for Register of Therapeutic Goods, and with Pharmaceutical Benefits Scheme.

- Q1 2014 – Global Registration Study.

-----

Enigma Therapeutics

Under a December 2012 license agreement, amended and restated in March 2013, Enigma Therapeutics Limited (Enigma) acquired an exclusive, worldwide, royalty-bearing license for the development of BrachySil, a BioSilicon product candidate for the treatment of pancreatic and other types of cancer. We received an upfront fee of $100,000, included in collaborative research and development revenue in fiscal 2013, and are entitled to an 8% sales-based royalty, 20% of sublicense consideration and milestones based on aggregate product sales. Enigma is obligated to pay an annual license maintenance fee of $100,000, creditable during each ensuing twelve month period against reimbursable patent maintenance costs and sales-based royalties.

Psivida hat die BrachySil Rechte an Enigma Therapeutics weitergegeben und Enigma selbst wurde vor kurzem von OncoSil aufgekauft .

Wenn BrachySil (heißt jetzt OncoSil) es auf dem Markt schafft dann erhält Psivida 8% royalties und bekommt 20% von den zahlungen bei einer möglichen Auslizenzierung . OncoSil könnte laut eignen angaben schon ende 2015 anfang 2016 auf dem Markt kommen wenn natürlich alles gut geht .

OncoSil Medical's medical device offers hope for pancreatic cancer patients

Wednesday, September 11, 2013 by Proactive Investors

http://www.proactiveinvestors.com.au/companies/news/47809/on…

- OncoSil Medical Limited is a Medical Device company that recently acquired OncoSil™, a medical device technology that is ready for global registration studies.

- OncoSil™ is a localised radiation potential therapy treatment for pancreatic cancer that would meet a major unmet clinical need.

- Pancreatic cancer remains a huge challenge for physicians. The annual global incidence of pancreatic cancer affects more than 280,000 people who have a median 5 year survival rate of less than 5% utilising current drug regimes.

- OncoSil™ has successfully completed Phase II studies for pancreatic cancer, and aims to capture a significant part of the global market for pancreatic drugs that are expected to exceed $1.2 billion by 2015.

- OncoSil™ is a Class III medical device, not a drug thereby requiring significantly less funding and time required undertaking a registration study.

- The capital investment to develop and globally register OncoSil™ as a medical device is a tiny fraction of the cost of developing an effective drug that achieves the same outcome. This provides a much higher return for investors.

- Market studies have indicated the potential for commercialised revenues for OncoSil™ treatment are from US$432 million to $705 million.

- There are share price catalysts for OncoSil Medical which has established an approximate 30 month timeline to undertake a global registration study, and commence formal applications for the right to sell OncoSil™ in major global markets. Each milestone and timeline achieved will further de-risk the company and place it more firmly on the radar of potential acquirers.

Catalysts and Milestones – Valuation inflection points next 6-12 months

- Q3-Q4 2013 – Commence application for Conformité Européenne marking with European Medicines Agency. This is a mandatory conformity marking for products that are sold in the European Economic Area that includes 27 member states and Iceland, Norway and Liechtenstein.

- Q4 2013 – Commence Pre-Investigational Device Exemption “IDE” application with U.S. Food and Drug Administration.

- Q4 2013 – Commence Australian application with Therapeutic Goods Administration for Register of Therapeutic Goods, and with Pharmaceutical Benefits Scheme.

- Q1 2014 – Global Registration Study.

-----

Enigma Therapeutics

Under a December 2012 license agreement, amended and restated in March 2013, Enigma Therapeutics Limited (Enigma) acquired an exclusive, worldwide, royalty-bearing license for the development of BrachySil, a BioSilicon product candidate for the treatment of pancreatic and other types of cancer. We received an upfront fee of $100,000, included in collaborative research and development revenue in fiscal 2013, and are entitled to an 8% sales-based royalty, 20% of sublicense consideration and milestones based on aggregate product sales. Enigma is obligated to pay an annual license maintenance fee of $100,000, creditable during each ensuing twelve month period against reimbursable patent maintenance costs and sales-based royalties.

Antwort auf Beitrag Nr.: 45.544.451 von binda am 01.10.13 08:55:56Diese News ist fantastisch für Psivida denn Iluvien steht jetzt den Patienten kostenlos zur verfügung da es jetzt von steuerfinanzierten Gesundheitsdienst bezahlt wird statt privat aus eigner tasche .

Auch in Deutschland wird gerade geprüft ob die kosten von der Krankenkasse übernommen werden und auch hier dürften wir bald was davon hören .

--

Die National Institute for Clinical Excellence (NICE) prüft nicht nur die Wirksamkeit neuer Medikamente, sondern auch deren Wirtschaftlichkeit.Der Grenzwert liegt derzeit bei 30.000 Pfund. Mehr darf eine medikamentöse Therapie nicht kosten, damit sie Patienten im steuerfinanzierten Gesundheitsdienst (NHS) kostenlos zur Verfügung gestellt wird.

Auch in Deutschland wird gerade geprüft ob die kosten von der Krankenkasse übernommen werden und auch hier dürften wir bald was davon hören .

--

Die National Institute for Clinical Excellence (NICE) prüft nicht nur die Wirksamkeit neuer Medikamente, sondern auch deren Wirtschaftlichkeit.Der Grenzwert liegt derzeit bei 30.000 Pfund. Mehr darf eine medikamentöse Therapie nicht kosten, damit sie Patienten im steuerfinanzierten Gesundheitsdienst (NHS) kostenlos zur Verfügung gestellt wird.

PSDV läuft wie am Schnürchen

Super News und ein Ja der FDA ist eigentlich nur noch Formsache

Mit solch guten Aussichten ist PSDV immer noch viel zu billig

Aktuell 4.49$

Super News und ein Ja der FDA ist eigentlich nur noch Formsache

Mit solch guten Aussichten ist PSDV immer noch viel zu billig

Aktuell 4.49$

4,85$ = 3,55€

4,85$ = 3,55€

Was glaubt ihr, wie viel Luft nach oben haben wir noch?

wow, 4,97$

3,68 Euro

in Fra und auf Tradegate bekommt man sie für 3,50

ups, und schon über 5

komme gar nicht so schnell mit

3,68 Euro

in Fra und auf Tradegate bekommt man sie für 3,50

ups, und schon über 5

komme gar nicht so schnell mit

Antwort auf Beitrag Nr.: 45.550.201 von multimediaperle am 01.10.13 19:37:54Richtig gewinne mitnehmen schadet nie hab auch ein teil verkauft und gleich in eine neue Bio perle gesteckt ..

SK 5,40$ = 3,995

nachbörslich sogar höher

nachbörslich sogar höher

Auch in Australien, obwohl dort kaum noch gehandelt wird, stieg der Kurs heute Morgen auf 5,62 A$

USA vorbörslich schon Musik drin...

Tja, die 5 scheinen zu halten. Die Nachricht ist super gut für Psivida.

Das Schöne ist, dass in USA keine Gaps entstanden sind. Der Kurs war ganz geschmeidig, peu a peu bis zum TH gestiegen.

Das Schöne ist, dass in USA keine Gaps entstanden sind. Der Kurs war ganz geschmeidig, peu a peu bis zum TH gestiegen.

October 28, 2013

Dear Fellow Stockholders,

It is our pleasure to invite you to this year’s Annual Meeting, which will be held on December 18, 2013 at 10:00 a.m. (US EST), at the Waltham Westin Hotel, Alcott Room, 70 Third Avenue, Waltham, Massachusetts 02451.

The proxy statement accompanying this letter describes the business that we will consider at the meeting and provides voting instructions. Your vote is important.

We hope that you are able to attend this year’s Annual Meeting.

Yours sincerely,

Dear Fellow Stockholders,

It is our pleasure to invite you to this year’s Annual Meeting, which will be held on December 18, 2013 at 10:00 a.m. (US EST), at the Waltham Westin Hotel, Alcott Room, 70 Third Avenue, Waltham, Massachusetts 02451.

The proxy statement accompanying this letter describes the business that we will consider at the meeting and provides voting instructions. Your vote is important.

We hope that you are able to attend this year’s Annual Meeting.

Yours sincerely,

Antwort auf Beitrag Nr.: 45.549.545 von binda am 01.10.13 18:06:39dieser Long Chart ist kein long Chart sonst würde man sehen dass die schon mal bei 40 $ stand.

Antwort auf Beitrag Nr.: 45.565.871 von binda am 04.10.13 09:08:42den kannst du dir selber suchen, der ist nicht mehr zu finden, aber es gab eine Zeit vor 2008, oder glaubst du die Bude gibt es erst seit 5 Jahren? Dass die mit ihren laufenden Kursaussetzungen, Splits, Resplits, ändern der WKN und aufteilen der Aktien was zu verschleiern haben sagt einiges über das Management aus.

Zitat von wohinistmeinGeld: den kannst du dir selber suchen, der ist nicht mehr zu finden, aber es gab eine Zeit vor 2008, oder glaubst du die Bude gibt es erst seit 5 Jahren? Dass die mit ihren laufenden Kursaussetzungen, Splits, Resplits, ändern der WKN und aufteilen der Aktien was zu verschleiern haben sagt einiges über das Management aus.

ganz ruhig Brauner, Du scheinst ja einer von der ganz "netten" Sorte zu sein

Den 5 Jahreschart hatte ich , als Antwort auf die Frage von Ghoststock

"Was glaubt ihr, wie viel Luft nach oben haben wir noch?"

reingestellt. Dort kann man sehen, wie der Kurs damals, vor der FDA-Entscheidung stieg. Warum hätte ich einen noch längeren einstellen sollen?

den kannst du dir selber suchen - mach ich

es gab eine Zeit vor 2008, oder glaubst du die Bude gibt es erst seit 5 Jahren? - Ach

Der Pullback war sehr gut für PSDV weil massivst überkauft gewesen , der boden könnte schon da sein oder zumindest nah dran sein .

Ich schau es mir heute an und entscheide ob ich reingehe aufjedenfall ist die Aktie nach wie vor heiß vor allem wegen der bevorstehenden FDA Entscheidung .

Ich schau es mir heute an und entscheide ob ich reingehe aufjedenfall ist die Aktie nach wie vor heiß vor allem wegen der bevorstehenden FDA Entscheidung .

Antwort auf Beitrag Nr.: 45.566.619 von wohinistmeinGeld am 04.10.13 10:38:50Was hat der Chart mit dem Management zu tun ? Und es gibt nichts zu verschleiern das Unternehmen hatte schon immer zwei verschiedene WKN´s einmal für die unter der ASX laufende aktien und dann für die Nasdaq wobei ich von der ASX gelistete aktien abrate .

ob die 5 zurück erobert werden?

Antwort auf Beitrag Nr.: 45.568.833 von Biohero am 04.10.13 15:02:45schon immer? Was heißt bei dir immer, ich habe die Aufteilung erlebt, das war aber noch zu Zeiten die lange vor diesem "Langzeit Chart" lagen. Das ist $ Kurs, auch der EUR Kurs war mal über 40, aber echte Langzeit Charts gibt's schwer zu finden.

Das mit dem Shutdown und Schuldenobergrenze in USA macht mir sorgen deshalb werde ich vorerst bis zum 17. Oktober abwarten .

pSivida Corporation: Strong Takeover Target, October 17th PDUFA Date Make It A Buy

http://seekingalpha.com/article/1731522-psivida-corporation-…

pSivida Corporation: Strong Takeover Target, October 17th PDUFA Date Make It A Buy

http://seekingalpha.com/article/1731522-psivida-corporation-…

Investment Scenarios: The Positive and Negative Case

pSivida (PSDV) has a very important binary event upcoming on October 17, 2013; this is the PDUFA date for Iluvien, an ocular implant for diabetic macular edema that was licensed to Alimera (ALIM). I cannot answer the question of whether the government shutdown might delay the PDUFA date and if so, how long.

Approval would trigger a $25 million milestone payment to pSivida and potentially could expedite the approval of Medidur as early as 2016. Medidur is an ocular implant that uses the same insert device as Iluvien and the same dose of the same drug. Iluvien is indicated for diabetic macular edema (DME) and Medidur, if approved, would be indicated for the different indication of posterior uveitis; commercial potential may be comparable for these indications. Iluvien's approval could allow pSivida to file an NDA on the basis of a single phase III trial that is now underway. The company has profit sharing rights that provide it roughly 20% of Iluvien's operating profits in the US; this is based on sales minus cost of goods sold and direct selling expenses.

The $25 million milestone payment would put the company in a comfortable cash position with about $41 million on its balance sheet as of year-end 2013. This would be enough to take the company through the possible approval of Medidur in 2016 and might put pSivida in the position of being able to market Medidur in the US entirely on its own. This would dramatically change the business model from a licensing business to a much more attractive specialty pharmaceutical model.

This would also allow pSivida to adequately fund new ocular drug delivery products based on Tethadur. The company's current ocular implants do not degrade once they are implanted in the eye and can only deliver small molecule drugs. Tethadur is based on a new biodegradable technology that can potentially deliver biologics such as Lucentis or Eylea to the back of the eye. If successful, this would be a major technology and commercial advance. Tethadur is in pre-clinical testing and is currently being evaluated for an undisclosed product under a funded evaluation agreement with a leading global biopharmaceutical company.

If Iluvien is approved on October 17th, investors will focus on the potential approval of Medidur in 2016 and the evolution to a specialty pharmaceutical model. I expect a very slow sales ramp for Iluvien in the US, but with time it probably has sales potential of $100 to $200 million of sales, perhaps by 2019. This could result in $15 to $30 million of revenues for pSivida with no offsetting costs. Iluvien has already been approved in Europe and has similar sales prospects in the same timeframe in Europe. Topping off this very positive investment scenario is the significant promise of a new technology, Tethadur.

So far, I have laid out the positive case for pSivida. If this comes to be, I could see a significant move in the stock. Its current fully diluted share count is 31.3 shares if every outstanding option and warrant is included; by GAAP accounting the fully diluted share count is about 27.0 million. Based on 31.3 million shares and the recent price of $4.50, the current market capitalization is $140 million. If the positive case prevails, I think that it could drive market capitalization to $280 to $350 million or $9 to $11 based on valuations of similar companies.

This potential 100% to 150% upside must be weighed against what would likely be s sharp downside move of 40% to 50% in the negative case. There would be no $25 million milestone payment, Medidur would require another phase III trial pushing approval to 2018 and no payments based on Iluvien's US sales could be expected. While there would still be promise for pSivida based on Medidur, Tethadur and European sales of Iluvien, the investment potential would be meaningfully diminished.

So what are the odds of an approval for Iluvien, which has previously received two complete response letters from the FDA? In the last CRL, the FDA asked Alimera to conduct two new phase III trials which would be extremely expensive and could take three to four years to complete. Alimera believed that the information that the FDA needed to approve Iluvien could be provided from the data already compiled for the previous NDA filings. Alimera hired a consulting company to reorganize the NDA paying them $4 million and potentially another $2 million upon approval. Encouragingly, the FDA accepted the refiling and set the October 17th PDUFA date. This along with the previous approval of Iluvien in seven European countries suggests that there is a reasonable chance for approval.

I place the upside as potentially $9 to $13 with Iluvien's approval and $2.25 to $2.50 if it is not approved. I place the odds for approval as better than 60%. The approval by European regulatory agencies indicates to me that there is a persuasive case for approval based on the data in the NDA. I am inclined to think that the format of the initial NDA filing was flawed and with a better presentation of the underlying data that the US may follow Europe in approving Iluvien. I want to caution investors that these are guesses on my part meant to convey magnitude of the potential upside and downside. They convey more precision than is actually the case. Based on this reasoning, I think that the potential upside in the case of approval substantially offsets the downside if Iluvien is rejected.

More Detailed Analysis of pSivida and Alimera

I wrote a more detailed analysis of pSivida and Alimera on May 31, 2013. I would suggest that investors interested in pSivida carefully read that report. This note is only a brief summary and update of that earlier, more in-depth report.

The European Launch of Iluvien Has Been Slow and Disappointing So Far

pSivida receives 20% of net profits of Iluvien in Europe using the same determination previously described for the US; sales minus cost of goods sold minus direct sales expenses on a country by country basis. Iluvien has been approved in seven European countries and has been going through the slow and rigorous process of gaining satisfactory reimbursement in the three major markets: Germany, the UK and France. Work continues on pricing and reimbursement in Italy, Spain, Portugal and Austria. However, Alimera does not currently plan to commercialize Iluvien in those countries until it achieves positive cash flow in Germany, the United Kingdom and France.

Germany is most advanced in terms of commercialization, but progress has been slow. In Germany, reimbursement requires individual negotiations with over 20 health insurers and associations and reimbursement is gained one at a time. Without such approvals, patients must file individual requests to be reimbursed. This is a tedious, slow process. Alimera reported that nearly 90 individual funding requests have been made and of these less than one third of patients have been treated. This has obviously slowed the commercial launch in Germany.

The launch in the UK has been greatly affected by determination of the National Institute for Health and Care Excellence, or NICE, not to recommend Iluvien for DME. However, NICE's Appraisal Committee has since recommended Iluvien for the treatment of pseudophakic patients with chronic DME considered insufficiently responsive to available therapies. Alimera hopes that this will lead to pricing approval in this indication in 4Q, 2013. The Transparency Commission of the French National Health Authority issued a favorable opinion for the reimbursement and hospital listing of Iluvien by the French National Health Insurance. The commercial launch could begin in early 2014.

Iluvien was initially rejected by NICE in the UK as being not cost effective for use in diabetic macular edema, which meant that it would not be reimbursed by the National Health Service, which is responsible for reimbursement for 90% of UK patients. This meant that only private pay patients could be addressed. However, NICE has recently found Iluvien to be cost effective for pseudophakic patients and this opens up a not insignificant opportunity.

Alimera began realizing Iluvien revenues in the second quarter of 2013 from operations in Germany and the UK as 18 units (90% in Germany) were implanted leading to revenues of $179,000. As of the quarterly conference call on August 12th 2013, Iluvien had been used by 14 physicians in the U.K. and Germany to treat a total of 30 patients with chronic diabetic macular edema. Initially patients are treated in one eye, but the company reports that good outcomes have led to some patients being treated in the second eye.

The European uptake has been slower than management expected primarily because of these reimbursement hurdles. Looking ahead, they cautioned that demand could flatten in the 3Q and early 4Q as physicians assess the first patients treated before some upward inflection occurs in late 2013. By that time they hope that most of the reimbursement issues will be behind them. It seems to me that sales will probably be about $1 million in 2013. I would expect some significant improvement in 2014, but I can't give anything more than an outright guess of perhaps $5 to $10 million. I do believe that Iluvien has an important role to play in DME patients who have failed both VEGF and laser therapy and also in pseudophakic patients.

http://seekingalpha.com/article/1733322-psivida-previewing-t…

pSivida (PSDV) has a very important binary event upcoming on October 17, 2013; this is the PDUFA date for Iluvien, an ocular implant for diabetic macular edema that was licensed to Alimera (ALIM). I cannot answer the question of whether the government shutdown might delay the PDUFA date and if so, how long.

Approval would trigger a $25 million milestone payment to pSivida and potentially could expedite the approval of Medidur as early as 2016. Medidur is an ocular implant that uses the same insert device as Iluvien and the same dose of the same drug. Iluvien is indicated for diabetic macular edema (DME) and Medidur, if approved, would be indicated for the different indication of posterior uveitis; commercial potential may be comparable for these indications. Iluvien's approval could allow pSivida to file an NDA on the basis of a single phase III trial that is now underway. The company has profit sharing rights that provide it roughly 20% of Iluvien's operating profits in the US; this is based on sales minus cost of goods sold and direct selling expenses.

The $25 million milestone payment would put the company in a comfortable cash position with about $41 million on its balance sheet as of year-end 2013. This would be enough to take the company through the possible approval of Medidur in 2016 and might put pSivida in the position of being able to market Medidur in the US entirely on its own. This would dramatically change the business model from a licensing business to a much more attractive specialty pharmaceutical model.

This would also allow pSivida to adequately fund new ocular drug delivery products based on Tethadur. The company's current ocular implants do not degrade once they are implanted in the eye and can only deliver small molecule drugs. Tethadur is based on a new biodegradable technology that can potentially deliver biologics such as Lucentis or Eylea to the back of the eye. If successful, this would be a major technology and commercial advance. Tethadur is in pre-clinical testing and is currently being evaluated for an undisclosed product under a funded evaluation agreement with a leading global biopharmaceutical company.

If Iluvien is approved on October 17th, investors will focus on the potential approval of Medidur in 2016 and the evolution to a specialty pharmaceutical model. I expect a very slow sales ramp for Iluvien in the US, but with time it probably has sales potential of $100 to $200 million of sales, perhaps by 2019. This could result in $15 to $30 million of revenues for pSivida with no offsetting costs. Iluvien has already been approved in Europe and has similar sales prospects in the same timeframe in Europe. Topping off this very positive investment scenario is the significant promise of a new technology, Tethadur.

So far, I have laid out the positive case for pSivida. If this comes to be, I could see a significant move in the stock. Its current fully diluted share count is 31.3 shares if every outstanding option and warrant is included; by GAAP accounting the fully diluted share count is about 27.0 million. Based on 31.3 million shares and the recent price of $4.50, the current market capitalization is $140 million. If the positive case prevails, I think that it could drive market capitalization to $280 to $350 million or $9 to $11 based on valuations of similar companies.

This potential 100% to 150% upside must be weighed against what would likely be s sharp downside move of 40% to 50% in the negative case. There would be no $25 million milestone payment, Medidur would require another phase III trial pushing approval to 2018 and no payments based on Iluvien's US sales could be expected. While there would still be promise for pSivida based on Medidur, Tethadur and European sales of Iluvien, the investment potential would be meaningfully diminished.

So what are the odds of an approval for Iluvien, which has previously received two complete response letters from the FDA? In the last CRL, the FDA asked Alimera to conduct two new phase III trials which would be extremely expensive and could take three to four years to complete. Alimera believed that the information that the FDA needed to approve Iluvien could be provided from the data already compiled for the previous NDA filings. Alimera hired a consulting company to reorganize the NDA paying them $4 million and potentially another $2 million upon approval. Encouragingly, the FDA accepted the refiling and set the October 17th PDUFA date. This along with the previous approval of Iluvien in seven European countries suggests that there is a reasonable chance for approval.

I place the upside as potentially $9 to $13 with Iluvien's approval and $2.25 to $2.50 if it is not approved. I place the odds for approval as better than 60%. The approval by European regulatory agencies indicates to me that there is a persuasive case for approval based on the data in the NDA. I am inclined to think that the format of the initial NDA filing was flawed and with a better presentation of the underlying data that the US may follow Europe in approving Iluvien. I want to caution investors that these are guesses on my part meant to convey magnitude of the potential upside and downside. They convey more precision than is actually the case. Based on this reasoning, I think that the potential upside in the case of approval substantially offsets the downside if Iluvien is rejected.

More Detailed Analysis of pSivida and Alimera

I wrote a more detailed analysis of pSivida and Alimera on May 31, 2013. I would suggest that investors interested in pSivida carefully read that report. This note is only a brief summary and update of that earlier, more in-depth report.

The European Launch of Iluvien Has Been Slow and Disappointing So Far

pSivida receives 20% of net profits of Iluvien in Europe using the same determination previously described for the US; sales minus cost of goods sold minus direct sales expenses on a country by country basis. Iluvien has been approved in seven European countries and has been going through the slow and rigorous process of gaining satisfactory reimbursement in the three major markets: Germany, the UK and France. Work continues on pricing and reimbursement in Italy, Spain, Portugal and Austria. However, Alimera does not currently plan to commercialize Iluvien in those countries until it achieves positive cash flow in Germany, the United Kingdom and France.

Germany is most advanced in terms of commercialization, but progress has been slow. In Germany, reimbursement requires individual negotiations with over 20 health insurers and associations and reimbursement is gained one at a time. Without such approvals, patients must file individual requests to be reimbursed. This is a tedious, slow process. Alimera reported that nearly 90 individual funding requests have been made and of these less than one third of patients have been treated. This has obviously slowed the commercial launch in Germany.

The launch in the UK has been greatly affected by determination of the National Institute for Health and Care Excellence, or NICE, not to recommend Iluvien for DME. However, NICE's Appraisal Committee has since recommended Iluvien for the treatment of pseudophakic patients with chronic DME considered insufficiently responsive to available therapies. Alimera hopes that this will lead to pricing approval in this indication in 4Q, 2013. The Transparency Commission of the French National Health Authority issued a favorable opinion for the reimbursement and hospital listing of Iluvien by the French National Health Insurance. The commercial launch could begin in early 2014.

Iluvien was initially rejected by NICE in the UK as being not cost effective for use in diabetic macular edema, which meant that it would not be reimbursed by the National Health Service, which is responsible for reimbursement for 90% of UK patients. This meant that only private pay patients could be addressed. However, NICE has recently found Iluvien to be cost effective for pseudophakic patients and this opens up a not insignificant opportunity.

Alimera began realizing Iluvien revenues in the second quarter of 2013 from operations in Germany and the UK as 18 units (90% in Germany) were implanted leading to revenues of $179,000. As of the quarterly conference call on August 12th 2013, Iluvien had been used by 14 physicians in the U.K. and Germany to treat a total of 30 patients with chronic diabetic macular edema. Initially patients are treated in one eye, but the company reports that good outcomes have led to some patients being treated in the second eye.

The European uptake has been slower than management expected primarily because of these reimbursement hurdles. Looking ahead, they cautioned that demand could flatten in the 3Q and early 4Q as physicians assess the first patients treated before some upward inflection occurs in late 2013. By that time they hope that most of the reimbursement issues will be behind them. It seems to me that sales will probably be about $1 million in 2013. I would expect some significant improvement in 2014, but I can't give anything more than an outright guess of perhaps $5 to $10 million. I do believe that Iluvien has an important role to play in DME patients who have failed both VEGF and laser therapy and also in pseudophakic patients.

http://seekingalpha.com/article/1733322-psivida-previewing-t…

Zitat von Biohero: Das mit dem Shutdown und Schuldenobergrenze in USA macht mir sorgen deshalb werde ich vorerst bis zum 17. Oktober abwarten .

pSivida Corporation: Strong Takeover Target, October 17th PDUFA Date Make It A Buy

http://seekingalpha.com/article/1731522-psivida-corporation-…

Da Alimera den Zulassungsantrag ( PDUFA ) schon vor geraumer Zeit eingereicht hat und man davon ausgehen kann, dass die Gebühren dafür schon längst bezahlt wurden, sollte dies für Iluvien gelten: